Attack the Week (ATW)

November 3, 2024

Sunday Thoughts

November has started with a bang. And it’s not going to get easier. The much-awaited US election will be the spectacle to follow. It’s absurd that macro punters will have to find out the election results before moving on to what normally drives financial markets. After all, we have a Fed meeting and several other central banks reporting later in the week. Who cares it would seem as the prevailing narrative and focus is firmly set on what each outcome of Tuesday’s race will ultimately mean for financial markets.

In the long run, I always have doubts whether political changes really matter much for economic trajectories. After all, we have a financial market capitalization which is a healthy multiple of economic output and hence carries the stability and support of central bankers and politicians alike. Everything is ultimately ruled by markets. Take the UK government’s proposed budget as an example. Markets weren’t impressed, and if the bond tantrum continues, the labour government’s plans might have to be rewritten. That’s the power and efficiency of markets. You can’t tame the beast, it will tame you.

As for the election, I suggest you read the 3-part series Macro D has kindly put together.

Part 1: Debt, Deficit & Rates

Part 2: Showtime for Macro

Part 3: Socio-Geo-Political is the new Macro

I am going to stay up for the night and follow the stories unfold. Markets seem to be convinced of a Trump win, and with that comes a sweep in the congress. Everyone I talk to in finance is convinced of the outcome. I am also expecting him to win, but I’m not sure its going to be that easy. I am also preparing for overnight volatility, which often heralds opportunities. It is, however, a sad state of affairs. Watching both candidates’ campaigns, it would seem that it is more about stifling hatred and polarisation towards their opposition rather than framing a positive outlook and messaging for themselves and what they stand for. An election based on hatred and emotions can’t result in good things. I imagine having to vote in such an environment where emotions are running high and scaremongering is rife. I wouldn’t be surprised if an undecided voter is just going to see how they feel on the day, which can lead to surprising results. While there is no cross-read across different countries it’s worth noting that quite a few global elections have this year resulted in surprises. Will we get another one? I wouldn’t exclude anything.

As for markets, we had a big decline in equities as we head into the weekend. This is a natural setback ahead of the election, which we have witnessed before. This time around, however, US equity positioning is at much more elevated levels in comparison to the most recent election cycles. Some of it is the expectation of a Trump sweep.

As for the election process itself, it would appear that Trump’s path is a bit more straightforward compared to Harris’. He should have 262 electoral votes (270 to win) largely in the bag. Georgia and North Carolina are both still considered swing states, but Trump’s probability of winning each is sitting around 65% right now, according to Silver Bulletin. If we assume both go Republican, then he would need to win either Pennsylvania (SB probability: 56%; EVs: 19) or Wisconsin (SB probability: 44%; EVs: 10) to get him over the 270 mark. This sequencing is neatly summed up in the graphic below from the excellent blog:

There is obviously also the question of whether the president gets a sweep with Congress. As of now, a republic sweep has the highest probability with a Harris presidency and split Congress coming in as second. Taking these two events as the highest chance outcomes makes me wonder how much financial markets really have already discounted. I think a lot is already priced.

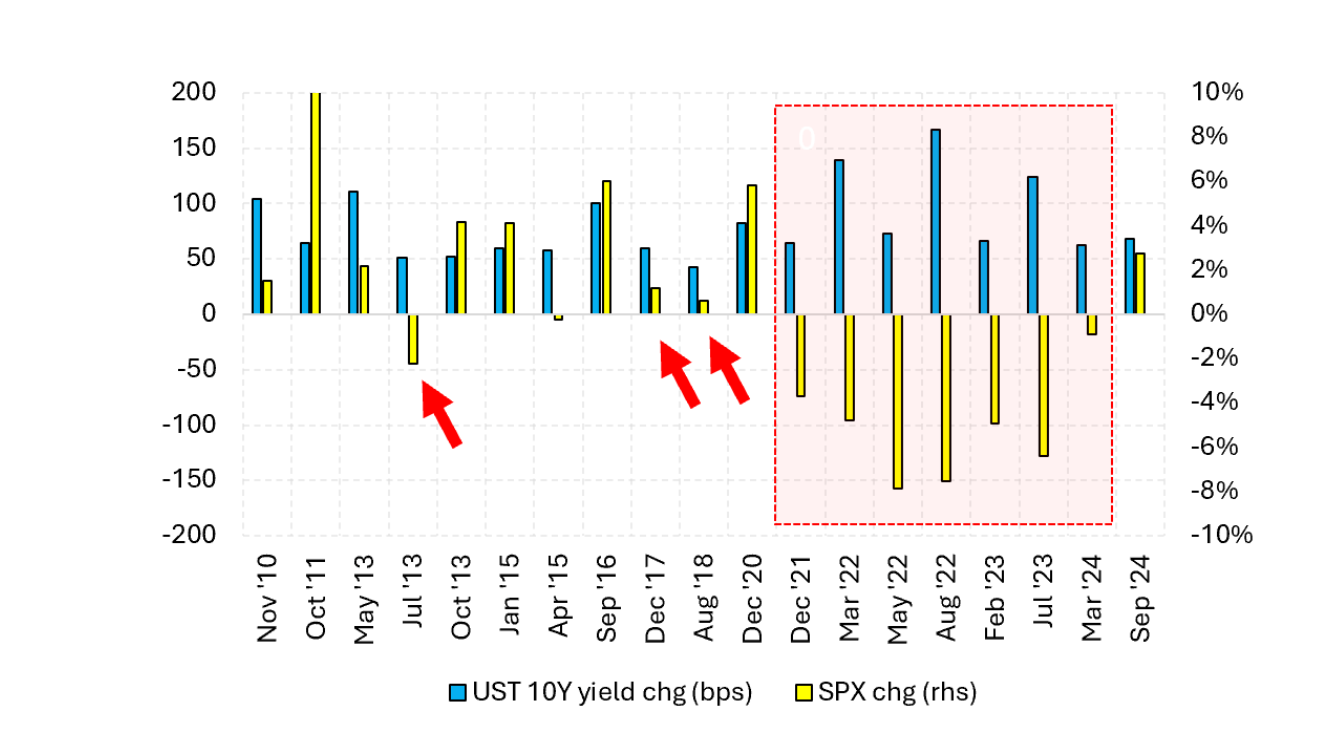

US bond yields (and global yields) have been grinding higher, punishing every attempt to buy it along the way. One of those reactions came on Friday, after the softer-than-expected payroll, which prompted a sharp reversal in bond yields higher. The US 10-year yield initially rallied almost 10 bps just to then sell off by 16 bps and close the day at the highs. Nasty.

When do higher yields impact equities? It really depends on where we are in the cycle as the following chart tries to demonstrate. Most of the underperformance came when correlations flipped to strong positives as the Fed lifted rates from 0 and hiked by 500 bps over the past few years. In other episodes, a higher Treasury yield did not necessarily mean lower equity prices as it was generally viewed as correlating closer to where nominal growth is currently tracking.

My personal nominal GDP tracker is currently just north of the 4.60% mark, not far from where US 30-year yields are trading.

As always, stay nimble and focused in the coming days. There will be many head fakes to navigate until it will hopefully become clear where we are headed. There are many scenarios where a clear winner won’t immediately be known, and as such a more volatile market environment would most likely ensue. Rest assured I will send updates and our charts shall guide us, as they always did, through these times as well.

Let’s now hear from our friend Macro D and his latest thoughts before we scan the calendar for other macro events in the week. We shall then explore the 10 most important charts for the week before we look at how the asset allocation model is positioned for the upcoming sessions.

Let’s go!