Attack the Week (ATW)

Unnerving Calm / Weekly Calendar / Macro FX Spreadsheet / Asset Allocation Update

Sunday Thoughts

I’m now back from my travels, and I hope you are all enjoying the summer solstice if you are based in the northern hemisphere. While fighting off the jetlag, I’m scanning charts and reading a few research reports to plan the week ahead. There is, admittedly, not much going on, but I have noticed some subtle changes.

I have laid out my Warsh thoughts in Friday’s thought piece, and nothing has changed my stance. See details below.

Friday Thoughts

A glorious good morning to all of you. My travels conclude this weekend as I slowly ease back into modern life after spending some valuable time in the wilderness. My internet connection was patchy at times, but I tuned into Warsh’s first FOMC meeting. Many think the game has changed; I disagree.

When scanning markets, one of the more fascinating aspects is not that equities continue to grind higher, but how little investors seem to care about everything happening around them. Over the past few months, we have traded through a regional banking crisis, a Japanese bond-market scare, Liberation Day, a war in the Middle East, the temporary closure of the Strait of Hormuz and now what may prove to be the most meaningful shift in Federal Reserve communication policy in over a decade. Despite all of that, the S&P 500 continues to make fresh highs, and implied volatility remains remarkably subdued. Looking only at the index level, one could be forgiven for concluding that markets are extraordinarily stable.

The reality beneath the surface looks rather different. What strikes me is not the resilience of the AI story, but how ownership of that story continues to evolve. Investors are no longer simply buying the obvious mega-cap beneficiaries. Capital is moving deeper into semiconductors, power infrastructure, data centres and Asian supply chains. In many ways, the AI story is becoming broader rather than narrower. The secular thesis remains intact, earnings revisions remain supportive and corporate investment spending continues to point towards a multi-year cycle. If anything, conviction around AI appears stronger today than it did six months ago.

The challenge, however, is that everybody knows it. Hedge fund leverage has climbed sharply, semiconductor allocations have reached record levels and positioning throughout large parts of the AI ecosystem has become increasingly crowded. That does not mean the trade is wrong. Some of the most profitable trades in history were crowded because the underlying thesis was fundamentally correct. What it does mean is that market behaviour increasingly becomes driven by positioning and flows rather than purely by fundamentals. Markets can remain directionally right even as they become structurally fragile.

That is why I think many investors are missing what is actually happening underneath the index. While headline volatility remains low, factor rotations, sector moves and single-stock reactions have become increasingly violent. We continue to see aggressive leadership swings and sharp repositioning beneath a seemingly tranquil surface. The index looks calm, but the market itself feels considerably less stable. It is a distinction that has become increasingly important this year.

What also stands out is how quickly investors have moved on from geopolitics. Oil has already surrendered most of its war premium, and speculative positioning has rapidly shifted back towards outright bearish bets. The market appears to have concluded that the Iranian conflict was little more than a temporary interruption. Perhaps that assessment ultimately proves correct. Yet markets often dismiss risks immediately after they materialise, while obsessing over them beforehand. The lesson from the conflict may not be the impact on oil prices themselves, but the reminder that relatively small actors can still create significant disruptions through strategic chokepoints and asymmetric means.

More broadly, I suspect (and hope) that we are witnessing the return of macro as a dominant market driver. For much of the last decade, investors operated in an environment where central banks worked tirelessly to suppress uncertainty. Every speech, every projection and every dot plot existed partly to reduce volatility and guide expectations. If Warsh follows through on his rhetoric, that world may be changing, although I remain sceptical. A more credible Federal Reserve is likely to be a less predictable Federal Reserve. Every inflation print, payroll report and FOMC meeting becomes more consequential when investors are no longer handed a detailed roadmap of future policy decisions.

Ironically, that may ultimately be a healthier outcome. Markets often confuse predictability with stability. They are not the same thing. A central bank that responds quickly to emerging risks may create more short-term policy uncertainty, but it may also reduce the probability that larger policy mistakes become embedded in the economy. The path of rates may become less predictable, while inflation's path becomes more stable.

For now, I remain struck by the extraordinary calm that surrounds markets. The macro backdrop is shifting, policy frameworks are evolving, leverage is rising, and positioning is becoming increasingly concentrated. Yet investors continue to behave as though very little has changed. Perhaps they are right. But increasingly, I find myself wondering whether the market’s greatest source of risk is not what investors worry about, but what they have stopped worrying about altogether. Solstices and equinoxes sometimes bring a shift in change in market behaviour. I stand ready.

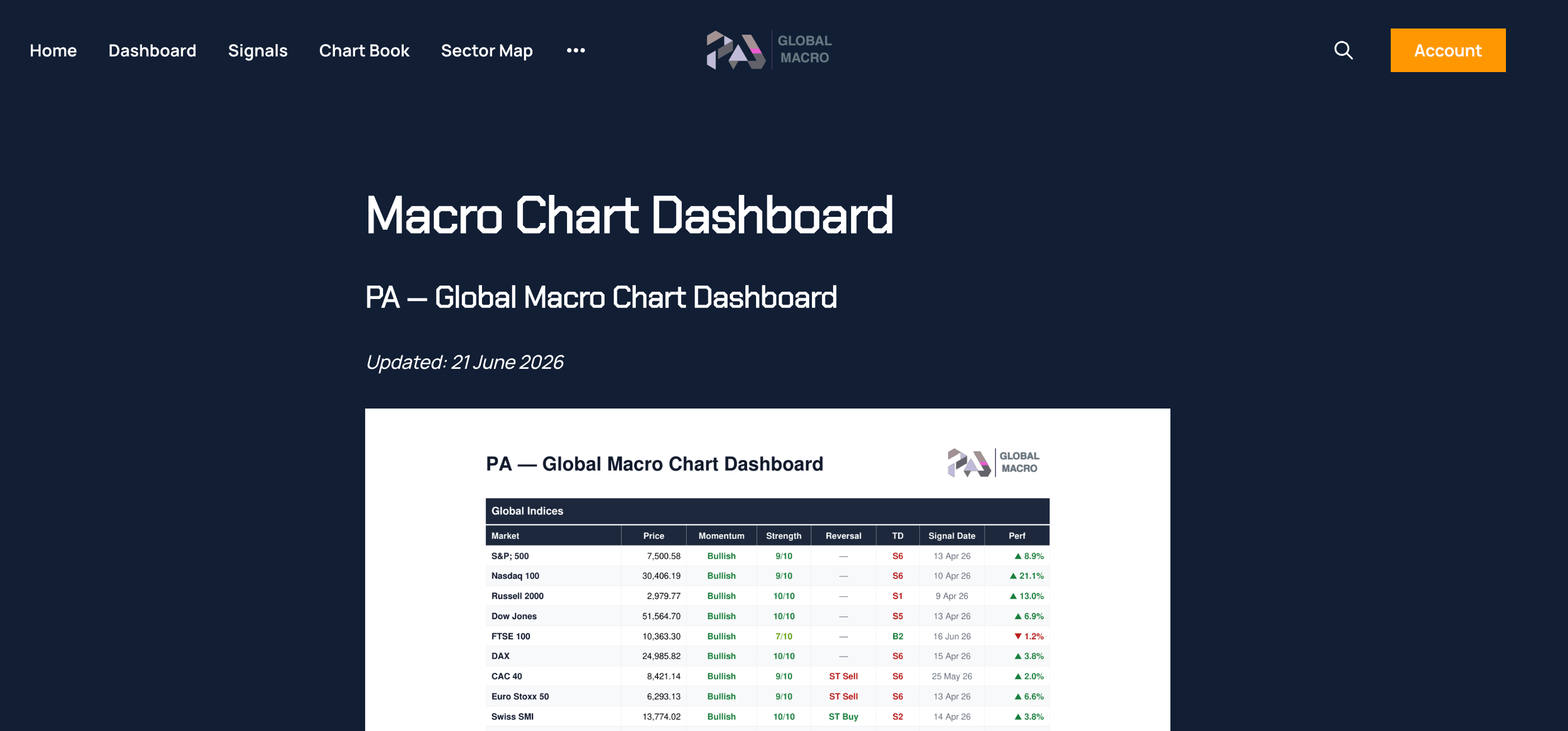

Let’s now read Macro D’s latest thoughts and study his latest Macro FX trades in the updated, detailed spreadsheet. We then scan the weekly calendar before walking through the latest global macro dashboard readings, which subscribers can access on our dedicated site at pa-globalmacro.com. We conclude the piece with the latest output of the asset allocation model. Details of the model’s workings can be found in the detailed piece below.

Macroscope

This is the second instalment of the Macroscope series. I will present an allocation model based on SPX and 10-year US Treasuries in the below section. As a quick refresher, edition 1 featured a liquidity model, which essentially provided entry and exit points for equities, in this case, the