Friday Thoughts

Warsh reality / Macro week in review

A glorious good morning to all of you. My travels conclude this weekend as I slowly ease back into modern life after spending some valuable time in the wilderness. My internet connection was patchy at times, but I tuned into Warsh’s first FOMC meeting. Many think the game has changed; I disagree.

For most of my professional life, I have spent an inordinate amount of time analysing central banks and their reaction functions. Like many macro investors, I became accustomed to dissecting every FOMC statement, every ECB press conference and every speech delivered by a voting member somewhere on the conference circuit. Entire teams of economists would spend hours debating whether a single word had become more hawkish or dovish, while markets attempted to reverse engineer reaction functions that often appeared as complicated as the economies they were supposedly trying to manage.

Over time, however, I have increasingly come to the conclusion that central banking has become far too complicated, far too communicative, and, perhaps most importantly, far too confident in its ability to forecast the future.

The rise of forward guidance was largely a product of necessity. Following the Global Financial Crisis, central banks found themselves trapped at the zero lower bound. If rates could not be cut much further, policymakers sought alternative ways to influence financial conditions. Expectations became a policy tool. Rather than simply setting interest rates, central bankers attempted to shape the entire future path of policy through forecasts, projections, speeches and increasingly detailed reaction functions. The theory was straightforward enough. If markets believed what central banks would do tomorrow, financial conditions could adjust today. There is some truth in those assumptions.

What started as an emergency measure gradually evolved into an institutional obsession.

Every quarter brought a fresh set of forecasts. Every meeting generated new projections. The famous dot plot became one of the most scrutinised charts in global finance, despite being nothing more than a collection of individual guesses about an unknowable future. Policymakers repeatedly reminded investors that monetary policy was not on a predetermined path, yet simultaneously published documents that encouraged markets to believe exactly that. The contradiction was obvious, but somehow became accepted as normal.

The result was that central banks increasingly became prisoners of their own communication. Every forecast became a commitment. Every projection became a benchmark against which future decisions would be judged. Every deviation required explanation. The more guidance policymakers provided, the less flexibility they retained. Rather than enhancing policy effectiveness, excessive communication often reduces policymakers’ room for manoeuvre.

This is one reason why I found the reaction to Kevin Warsh’s first meeting somewhat surprising. Having read some post-FOMC analyses, I was struck by how many commentators treated the changes as revolutionary. To my eyes, very little of substance changed. The statement became shorter. Some of the ritualistic language disappeared. Forward guidance was scaled back. The emphasis shifted away from forecasting a path and towards delivering an outcome. Frankly, most of this simply looked like common sense returning after a long absence.

The dot plot, in particular, has always struck me as one of the stranger inventions of modern central banking. Markets became obsessed with a handful of projections despite knowing full well that policymakers themselves routinely changed their minds as incoming data evolved. Investors treated the dots as promises while central bankers insisted they were merely forecasts. Neither side truly believed the distinction. The entire exercise created an illusion of precision that was never actually there.

What makes this even more relevant today is that the frameworks underpinning forward guidance were largely developed during a very different macroeconomic regime. The post-crisis world was characterised by secular stagnation, chronically weak inflation, low productivity growth and repeated demand shortfalls. Central banks spent much of the decade attempting to convince markets that rates would remain lower for longer. In that environment, communication itself became a policy instrument.

Today’s world looks very different. Inflation is no longer permanently dormant. Fiscal policy has returned. Supply shocks matter again. Geopolitical fragmentation, tariffs, energy disruptions and demographic constraints are increasingly important drivers of economic outcomes. We are trying to apply frameworks developed for one regime to a world that increasingly resembles another. Unsurprisingly, the results have been mixed.

One aspect of the recent shift that I do find encouraging is the recognition that central banks do not need to explain every thought process to markets. A credible central bank should not have to. In fact, the most effective monetary regimes often rely less on communication and more on credibility. If investors genuinely believe that policymakers will deliver price stability over time, markets themselves do much of the heavy lifting. Expectations adjust, yields move, and financial conditions tighten or ease without policymakers having to provide a detailed roadmap for every future meeting.

In many respects, central banking drifted well beyond its original mandate over the past fifteen years. Policymakers increasingly found themselves discussing financial stability, wealth inequality, climate risks, asset prices and a host of other issues. Meanwhile, inflation reminded everyone that preserving the purchasing power of money remains the primary responsibility of a central bank. The more objectives policymakers attempt to pursue with a single instrument, the greater the likelihood that they ultimately fail at several of them simultaneously.

That said, investors should be careful not to mistake changes in communication for changes in behaviour.

While some of the old frameworks may finally be disappearing, institutional habits tend to survive far longer than policy documents. The same central bank remains in place. The same intellectual biases remain embedded in the institution. The same preference for caution remains. The same tendency to wait for overwhelming evidence before acting remains. While some observers have interpreted the recent changes as evidence of a more hawkish Federal Reserve, I am not entirely convinced. The furniture may have changed, but the occupants remain largely the same.

Indeed, I suspect one consequence of reduced forward guidance may be that markets themselves assume a greater role in setting financial conditions. Less communication inevitably creates more uncertainty. More uncertainty encourages markets to do what they are supposed to do: price risk. Bond yields can rise, risk premiums can widen, and financial conditions can tighten without policymakers having to deliver a single rate hike. In many respects, that is exactly how the system should function.

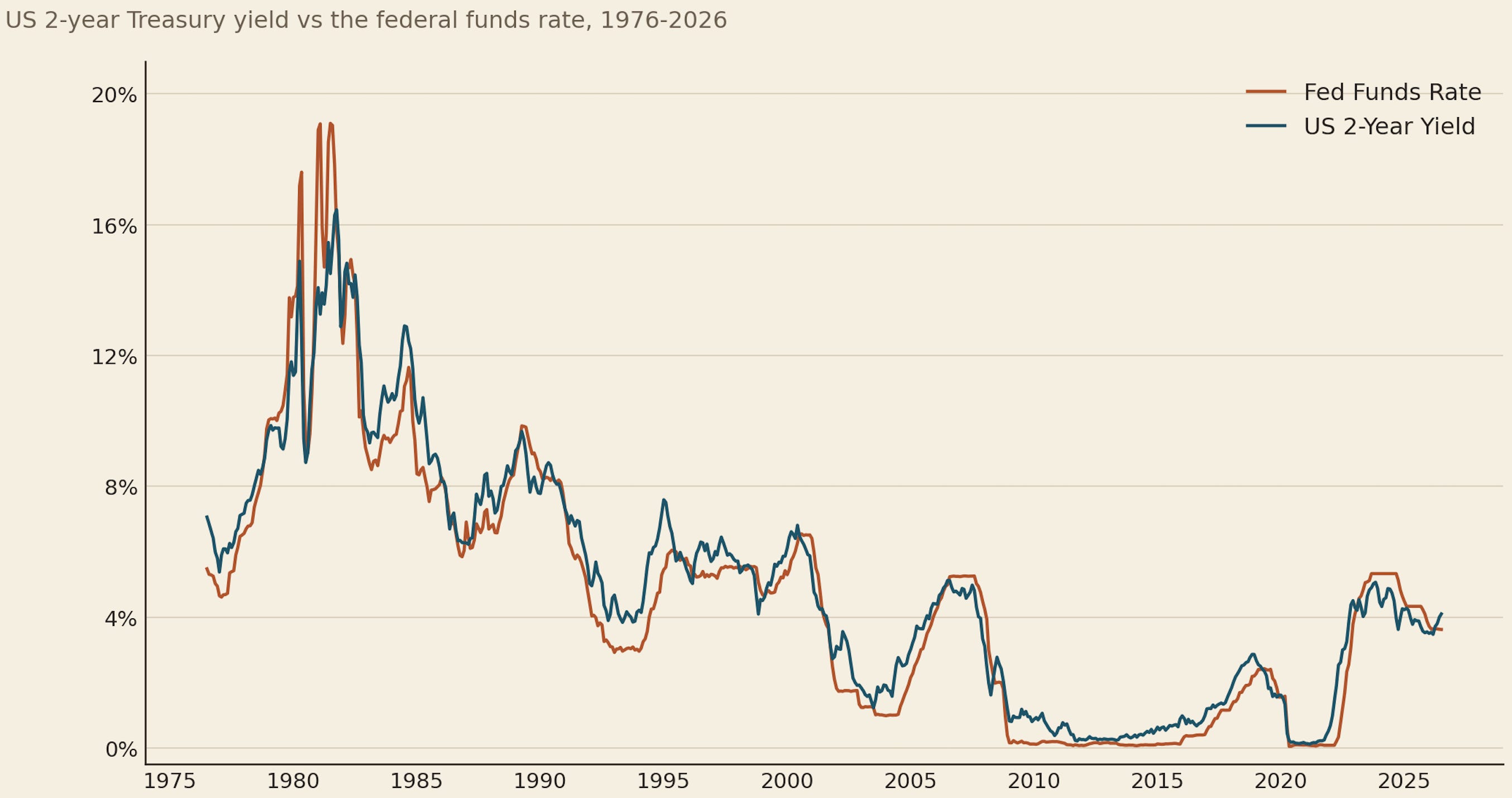

This is where I think markets are currently sending a message that policymakers may not yet fully appreciate. For years, I have viewed the US two-year Treasury yield as one of the best real-time indicators of where policy rates should be. It aggregates the views of investors, businesses, economists and institutions far more efficiently than any committee forecast ever could. While it is not perfect, it often provides a cleaner signal than the central bank itself.

Today, that signal appears relatively straightforward. The bond market is increasingly questioning whether the three rate cuts delivered last year were justified. Growth remains resilient, labour markets remain firm, and inflation remains more persistent than policymakers anticipated. If one were looking purely at the underlying macroeconomic backdrop, there is a reasonable argument that some of that easing should be reversed.

Will it happen? I am not so sure.

If the past several decades have taught us anything, it is that central banks are often slow to recognise changes in regime and even slower to reverse course. The Federal Reserve spent much of 2021 insisting inflation was transitory before spending much of 2022 trying to catch up with reality. That experience should have reinforced the limits of forecasting and the dangers of excessive confidence. Instead, many policymakers continue to behave as if sufficiently sophisticated models can eliminate uncertainty.

They cannot.

The lesson from the past twenty years is not that central banks need better forecasts. They should place less faith in them. The lesson is not that policymakers need to communicate more. They should communicate more clearly and less frequently. Most importantly, the lesson is that monetary policy was never meant to provide certainty about an uncertain future.

The best central banks are not those that tell markets exactly what will happen next. They are the ones that retain sufficient flexibility to respond when reality inevitably proves them wrong. The recent shift in communication may represent a step in that direction. Whether it ultimately produces a different reaction function remains an entirely separate question.

For now, I remain sceptical. The old framework may be disappearing, but I suspect the institutional dovishness that defined much of the past decade remains alive and well. The bond market appears to be telling policymakers that rates should probably be higher. Whether the Federal Reserve chooses to listen is another matter entirely. Markets are pricing them to hike this year. They should, but whether they will is a totally different matter.

For a history lesson and a detailed analysis of my view on how things might play out in light of a past analogue episode, I suggest everyone read the following piece I posted a few weeks ago. It’s closer now than it was when I wrote it.

Where Time Stops Rhyming

Analogues are a roadmap, not a prophecy. History doesn’t repeat. It mumbles, and if you’ve been at this long enough, you start to recognise the tune.

A reminder that the technical model site over at pa-globalmacro.com is fully operational and updated daily. Subscribers can choose to receive daily emails highlighting changes to any of the running models. Subscribers to this publication automatically gain access to the technical website, where they can log in with the same email. There are no trials available.

Behind the paywall, Macro D shares his thoughts on the week just gone by and any meaningful changes he made to his Macro FX portfolio. He is analysing the BoJ, FOMC, RBA and BoE meetings.

Let’s go!