Mid-Week Update

CPI and State of Play ahead of FOMC

CPI did little to change expectations for today’s FOMC meeting. This could open a window for Powell to acknowledge Waller’s comments on how a Taylor rule approach would ultimately demand the Fed to cut rates as inflation slows back to target. The Taylor rule concept is quite a theoretical way to ascertain an appropriate monetary policy stance. While outdated it is clearly still used amongst our monetary decision makers. I have previously opined on it in the below post, which is still very much valid.

Inverse Optimal Control Monetary Policy

When Janet Yellen was the Fed Chair from 2014 to 2018, some of her mostly dovish concepts came to the forefront when anticipating future monetary policy stances. I studied her academic views regarding rules-based monetary policy strategies in detail, as it showed me how far they will likely go in keeping rates lower for longer. It was one part of my long-held long bond thesis back then.

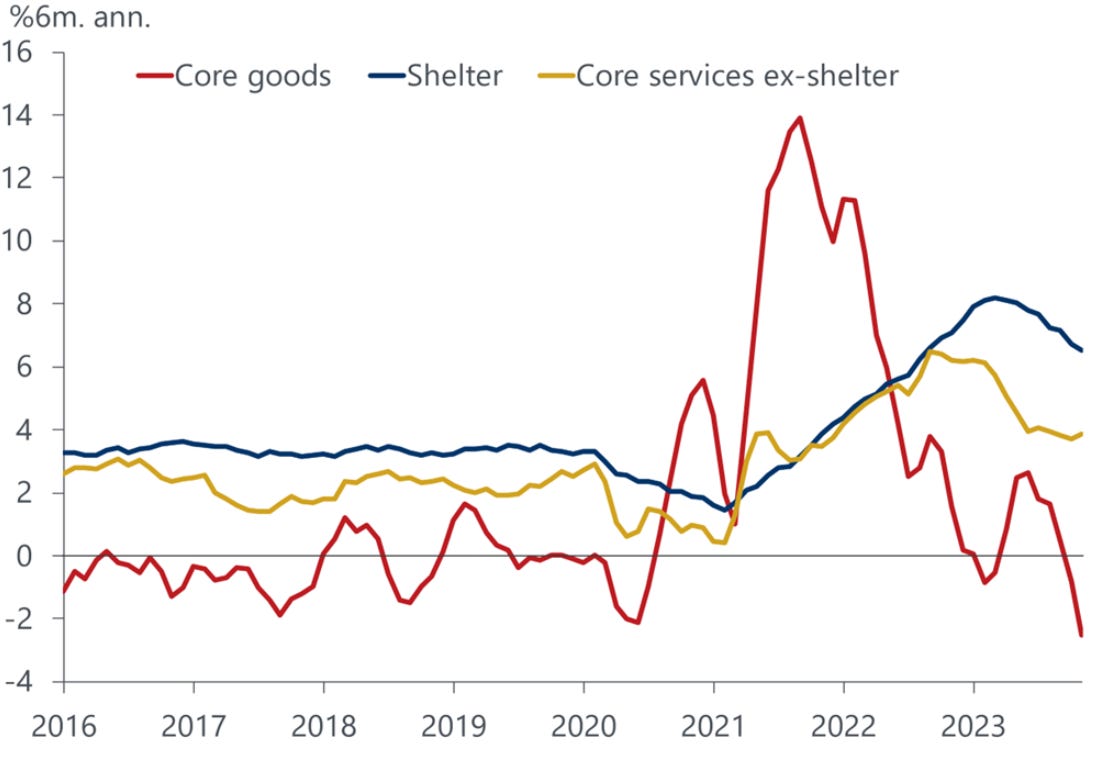

The most concerning element from yesterday’s inflation report was the persistence in services inflation. Core inflation also seems to be stickier than anticipated, with a YoY print of 4%, which failed to decline for the first time since the first quarter of this year. Core goods prices continue the downward trajectory, offsetting shelter inflation and OER (owner equivalent rent) rise. With the strong link to still buoyant wage inflation it will be hard to see how this would cool enough for the currently priced 25 bps cut by May 2024 to materialise.

Overall, the street anticipates a downward shift in median dots of 50 bps in ‘24 and ‘25, respectively, which is basically bringing back dots to their June SEP. As also opined in ATW, I would anticipate Jay to lean against the more dovish near-term market pricing. There is no rush for them to deliver cuts even if you are following a Taylor rule type of approach. Jay could also open up the discussion of the necessity of a risk management approach with regards to ensuring inflation isn’t anchored at current levels and monetary policy restrictive enough still to bring inflation back into their target zone. How does he do that? By stating that they still have a tightening bias in place and that their indicated lower dots are all contingent on their success in pushing inflation lower. The logic is simple: you can’t have dovishness without a good dose of hawkishness first.

Overall, it will be quite an important meeting as it will set the tone for asset markets for the remainder of this year and then to the start of 2024. Markets will most likely focus on any dovish element within the speech. As I type, PPI came in softer than expected, further pushing a dovish expectation into today’s meeting.

While we wait for Jay to appear (I am thinking grey/blue tie, similar to last December), let’s look at what my models have been flagging in the meantime.