Friday Thoughts

Warsh + 1 Week / 3 Years on / What's next?

The stifling heat this week has forced me to move my writing sessions to cooler locations. I’m writing this in a co-working space where many cool prototypes frequent. It’s more of an artist's place. While others are talking about fashion, music, and the latest London hotspots, I am scanning markets and preparing for the second half of the year. You can argue it’s art, but of the boring kind.

Talking of boring outcomes, as I wrote last Friday (see post below), the market’s initial interpretation of the FOMC as a meaningful hawkish shift has now been largely unwound. More than a week later, the message from price action is clear. US 10-year Treasury yields are now trading below their pre-FOMC levels, erasing the post-meeting repricing almost entirely.

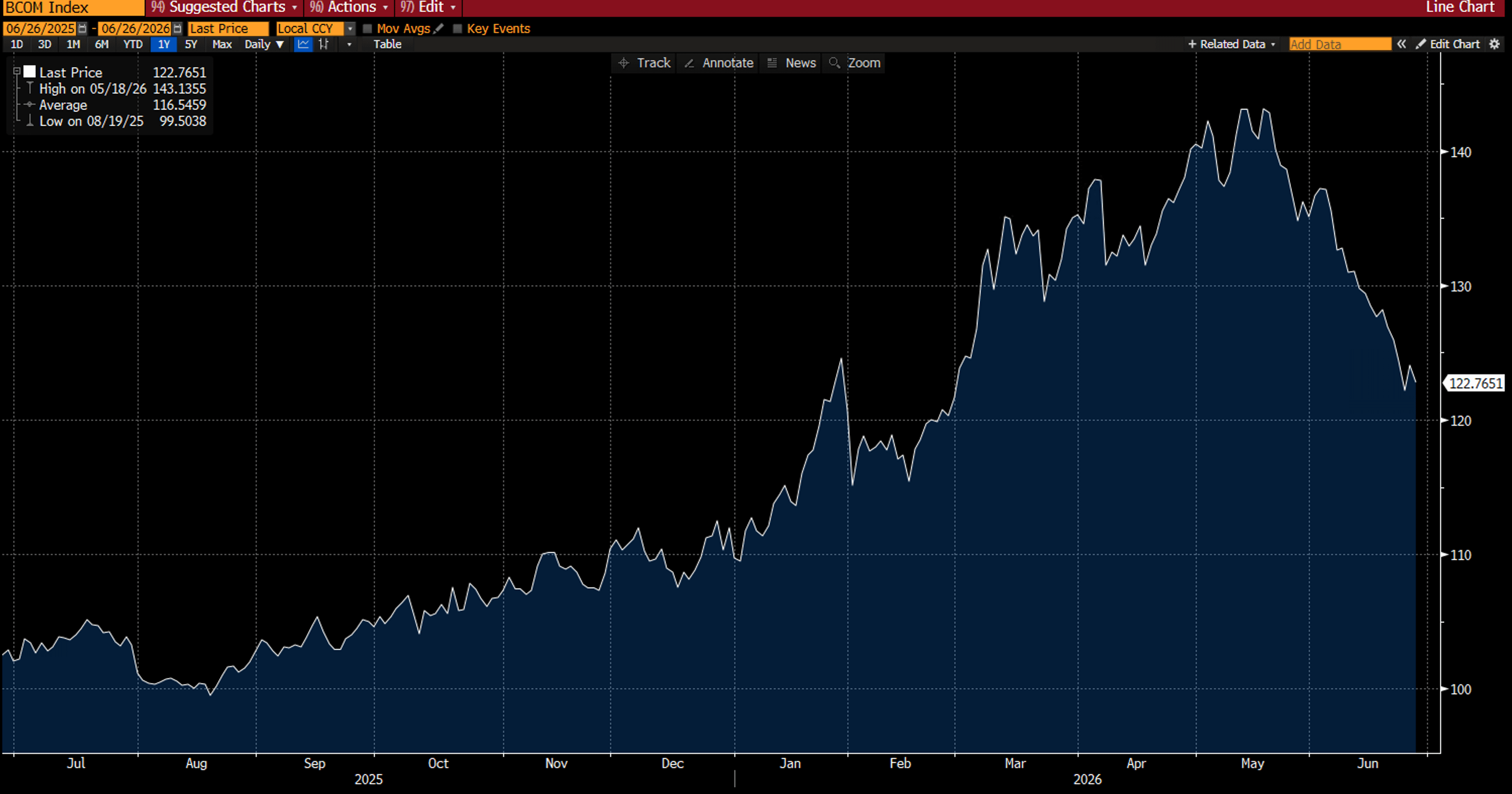

The biggest driver has been commodities. Oil has continued to retrace following the ceasefire in Iran, while broader commodity markets have softened materially. The Bloomberg Commodity Index (BCOM) has now fallen back close to levels last seen before the conflict began. With one of the market’s biggest inflation fears fading, inflation breakevens have eased and nominal yields have followed suit. Markets have once again demonstrated how quickly geopolitical risk premiums can evaporate once headlines disappear.

Friday Thoughts

A glorious good morning to all of you. My travels conclude this weekend as I slowly ease back into modern life after spending some valuable time in the wilderness. My internet connection was patchy at times, but I tuned into Warsh’s first FOMC meeting. Many think the game has changed; I disagree.

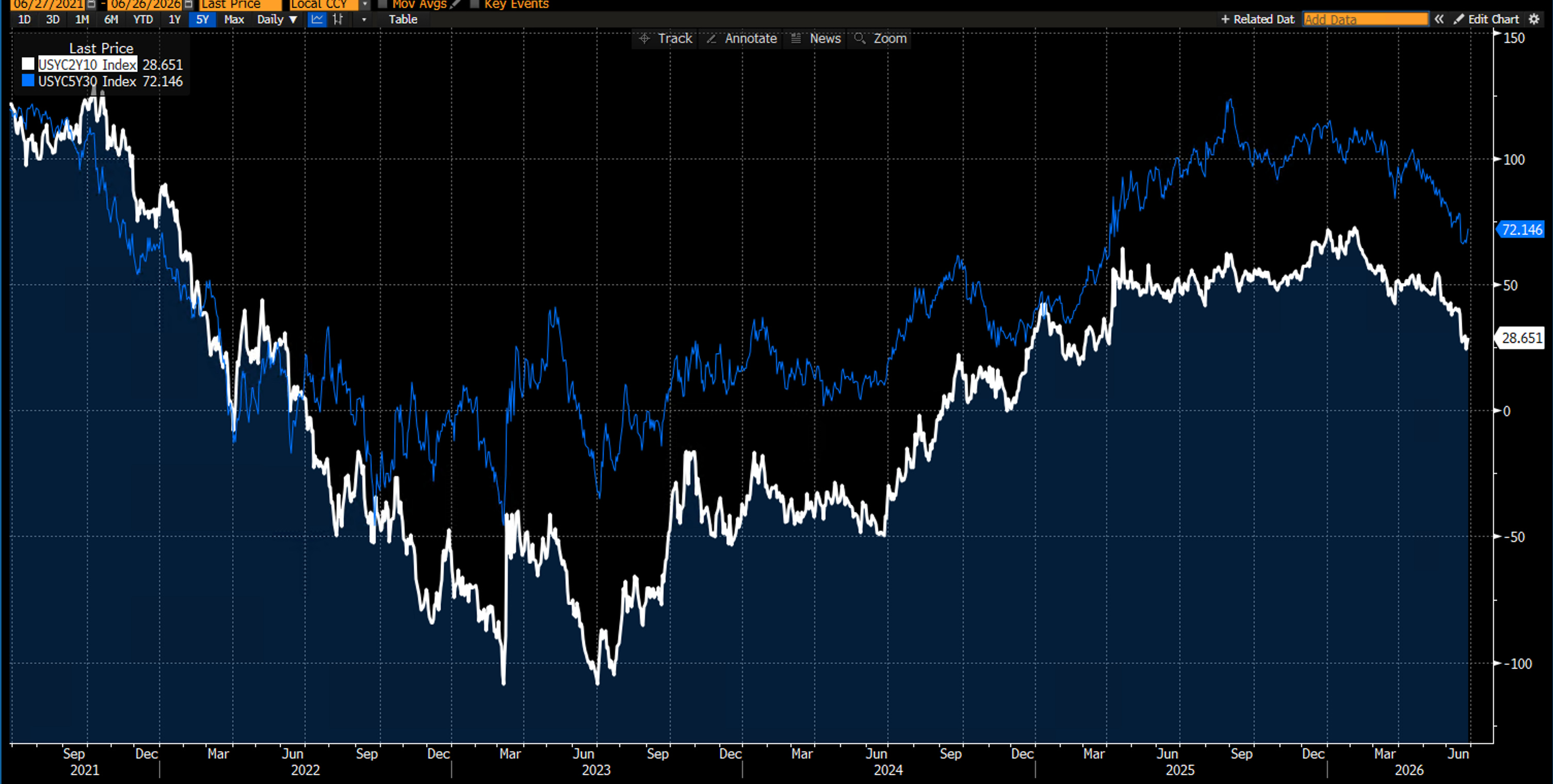

The curve, however, tells a more nuanced story. Yield curves have flattened as the front end remains comparatively sticky while longer maturities rally. That makes perfect sense to me. Markets still have little conviction regarding the reaction function of the “new” Federal Reserve. Chair Warsh’s first meeting undoubtedly shifted the tone of communication, but one meeting does not establish a framework. Investors are still trying to determine whether the emphasis on price stability represents a genuine structural change or simply a more hawkish starting point that reverts to the familiar playbook whenever growth softens. You know my thoughts: The Fed has not changed its colours overnight. Forget it.

Cross-market rate differentials continue to do much of the heavy lifting. European and UK government bonds have outperformed Treasuries over recent weeks, widening relative yield advantages in favour of the US and helping underpin the dollar’s recovery. Much of the recent dollar strength has been less about renewed US exceptionalism and more about relative rates moving back in America’s favour as overseas curves rally even harder.

So, where from here?

Seasonality is becoming increasingly important. We are entering the heart of the northern hemisphere summer, a period that typically brings thinner liquidity, lower realised volatility and fewer meaningful macro catalysts. That does not necessarily mean markets become quiet—summer has produced plenty of surprises over the years—but absent a major geopolitical shock or a significant inflation surprise, realised volatility tends to compress while investors increasingly focus on harvesting carry rather than chasing large directional themes.

Carry remains the dominant strategy across much of the hedge fund and institutional universe. Whether in FX, fixed income or credit, investors continue to be paid to own yield while waiting for the next macro regime shift to emerge. That environment can persist for longer than many expect, particularly if inflation continues to moderate and central banks remain comfortably on hold.

For me, the bigger question remains whether markets are once again becoming too comfortable. Volatility has fallen quickly, geopolitical risk premiums have disappeared almost overnight, and financial conditions continue to ease despite central banks insisting policy remains restrictive. That combination rarely lasts indefinitely. Summer may well become a period of collecting carry, but history suggests that it is often during these quiet periods that the foundations for the next major move are laid.

No matter what, we will continue scanning markets and prepare for what’s ahead. If there is one universal truth in markets, it’s that you should never be too complacent.

It’s now nearly 3 years since I opened my own approach, thoughts and models to paying subscribers, and I’m quite astonished how fast time has flown. I’m humbled by the reception and following I have received, and I am particularly blessed that some of my earliest backers are still with me today.

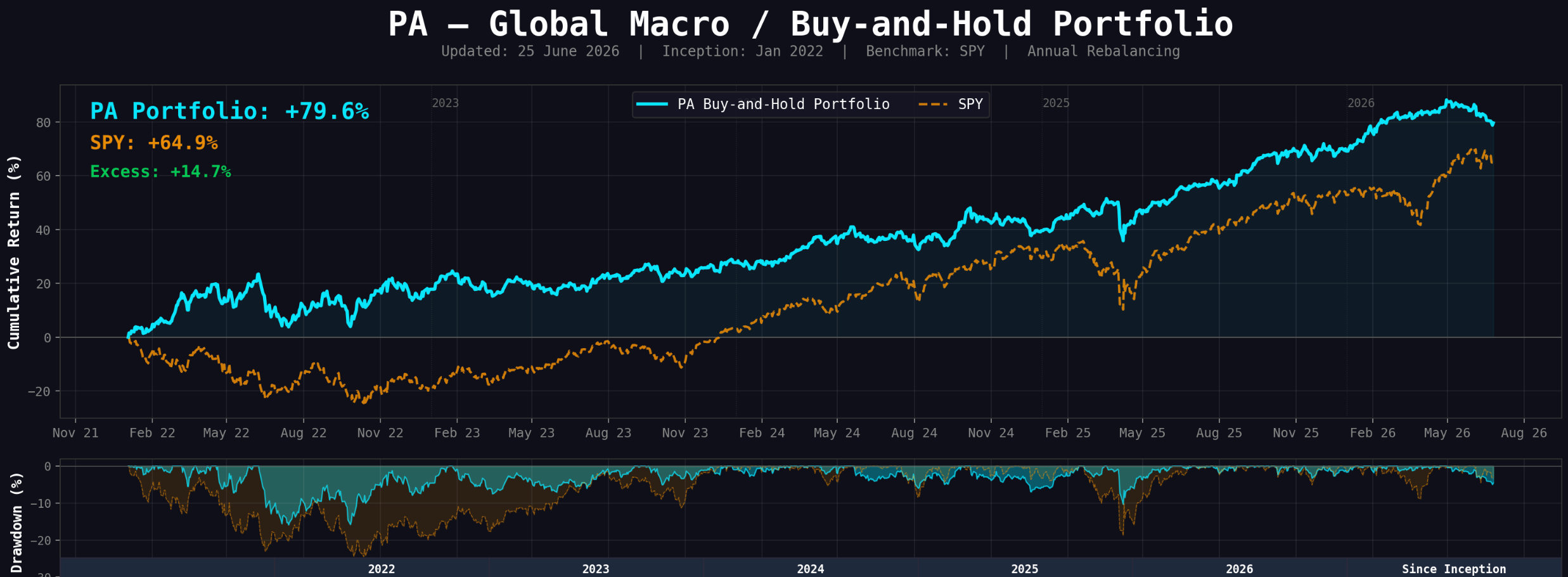

We have grown considerably since then, and with that, I have kept pace by producing free educational content and making my models and strategies available. The yearly buy-and-hold portfolio, for example, which I launched in 2022, is still beating the SPX comfortably over that time horizon, with considerably less volatility. This was particularly evident this year during the war period. Long may it last.

All of my models and strategies have moved to a dedicated site over at pa-globalmacro.com, which features the above portfolio and details, the daily dashboard of momentum and reversal indicators, a daily signal dashboard of any meaningful changes and the entire single security chart book spanning more than 200 securities, from single-name stocks, rates, FX, commodities to crypto. Paying subscribers on here have full access to current and future releases of the offering, which I will be expanding soon. There is an option on the site to subscribe only to those models, which will not include the Substack offering.

You know, three years ago, I wrote the following sentence in this publication before I launched paywalled content.

“Life is about making a difference, and that’s the firm goal I have set out with my commitment to this.”

You know, 630 articles later, I think I have achieved that for my subscribers so far, and I want to thank you all wholeheartedly for your support in making this journey a wonderful experience. Let the good times roll.

Below the paywall, we have my loyal friend and contributing member, Macro D, provide his thoughts on the macro week just gone by and what, if any, changes he has made to his Macro FX portfolio.

Let’s go and enjoy a wonderful weekend.