Friday Thoughts

Are Equities the Dominant trade? / +13% YTD / Central Bank Meeting Implications

April has come and gone in a flash. It was a weird month, and I think nobody would have predicted equities to perform the way they did if you had known that the war was still ongoing with a double blockage in place at the Straight and front oil contracts making new highs.

Themes and narratives don’t move as they "should”. I have written extensively about sufficient and necessary conditions when evaluating trade ideas (see the Macro Book article below). It’s at the very core of my process for isolating dominant trades from less dominant ones. In the same way, there are trade expressions that cover many different areas, meaning there is no binary distribution associated with their investment success. Gold last year was one of those expressions that spanned various themes, including deficit spending, reserve diversification, and anti-dollar movements.

Macro Book

Welcome to another article from the Macro Book. In the second instalment of the idea structuring series, I will build on the last article, where we dissected the art of great trade selection. This time, I will explore the idea of dominant trades and how to scan, observe and go after them. This will give you a

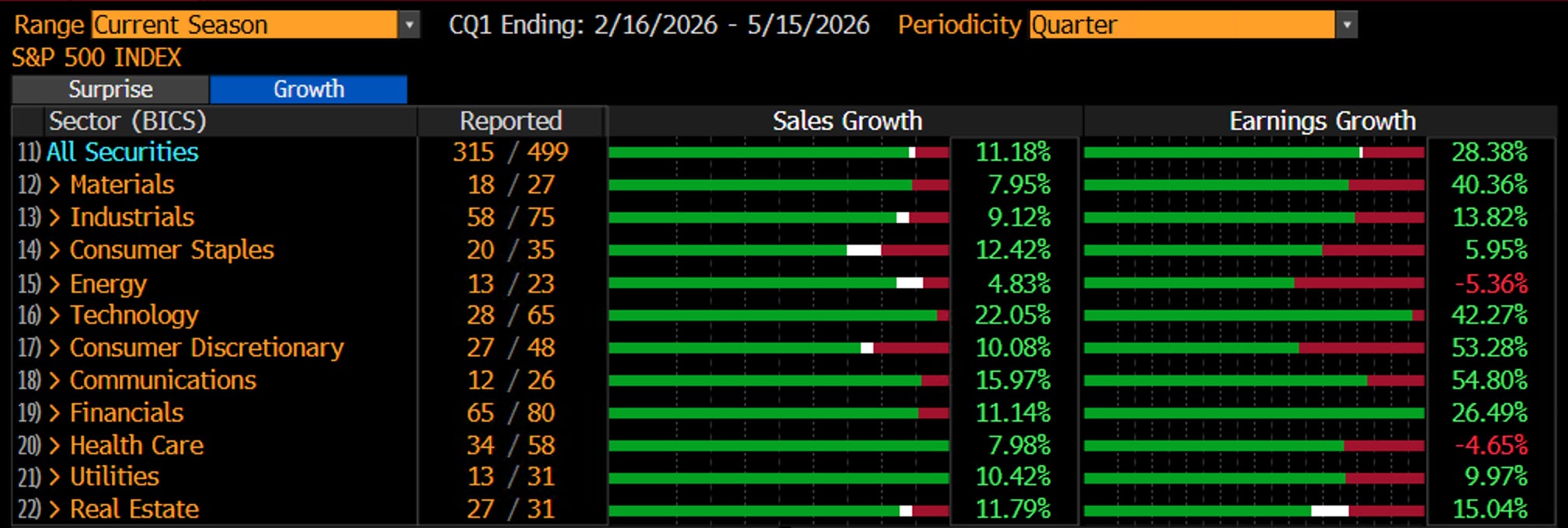

Are equities the dominant trade here? The earnings season has done outstandingly well, with 28% earnings growth reported so far. But are equities the dominant expression above everything else?

Let’s look at some numbers. The forward P/E sits around 20.9x, above both the 5- and 10-year averages. The Mag-7 trades at 29.9x, compared with the S&P-493 at 20.0x. Tech drove two-thirds of S&P 500 earnings growth. The effective number of securities truly driving returns has shrunk to roughly 44, the lowest in 35 years. That’s not diversification. That’s dependence. And dependence is fragile.

As I explored in the Macro Book, dominant trades ripple across everything. Right now, the dominant trade is clearly AI-driven earnings growth. It’s compelling. It’s also the most crowded trade on the planet.

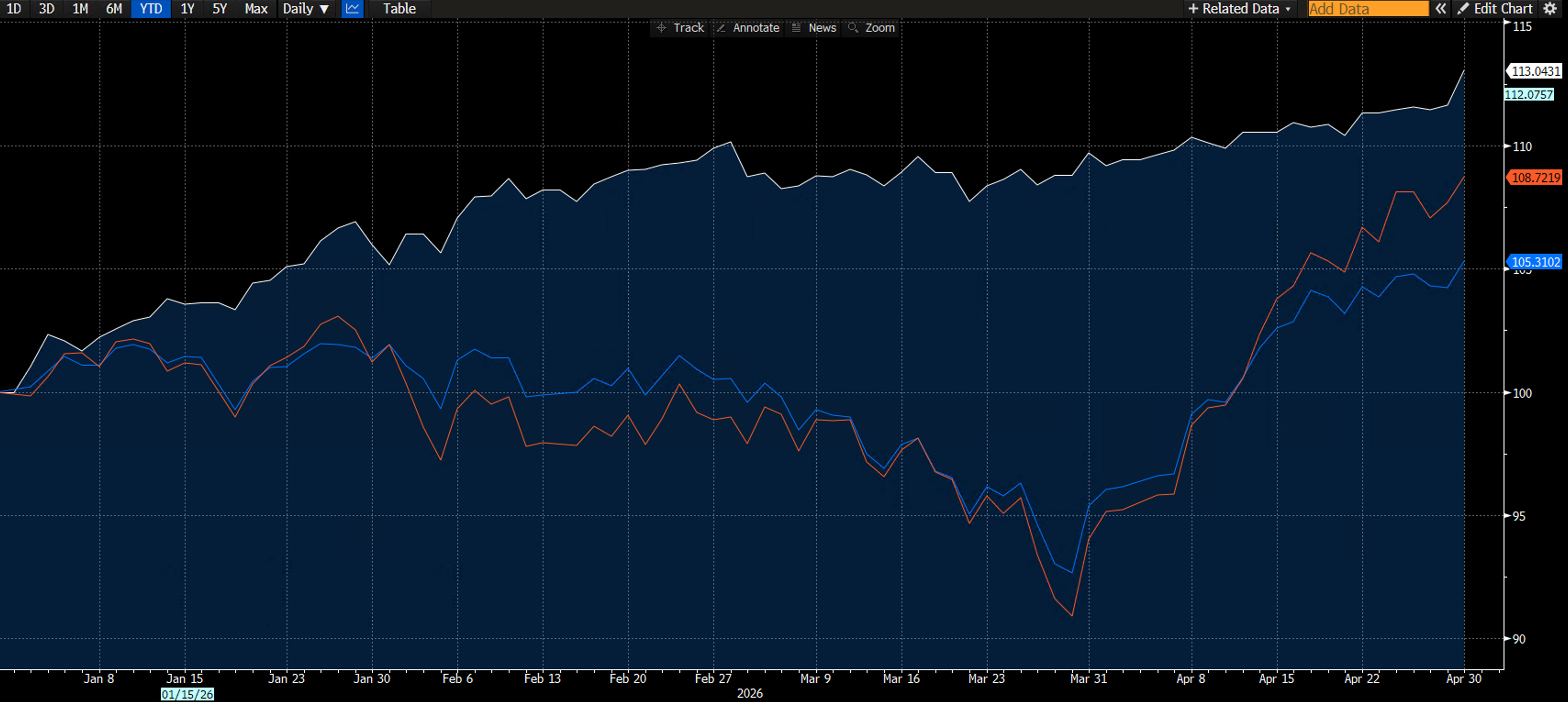

Most of the equity outperformance is also driven by the relative unattractiveness of other markets. Once-loved precious metals have lost their allure amid the inflationary impulse, which is not how they normally “should” react. Nominal bonds, of course, aren’t desired even as a diversifier, as central bank reaction functions remain unclear. Real bonds, meanwhile, are doing much better as the inflation expectations are driving yields lower. Below is the TIP ETF, which isn’t far away from levels seen before the war started.

The 2026 portfolio has reached new highs, now tracking just north of 13% YTD and still outperforming the SPX and Nasdaq since the start of the year, although the past month's bounce has narrowed that advantage. Still, the portfolio is offering much better absolute and risk-adjusted performance. Well-diversified portfolios, with exposures to attractive markets, are still the way to go.

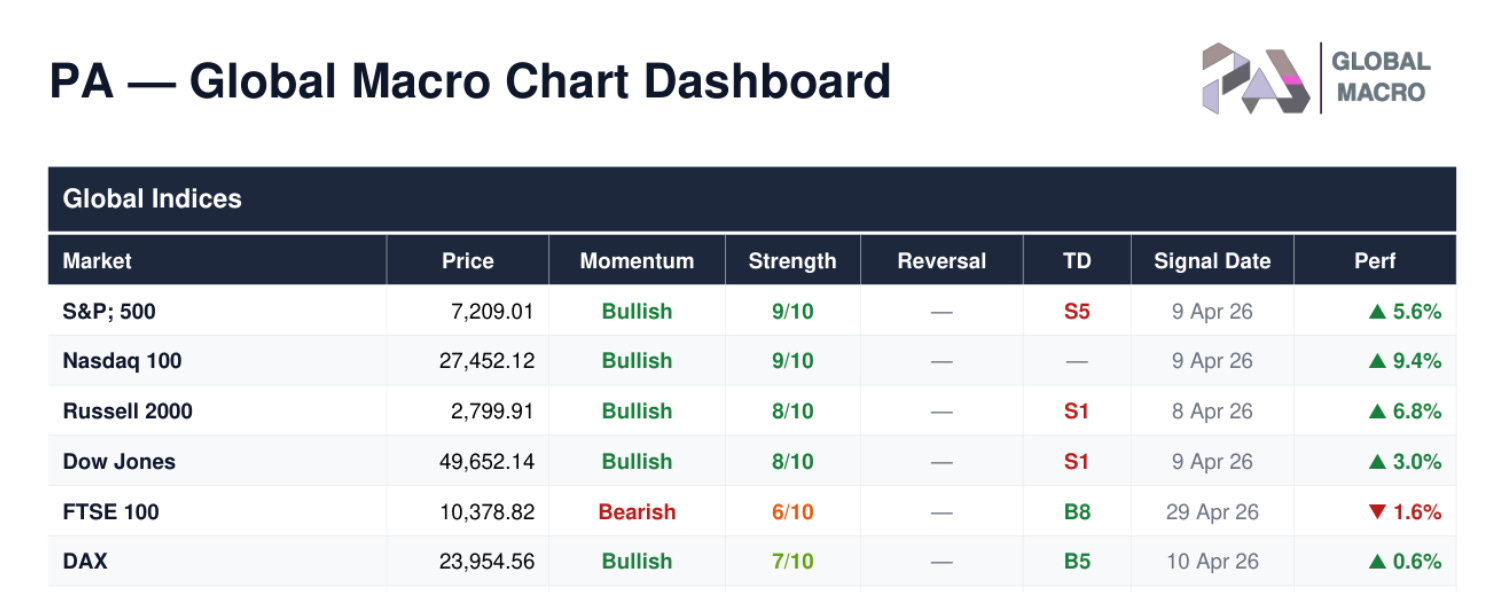

The newly launched site, dedicated to the technical models I have developed, is live and helping our subscribers navigate and identify new or exhausting trends across the global macro universe. The dashboard identified the shift in dominance in equities early, as the momentum model switched from short to long in early April.

My good friend Macro D has updated the Global Macro FX Trade Corner this week, which includes a detailed breakdown of his trades so far this month. See below for details.

Macro FX - Trade Corner Update

It’s not easy out there. Between the geopolitical noise, the tariff ping-pong, and markets that seem to swing on every headline, finding genuine macro trades with conviction requires a certain kind of discipline. Macro D, as always, cuts through the noise and focuses on what matters: the trades, the thesis, and the execution.

Let’s now read his latest thoughts and a summary of this week’s central bank meetings and FX implications. A detailed analysis of the BoJ (including yesterday’s FX intervention), the BoC, Federal Reserve, ECB and BoE meetings follows behind the paywall.

To my European friends, a happy long weekend. Enjoy!