Friday Chart Book

January 10, 2025

What a crazy start to the new year. I hope you are well-rested and focused. This isn’t going to be an easy year if the first week is any guide. Macro is officially back, and with that, the opportunity set is going to get larger. Exciting times are ahead. Bonds are the wrecking ball, and I have written at length that there are lazy longs and people constantly looking for the top in yields to buy. Meanwhile, we have tons of issuance on the calendar also in corporate bonds, which are going to likely put further pressure on rates. UK Gilts (10 years) especially had a tough week, and I wrote a very brief piece during the week, which you can find below.

Bond Market Update

Bonds are in a pickle. What started as a sell-off a few months ago is now continuing with further bear steepening across major market curves. You can see the 2/10s curves for a few developed markets below, which shows the highly correlated move.

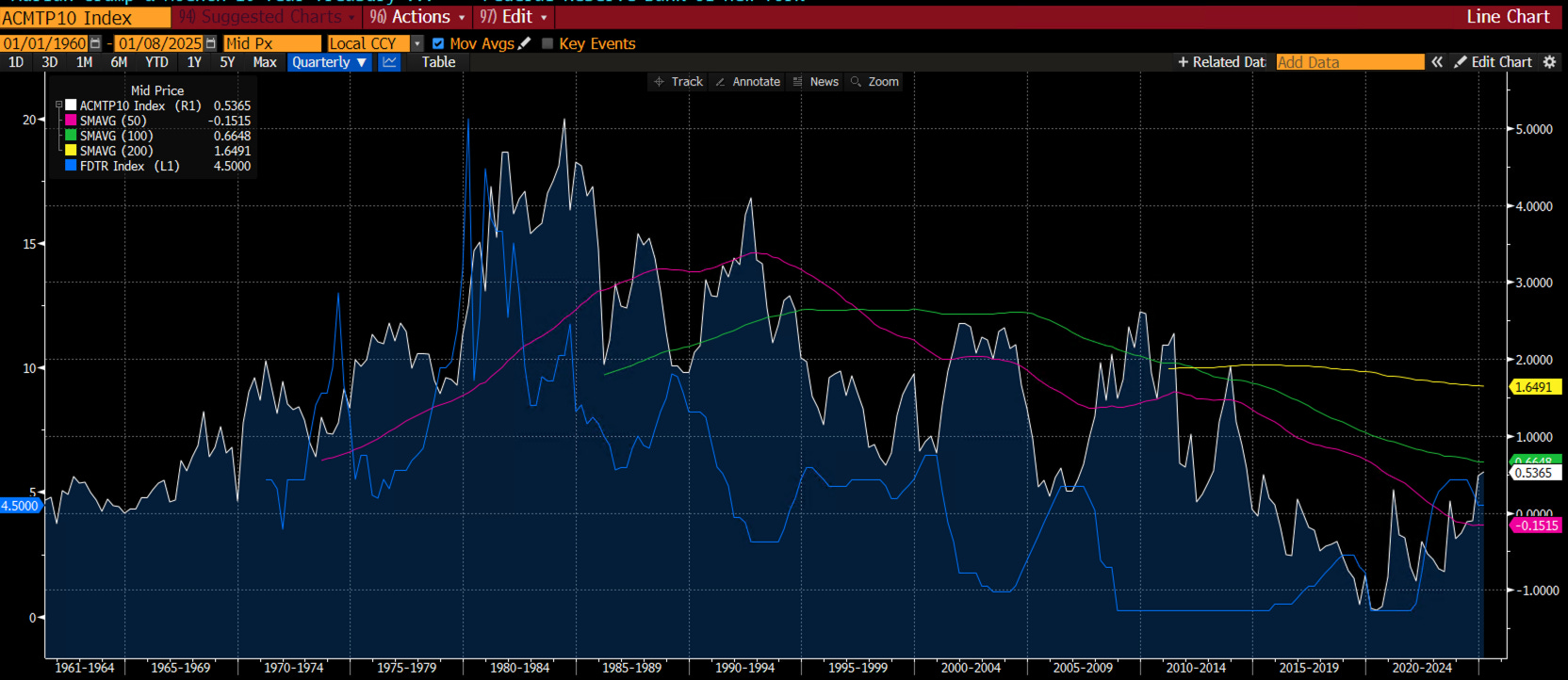

Term premium typically expands in easing cycles and then reverses in hiking episodes. You can see this below where the blue line (US Fed Funds) is plotted against the white line, which is the ACM model created by NY Fed economists Adrian, Crump and Moench. According to this model there is nothing crazy happening in Treasuries.

You could argue that the term premium for last year was too low, given Yellen’s move to issue more T-Bills and, therefore, deplete the Reverse Repo facility.

Today’s job report came in hot. I won’t repeat the details, but it was higher than many anticipated, with the unemployment rate surprisingly falling to 4.1%. Bonds got whacked again, with the front end feeling the brunt of today’s move and the curve bear flattening. Risk is getting sold with gold, BTC and energy to only performers on the day (so far). The US Dollar is king and outperforming everyone but the Yen in developed market space.

The market now sees only 30 bps of cuts for the remainder of this year. Let me translate this to you in plain speak. The market basically pretty much thinks that no more cuts are coming. Goldman has now only 2 cuts from the previous three, and Bank of America no longer expects more Fed cuts. You know what comes next.

Let’s think this through. I can see a path where equities start disliking the higher rates plateau and cause significant pain just when everyone is maximum long and loaded. I have written before how much of the consumption engine is relying on wealth effects. If this goes into reverse, I’d expect a significant slowdown and Trump won’t be able to do much about it. That’s where bonds will be a major buy but this might still be far away.

30-year yields touched 5% today. We are now at levels last seen in Q4 2023 when Fed Funds were 100 bps higher.

Meanwhile, the 5y5y real rate (think of it as the terminal real-rate) stands close to the 2023 highs. Remember, the real rate is the nominal rate less the inflation expectation component. Interestingly, it’s flat on a day today as the 5-10s curve flattened aggressively, while simultaneously, the 5-10s inflation swap curve also flattened. At some point, this becomes a very attractive buy.

The Michigan inflation survey was also an interesting read, with inflation expectations edging quite a bit higher. The most interesting aspect comes in the chart below. Since it’s a survey, I don’t put any emphasis on it but look at the difference in expectation by party affiliation. That’s crazy and suggests the survey is pretty much worthless. All hinges on what the new administration does, and as such, expectations in markets, businesses and on the ground might turn out to be quite a bit different than what will ultimately unfold. Buckle up. It’s going to be awesome.

The models have done a fantastic job this week and caught the major moves and reversals well. This is a reminder that you can now also use my models in TradingView scripts, which I made available for subscribers to use on their charts. This is not for free and incurs an additional cost. I am also in the process of making one of my intra-day models available. This will come at no additional cost to existing users, but new admissions will see a price increase. If you are interested, ping me an email with your TV username. Note that only paying subscribers will be granted access. No exceptions.

Let’s now read what my friend Macro D has in store for us (his thoughts are before the NFP). We then scan the multitude of charts I have updated below.

Let’s explore!