Cross-Currency Basis

Some Theory and Application

If only I could get a dollar for every time I read a Twitter post with the author using a cross-currency basis as an argument. The concept, while not immediately clear to many, is often used to depict a coming funding crisis and imbalance in markets. That’s not always the case.

As my commitment to continued free education to my esteemed readers, I will set my goal to explain a few basics in terms of the dynamics of cross-currency basis, their application in the real world and when and how they can give you a signal in markets.

Definition

At its core, a cross-currency basis swap is an agreement where two parties borrow or lend to each other in different currencies. The cross-currency basis itself measures the discrepancy between the interest rates of these currencies in the interbank market and the rates derived from the foreign exchange (FX) forward market.

Simply put, if you were to borrow in one currency and simultaneously lend in another via a currency swap, the cross-currency basis indicates the difference in interest rates between these two operations.

Historically, under the covered interest rate parity condition, the cross-currency basis should be close to zero. However, post the financial crisis, significant divergences from zero have been observed. This deviation from the equilibrium signals a dislocation in FX and money markets.

Before we go into the cross-currency basis dynamics, it is worth revisiting the non-arbitrage setting of covered interest rate parity, something that the most liquid FX world is relying on a daily basis.

Covered Interest Rate Parity

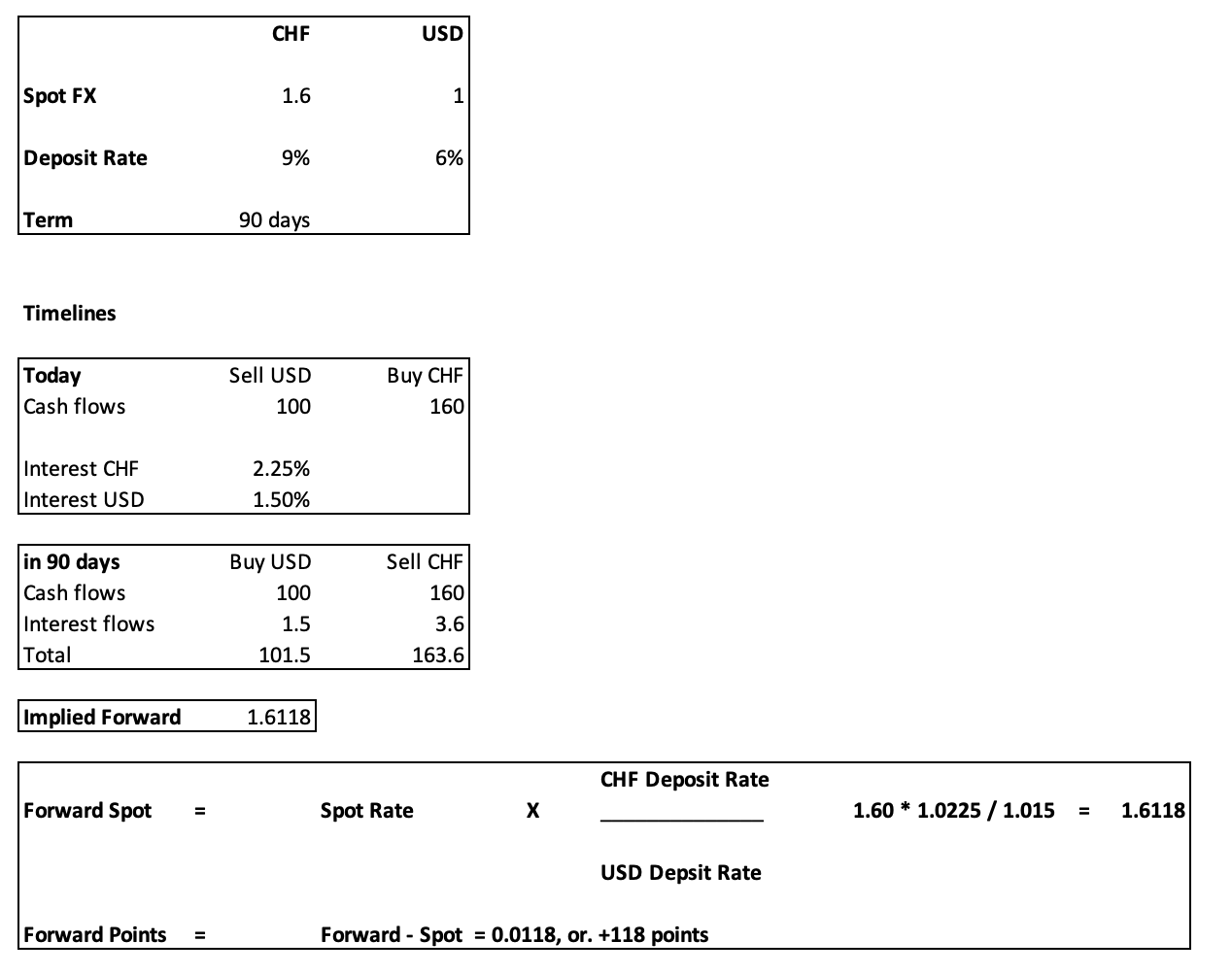

Let’s look at the dynamics of an FX swap and all its related cash flows.

Example:

You have a classic CHF/USD FX swap, where the spot rate is 1,60 and rates are 9% and 6%, respectively. I took a totally wild example, so none of the rates/spot rates are as of today.

Intuitively, what would you think the appropriate forward rate should be given the rate differential? Think about it first before you move on. Should the CHF weaken or strengthen in 3 months’ time?

The example above highlights the non-arbitrage setting for this swap, using money market rates to work out the appropriate FX forward. In this case, the CHF will have to weaken in 3 months’ time. That makes sense as it commands a higher interest rate than USD deposit rates.

Conceptually, you can think of it as one party borrowing one currency and simultaneously lending another currency to a second party. The borrowed amounts are exchanged at the spot rate and then repaid at the pre-agreed forward rate at maturity.

If the party lending a currency via FX swaps makes a higher or lower return than implied by the interest rate differential in the two currencies, then the covered interest rate parity fails to hold. Typically, the US dollar has tended to command a premium in FX swaps.

In essence, the cross-currency basis (often abbreviated as XCCY) is the difference between the theoretical value of the forward (as shown in our USD/CHF example above and the observed market value in markets.

For those interested, the CME has a handy tool and more information, which can be found here.

Cross Currency Basis - Details

A cross-currency swap is a floating/floating swap where two parties borrow from - and simultaneously lend to each other an equivalent amount of currency denominated in two different currencies for a predefined period of time.

Let’s go through the sequences in more detail:

At the start of the swap, the two parties exchange nominal denominated in two different currencies, equivalent in value at the prevailing spot rate.

During the life of the swap, floating interest rate payments are exchanged, typically on a quarterly basis, to remunerate each party of its respective loan.

At maturity, the same nominal is re-exchanged at the same spot rate as was set at the start, which makes the basis swaps largely free from any FX risk.

The floating reference for each leg is based on the associated reference rate, typically a three-month deposit rate, in the respective currency. The market convention is to quote the spread against the non-USD leg. Thus, in a standard configuration, an investor would pay (receive) 3m USD LIBOR and receive (pay) the relevant 3m deposit rate in the other currency plus a spread.

Example:

A 10-year EUR/USD XCCY is quoted as -30 bps. This means the borrower of EUR funds will pay EUR rates -30 bps every three months in exchange for receiving USD rates flat from its USD loan. Inversely, the borrower of USD funds will pay USD rates flat in exchange for receiving EUR rates -30 bps from its EUR loan.

A deeply negative basis (-30 bps in the example) suggests an exacerbated demand for USD, as one party is willing to receive much lower interest rates on its non-USD loan.

A bit of terminology: Because the basis is quoted on the non-USD leg, paying the basis means borrowing the other currency (EUR in our example) versus lending USD while receiving the basis implies lending the non-USD currency versus borrowing in USD.

A common use of those swaps is to exchange floating liabilities in one currency for another. With the growth of international markets, cross-currency basis swaps are used to match the assets and liabilities of corporations exposed to foreign exchange fluctuations from international operations.

Basis swaps are also used extensively to swap corporate issuance back to the currency of choice after availing more favourable funding in a foreign market (credit spreads might be tighter in USD vs EUR). Additionally, firms that need foreign-denominated cash can raise the funds using a cross-currency basis swap. The supply and demand are based on firms swapping issuance or raising foreign funds, which drives the cross-currency basis spreads.

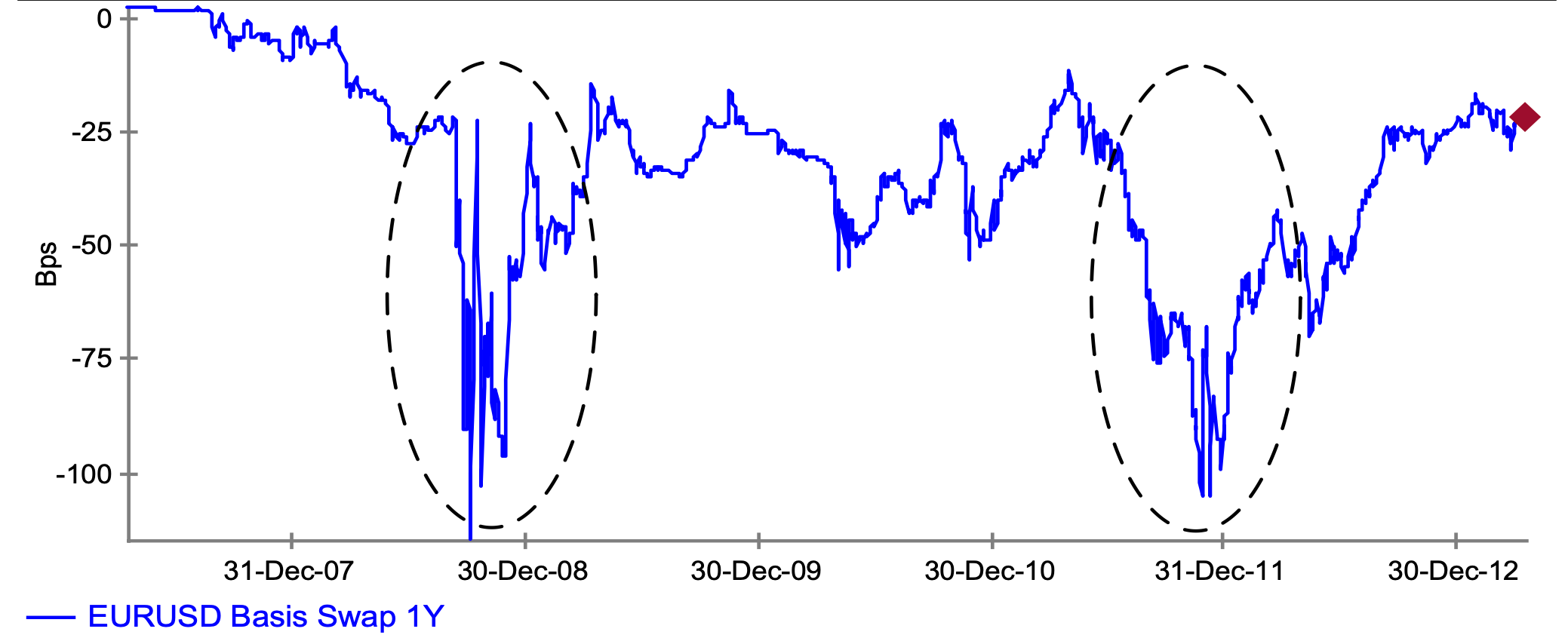

More often, though, you would have seen them highlighted as a pre-curser of funding stresses in the system. That is certainly one of the elements when looking at XCCY. Funding stresses and/or concerns over the credit risk of banks in one currency versus another can cause severe dislocations in basis spreads. A good illustration of this phenomenon was at the peak of the financial crisis when the demand for USD relative to all other currencies soared.

During this time, dollar funding in the interbank cash market became extremely limited as banks became reluctant to lend to other banks. As a result, the basis swap markets, as an alternative to acquiring USD funds, saw increased demand to receive USD funds in exchange for EUR, among other currencies. This excess demand drove the EURUSD basis swap spreads down to highly negative levels as counterparties were willing to receive lower interest payments in return for US dollar funds (see chart below)

Below is the JPY 1-year basis as a reference, and more recent history clearly indicates spikes lower when there were funding stresses.

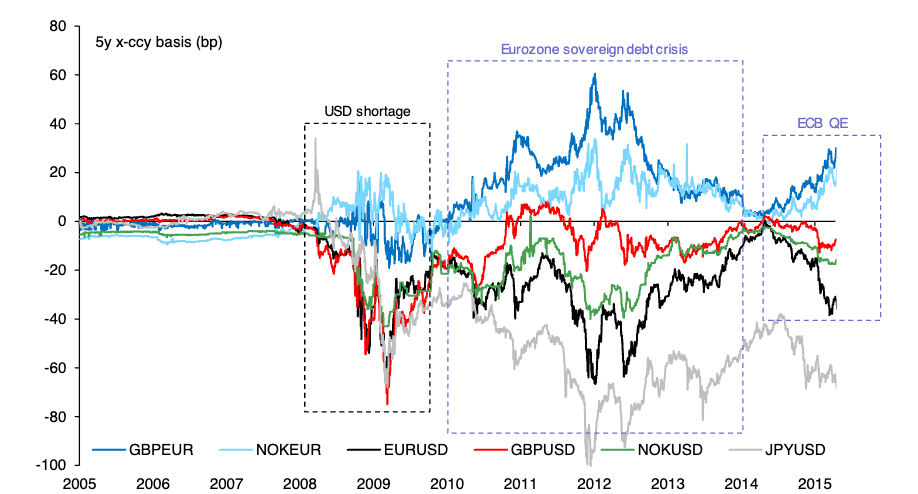

Aside from funding, stresses there are a number of other factors that are influencing the basis.

As you can see from the chart below, different factors have influenced the XCCY over the past years.

The most relevant factors are:

Foreign currency bond issuance

The net volume of foreign currency bond issuance between two regions is the traditional driver of basis swap markets.

Identifying seasonal patterns of net issuance during the year is an important factor and helps explain temporary shocks in the basis during the year.

When interest to pay the basis dominates (EU entities issuing in USD), the basis tends to tighten (turn less negative), as an example.

Credit risk premia and liquidity concerns

As highlighted above, spread widening due to banking stress and funding shortages globally will lead to a widening of spreads.

Historically, money market stresses will be visible first before they spill over to cross-currency basis swaps.

Sovereign risk premia

Sovereign CDS spreads are a good proxy to capture the degree of risk perceived towards a given country.

At the height of the European sovereign crisis, fears of a break-up contributed to a sharp widening of the basis as investors demanded higher compensation in exchange for lending their currency in exchange for the EUR.

Liquidity conditions

Increases in the ECB’s excess liquidity can reflect an increase in synthetic USD funding and thus explain a widening of the basis as excess liquidity rises. This makes intuitive sense as more liquidity generally cheapens the cost of funding in a currency as substantial amounts of cash flood the market and thus depreciate the basis as less interest is required to borrow.

Exchange Rates

The relationships between FX rates, the XCCY and funding cost differentials do not always hold; as before the financial crisis, there was no relationship whatsoever.

A widening of the EUR/USD cross-currency basis means that one needs to pay less interest to borrow Euros, reflecting a diminished cost of funding in EUR versus USD. A widening basis, therefore, reflects a depreciation of the EUR relative to the USD in basis terms.

As you can see, the cross-currency basis has some fundamentals to be aware of. It is, however, also a quite complex system which has plenty of drivers, with funding stresses being one of them.

Next time you hear someone using it as an argument for an immediate crisis, make sure you understand the logic above and that many other factors can drive the basis.

I hope this was useful; it was certainly for me as I had to brush up on some basics again. Remember, you never stop learning.

In your hypothetical example Shouldn't the CHF strengthen in 3 months compared to the dollar as it commands a higher interest rate

Thanks. Can you please tell the name of boa research for chart?