When To Buy Bonds 2

The sequel and update

Welcome to the second instalment and extension of the previous post from last December, which received some great comments. Thank you. Now that four months have passed, I thought it would be a good time to refresh where things stand and how things have changed. If you haven’t read When to Buy Bonds 1 yet, that’s probably a good way to start.

Ironically, we haven’t moved that much since the 7th of December, when the previous bond note came out. We are about five bps lower in 10-year Treasury yields. That’s roughly a 1% total return over the time horizon (mostly carry). Also, most of the capital returns came from quite a substantial rally over the past month following the mini-banking crisis.

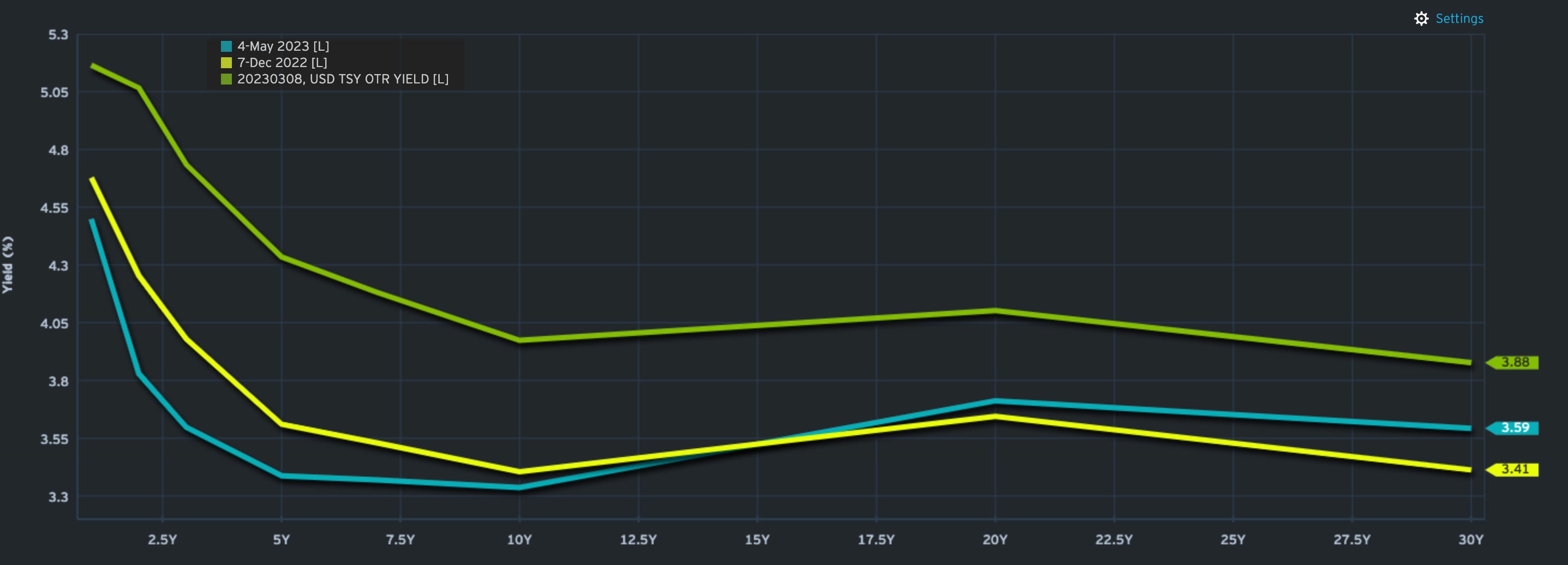

What about the curve as a whole? The below comparison shows the yield curve in yellow four months ago vs yesterday's latest iteration of the yield curve in blue. As you can tell, there was a slight steepening twist overall, with the 15-year point acting as the pivoting point. The green line is the yield curve on the day of Powell’s testimony to Congress and the corresponding peak in recent rate hike expectations.

Returning to the note from December and the accompanying tables, you can infer that even if we have seen March as the last rate hike in this cycle, the resulting total return of roughly 1% is just around where the median return (1.1%) settled in the previous episodes. My assessment then to wait for confirmation was not a bad call since we haven’t really left too much juice on the table. Sure, there were trading opportunities, but this post is aiming to provide answers from a longer-term perspective.

Following the second table, the conclusion (if held true) is that more information could be gleaned by looking at the evolution of certain segments in the yield curve, more specifically the 5-30s slope, which throughs around two months before the last rate. Similarly, 10-year treasury yields peak roughly a month before the last hike according to the table.

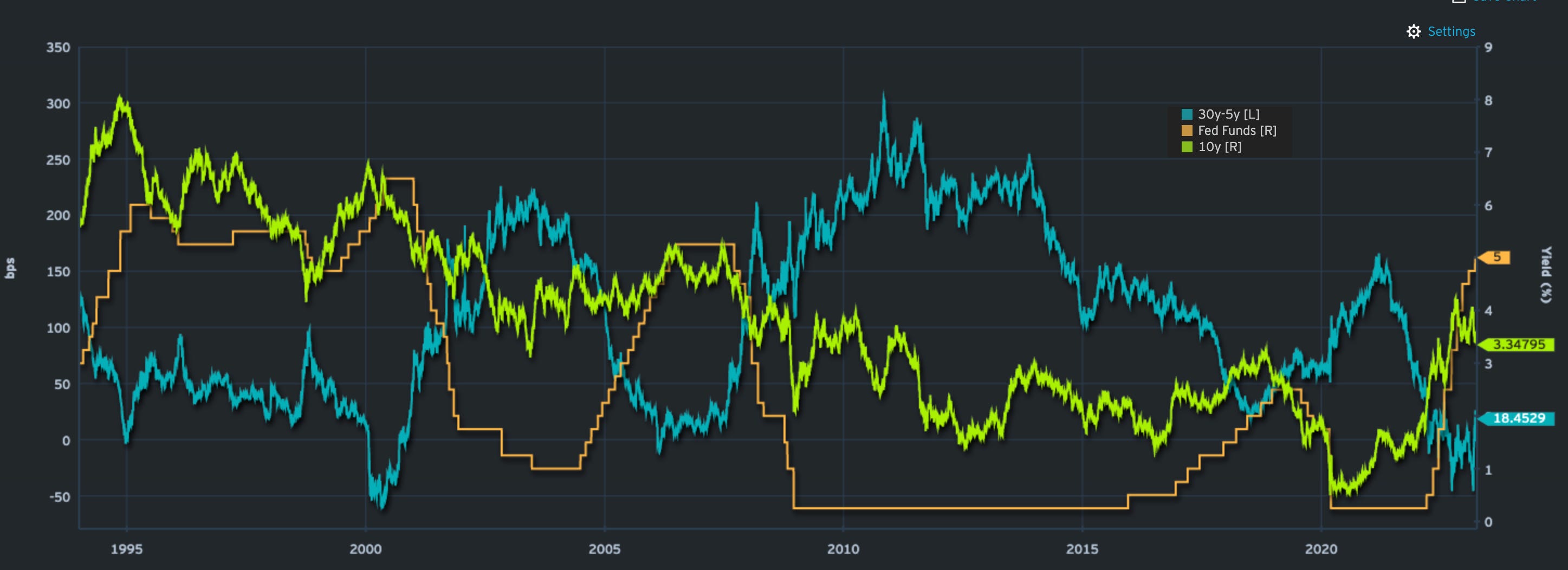

My preference for steepeners (5-30s) worked out well but was only helped by the recent bank troubles, propelling the front end nearly 100 bps lower. The curve flipped from -20 bps to +19 bps over the past few months after nearly touching -50 bps.

Looking at it in a longer context, the chart below shows the evolution of the 5-30s curve compared to Fed funds and the US 10-year yield since 1994. You can see the relative attractiveness for steepeners in the current environment, but they can be frustrating should the Fed indeed opt to keep a high rates plateau which we last saw during the 2006-2007 rate cycle (and completely different inflation dynamics).

As we are nearing the end of the current rate hike cycle, bonds inevitably are back in vogue. Pimco is screaming that bonds are back, but then, they are a bond house and slightly biased. The yield curve is screaming recession, and the Fed’s path is now anticipated to be cut short (again). SOFR futures have taken out 150 bps of front-end pricing over the coming year. That’s quite a lot of an insurance premium.

Comparing this to 2008, for example, as an extreme scenario (see chart below, using swaps) would indicate quite a significant premium. 2008’s “insurance” premium went as high as 225 bps, so another 75 bps ahead of what is currently priced.

Comparing this also in terms of overall yield curve shape, the below chart shows the various yield curves from yesterday and a month ago versus corresponding yield curves running four months and 2-months ahead of the Fed’s first rate cut (50 bps) on Sep 18, 2007. The same point, really; the current yield curve is anticipating quite a lot of easing compared to a period where inflation dynamics were totally different.

Where does that all leave us?

By any measure, the current bond market pricing is anticipating a recession and/or further fall-out of the cumulative effects of the tightening over the past few months, be this banking / CRE related or any further cracks appearing. Bonds are in vogue again as everyone anticipates the Fed (again) to roll over soon. Meanwhile, the inflation fight hasn’t been won yet, although forward CPI fixings are anticipated to fall further. Money multipliers are collapsing, which is a further harbinger of a disinflationary environment. I still like steepening trades in all scenarios. Am I buying bonds hand over fist? Not yet, but I would certainly use any meaningful backup in yields to add bonds to my portfolio. Will we see 4% handles in Treasury yields again? Wouldn’t it be great? Although the building narrative of disinflation/recession is probably hard to shake, I could envisage a scenario as we saw earlier this year where inflation is stickier and growth and labour market simply too strong to let the Fed take a breather.

It’s a tricky environment, so being nimble and flexible remains my main priority, given none of us (or very damn few) have been in an environment such as the one we are facing now. It’s never wrong to put your money into cash which gives you still relatively attractive returns, all else being considered. Not sure for how much longer. I will update you all if and when my view changes.

Thanks for reading, and as always, please leave a comment.

Paper Alfa