Ueda's Comet

Macro D Thoughts on the JPY & BoJ

This is a timely article by guest contributor Macro D, who called the JPY appreciation with nearly impeccable accuracy back in July. This seems to be quite a while ago, so it is worth hearing his latest thoughts on the matter.

You can find his BoJ post with a link to his other article that is connected to the subject below.

The BoJ , The Yen & Central Banking Chess

This is the third instalment of Macro D’s thought piece series.

Macro D

I try to imagine. In Japan, a man carefully examines the cover of the book that has kept him company for a few days: Hear the Wind Sing by Haruki Murakami. In 1979 (the date of publication of the book), Kazuo Ueda had not yet obtained his doctorate in economics from the Massachusetts Institute of Technology; he was just a student with high hopes; he certainly could not have known that forty-five years later, his decisions would have brought about such a scenario.

Preamble:

Last week, the Bank of Japan raised its policy rate to 0.25%, signalling its willingness to increase rates further. Markets are betting on two more increases in this fiscal year ending in March 2025.

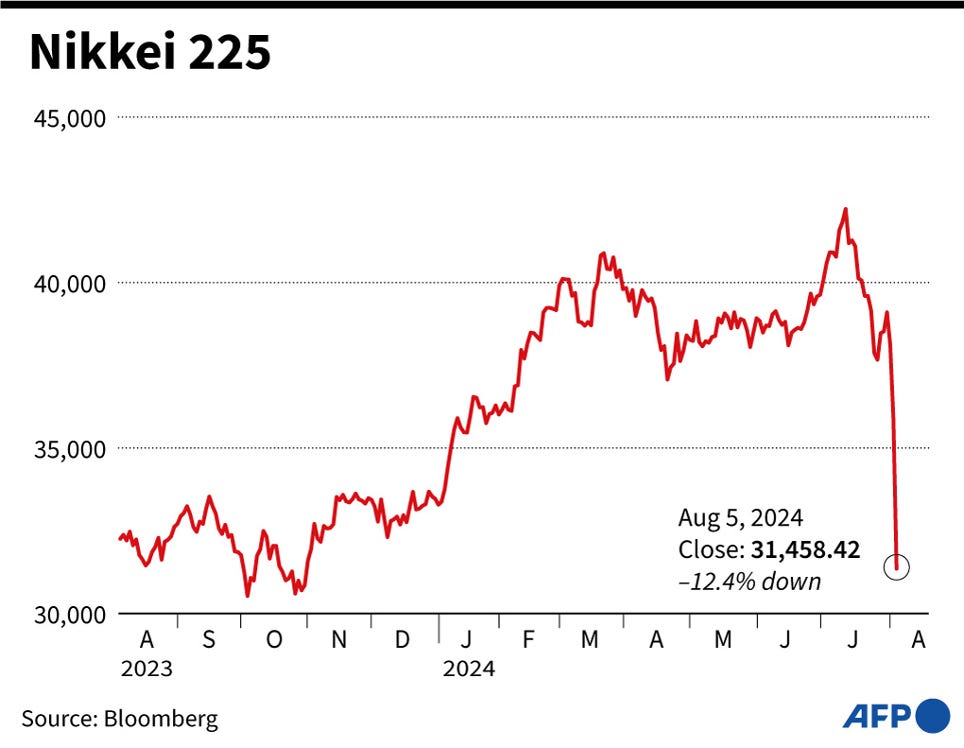

As I write, the Nikkei is down 12.4%, a clear indication that the financial landscape is shifting. In the Land of the Rising Sun, each individual component plays a crucial role in the financial system, with no room for the typical Western protagonism. This is a reminder of the importance of every participant in the market. Around our Ueda, the political zipper is starting to close. Japanese Finance Minister Shunichi Suzuki has just announced that the authorities are carefully and vigilantly watching the exchange rate movements, providing a sense of reassurance to the market.

This is the most significant one-day decline since “Black Monday” on October 19, 1987.

How did we get to this point? In order to answer that, I believe that we need to look at what is in the profit and loss statement of the BoJ. Japan is in debt of 20 trillion dollars in low-interest yen, but now the rate hike wipes out the carry trade. This has caused sudden fears for those who thought that the carry trade would last forever. The sudden rise of the yen has put the earnings prospects of Japanese industries, which are naturally oriented towards exports, in a precarious position.

This is the USD/YEN exchange rate:

As I write, the yen is up 3.7% at 142.87 to the dollar and is approaching its highest since early January.

What happened? This time, the yen's last gasp is not artificial (there was no direct intervention by the BoJ in its favour) but was favoured by the Bank of Japan's 15 basis point interest rate increase last week. The Japanese government is tied hand and foot to a stratospheric carry trade worth no less than 20 trillion dollars: well, if our Ueda decides to fan the flames, then this trade is destined to cause a hurricane of biblical proportions.

Let's take a look at what's cooking.