Party or Not?

Macro D Thought Piece

This is a great thought piece by the ever-thought-provoking Macro D. If he is right, his framework could have profound implications for the US Dollar going forward. There are big moves coming. I sympathize with his view. Regardless of your own bias, this is well worth your time to read.

Let's paint a general picture with the modest brushes I have at my disposal. The US stock market shows remarkable resilience in an economic context characterized by mixed signals. The S&P 500 has recorded an impressive increase of 16% since the beginning of the year. This performance is part of a broader positive trend, with the index closing in positive territory in four of the last five weeks. Even more surprising is the performance of the Nasdaq, with a gain of 22% since the beginning of the year. The Nasdaq is outperforming the S&P 500, which testifies to the tech sector's strength, albeit in a period of macroeconomic uncertainty. Indeed, this is not a healthy market but rather a coming and going of contracts signed by those who do not know what they want, do not know when they want it and do not know why they want to buy what they insist on buying. I wonder: 1) What drives this bull run during apparent economic uncertainty? 2) Where is all this enthusiasm coming from? 3) Who is this fabulous public relations expert who convinces everyone to join?

I can almost see Jay Gatsby[1] looking out the window of his beautiful mansion in West Egg, Long Island. He enjoys watching people have fun, but his fun is different. His is the silent peace of someone who pulls the strings of the party but never shows himself to anyone.

Well, who is pulling the strings of the party in these financial markets?

Suppose we avoid relying on gurus, fraudulent alchemists or second-rate magicians. In that case, the answer to these questions lies in investors' expectations regarding the future moves of the Federal Reserve.

To hell with prudence! Let's face it. There is now a new constant: the growing belief that any indication of economic weakness during the year will be addressed with an interest rate cut by the Fed. This new horizon feeds optimism in the markets and convinces investors to bet on unstoppable stock growth.

But let's get back to the initial reasoning: that long-awaited slowdown that should convince the Fed to cut rates.

Well, is this hypothetical next rate cut justified? Some data, in particular, suggests so.

Well, yes: For the first time since the pandemic, the consumer price index shows a negative figure (i.e. deflation). Let's get into the matter. If we look at the data carefully, we see that those who continue to believe in the predominance of inflation refer to the increases in the costs of health, car and property insurance, which in turn refer to three particular sectors: insurance, healthcare and the real estate market. Speaking of the real estate market, since sales are struggling, who should the supporters of inflation turn to to replenish the coffers of their inflationary beliefs? Obviously, to rents, but a new problem arises at this point. Real estate inflation (rent and OER) also decreased in June, going from 0.42% to 0.27%.

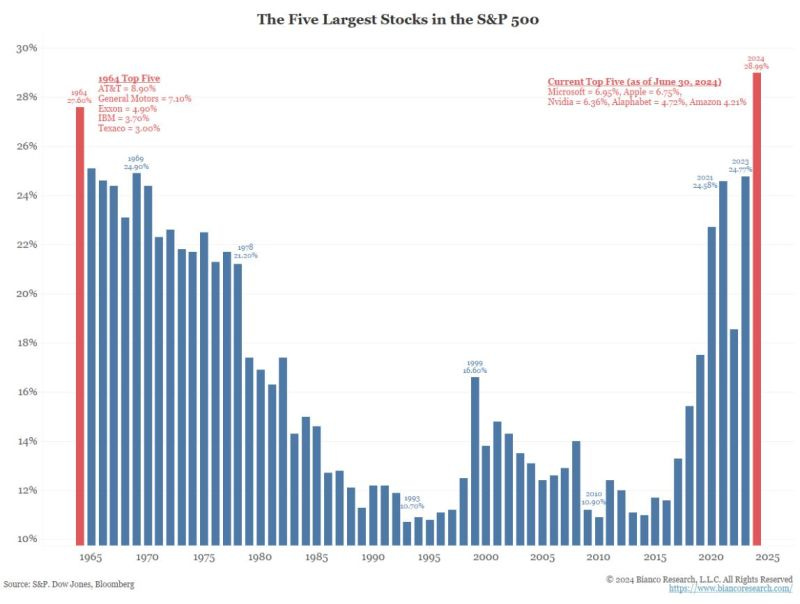

Let's look at some graphs.