Mid-Week Update

Post CPI deluge

The below-consensus CPI print sent waves across all asset classes. Core CPI rose 0.23% MoM in October, softer than the 0.3 to 0.4% range the street had forecasted, the consensus at 0.3% and the “whisper” number for an even stronger 0.4%. Shelter prices continued to moderate, with a 0.41% increase in owners’ equivalent rent. The biggest downside surprise was softer hotel prices, but even without softer hotels, details across the board were modestly softer.

While it is obviously more than welcome for policymakers to justify their policy on hold, I wouldn’t anticipate a fast trajectory to their 2% target any time soon. More on that in another post.

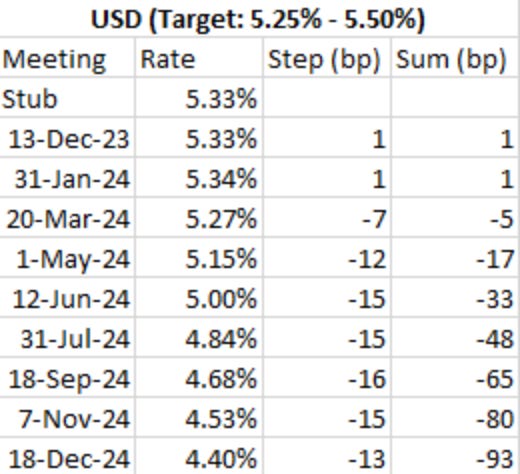

The following table is the STIR run post-CPI

Bonds have obviously taken the news positively, with 10-year yields rallying through 4.5%. Positioning, especially recent tactical shorts, could fuel a move further down towards 4.25%, with a 4-4.5% range, my base case, into year-end.

SPX futures have broken above the 4431 trigger level for CTAs to go max long.

USD has softened remarkably, with EUR/USD rallying through the 1.08 level easily, fuelling risk rallies in EM and high-carry positions.

None of this should surprise us, as the models have guided us to be positioned ahead of those moves.

Let’s dig deeper into what alerts have been triggered today due to this move.