Mid-Week Update

June 4, 2024

There are quite a few moving parts since the update over the weekend. The move lower in bond yields was mostly triggered by lower oil and commodity prices, which in turn sent risk assets lower. Renewed questions about an incoming economic slowdown have now raced to the forefront and occupy everyone’s mind as we are heading into NFPs later this week. The Mexican election fallout, while idiosyncratic, has reminded everyone how precarious carry can be. I think we are finding ourselves woken up by the market not to be too complacent. Other than that, at least for me, not much has really changed. It is interesting to observe and see where the weak and crowded positions are. That’s the main takeaway from the current consensus positioning unwind.

Let’s see what Macro D’s thoughts are before we go into what the charts are telling us as of late.

“The future enters us to transform itself into us long before it has happened.”

- Rainer Marie Rilke

From a macro perspective, what did we see that was significant in these two days?

The manufacturing PMI at 48.7% in May, down 0.5 percentage points from 49.2% recorded in April. This is the second consecutive month of contraction, and the reading indicates that production is contracting faster.

Meanwhile, consumer prices in Switzerland recorded a steady increase of 1.4 per cent year-on-year in May, the same rate as in April. The Swiss National Bank expects overall consumer prices to rise 1.4 per cent this year and 1.2 per cent in 2025. At its quarterly meeting in March, the SNB lowered its key rate by a quarter of a point to 1.5 per cent, deeming the battle against inflation waged in recent years to have been won for the time being.

The Bank of Canada (BOC) meeting, the European Central Bank (ECB) meeting, Non-farm payroll (NFP) and the European Parliament elections (starting June 6) are all scheduled for this week. Thus, this week's economic calendar will revolve around these events.

What fascinates me the most? I can't deny it. The data will be released on Friday, with the May report. The unemployment rate in April was 3.9%.

Before Friday, we will all observe the monthly report on private sector jobs (ADP) and the weekly initial jobless claims, which will be released on Thursday. What would be the consequences if these reports were to show a weakening of the labour market?

Could these reports potentially pave the way for a shift in monetary policy? The answer lies in the data. While waiting for the near future to reveal itself, let's cling to the past and its most authoritative voices.

Every concern, regardless of its origin, is worthy of attention. However, when a concern is voiced by someone with a proven track record of success, it demands our immediate attention. This is the case with Ray Dalio, whose words carry significant weight in the financial world.

Well, listening to Ray Dalio's words, I was worried, and consequently, I offered him my attention.

The founder of Bridgewater has expressed deep concerns about the political tensions and the consequences of high indebtedness on Treasuries. His assessment of the economic and political situation in the United States is particularly grim, with the escalating debt potentially triggering new geopolitical tensions and even a civil war.

For Dalio, the United States "is on the edge of the precipice." Given the growing divisions within the country, he believes there is a probability that more than "one in three" will end in a civil war; Dalio believes that the November elections will put democracy to the test. Does it still work well? Is it a form of government that is about to decline?

Dalio also said he was worried about Treasuries due to the high level of debt and the drop in demand that must cope with supply. International investors are seriously concerned about the size of the US debt and are turning their attention elsewhere.

Dalio's words are not a bolt from the blue; instead, they follow the line drawn by good Jay, who has openly declared in recent weeks that "the US is on an unsustainable fiscal path."

In short, whoever has ears to hear (in Washington) should listen.

Is Jay's warning not enough to stir action? Last month, the International Monetary Fund issued a global alert, stating that the escalating US government debt poses a significant risk to global financing costs and could potentially destabilize the world economy.

And yet, there's something I can't frame. The overall context tells the story of America's decline and shows an economic world that looks at the US dollar with ever greater suspicion.

So, I abandon the macro-theoretical context and embrace the micro-factual context. What do I see? For example, I see this.

But if investors shy away from the dollar and its debt, why is the dollar appreciating so dramatically against, for example, the yen? Let's hold on to the rope of reasoning that revolves around a fact: NOTHING IS AS IT SEEMS.

The yen is depreciating because Japan's currency granary is submerged by US government bonds, which (as we have said on various occasions) are considered by the markets (including the Chinese market) to be less and less attractive.

Question: but why are the much-maligned US government bonds considered less and less attractive?

Hypothetical answer: The colossal indebtedness, signed and countersigned in Washington, has forced the United States to get bogged down in a dark and gloomy path.

What do we get from all this?

The US dollar is now in a phase I call "debt currency transformism." What does this mean?

When it leaves the house, the US dollar wears a beautiful evening dress and perfect makeup that already allows it to be perceived as wealthy. Still, once the US dollar comes home, it opens the kitchen cupboard and finds nothing to eat because no one in the house has money to buy groceries.

So, the US dollar is depreciating (but silently and away from prying eyes). The world does not notice it directly because, at the moment in which this internal depreciation occurs (in front of the empty kitchen cupboard), the dollar itself manages to appreciate and maintain its value against other currencies (when it leaves the house and wears its evening dress and beautiful makeup).

The current situation is this: The dollar is depreciating away from the curious while appreciating in front of everyone.

But what is the trait union that unites the soul of the dollar that leaves home (and puts on its best suit) to that of the dollar that returns home (and sees that the kitchen cupboard is empty)?

Well, we have often and willingly named this trait-union in recent times. Its name is INFLATION, the one that is capable of depreciating everything without making any distinction between emerging markets and developed markets.

But between the two souls of the dollar (the one that depreciates away from prying eyes and the one that appreciates in full view of everyone), who is the one who will win?

It is certain that while these two souls divide the fee, one cannot help but notice that:

1) in flight, there is a specific raw material called GOLD:

2) The weakness of the GDP is now apparent.

Faced with such a global context, I cannot resist referring to the words of a human being who, between the lines, proposes a return to slowness in this disorganized and whirling world that toils inside a womb, continually in crisis.

"What sense does it make to talk about progress to a world sinking into a state of cadaverous rigidity?"

Walter Benjamin, Angelus Novus

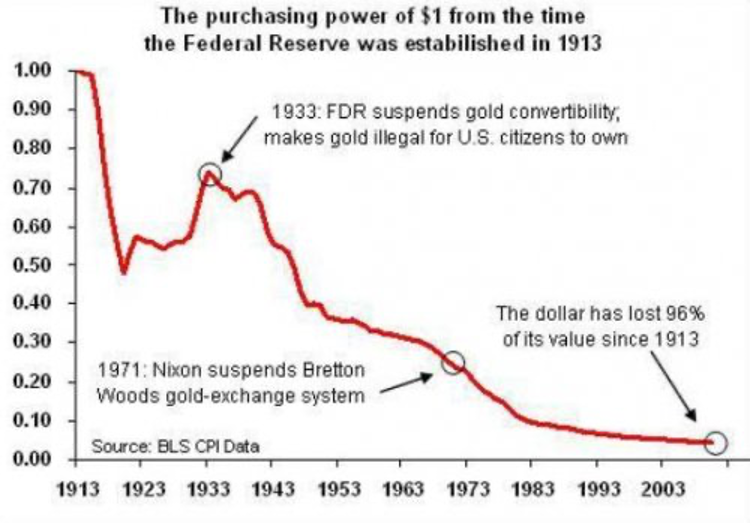

For now, let's leave it at that. Today, the United States cannot abandon the gold standard, the US government already did so in 1971.

So what will the gentlemen in Washington do?

to be continued, but let’s now focus on the most recent chart updates.