Mid-Week Update

October 8, 2024

They say that those things that multiply rapidly grow like mushrooms. Well. Based on this assumption, I would dare to say that in macro trading, ideas grow like mushrooms at any time and any latitude, and for us who are seekers, there is nothing else to do but arm ourselves with holy patience and crazy passion, and push ourselves to search for the most profitable ideas.

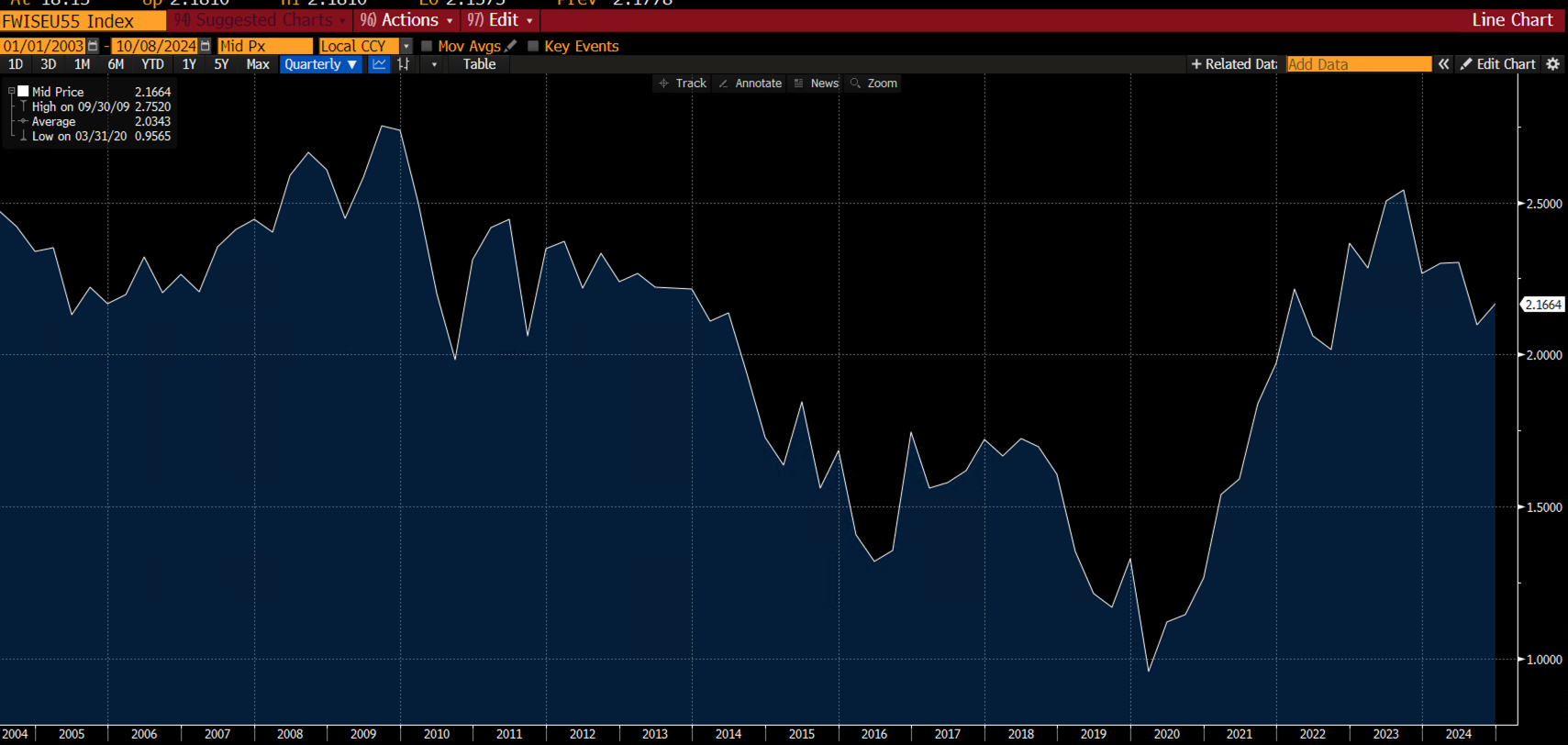

The macroeconomic agenda from 7 to 11 October 2024 intends to present us with some macroeconomic data of particular relevance for dear old Europe and the United States. Now, we will face the US inflation data for September and the minutes of the latest monetary policy meetings of the Federal Reserve and the ECB. As for the ECB, another interest rate cut of 25 basis points is expected on 17 October. ECB chief economists Philip Lane and Schnabel have begun referring to inflation as an abstract entity that has recently fallen faster than expected. Even French central bank chief Francois Villeroy de Galhau has gotten into this train of thought. Lagarde thanks. Below is the European 5y5y Inflation Swap, often mentioned by Draghi and it would seem we are basically running it close to the target.

After the rollercoaster of the weekend that we left behind, Monday began with the American stock markets taking a breather, accompanied by the same sleepy temperament as China, which is concluding its 75th-anniversary celebrations at the beginning of this week. Europe started over from its locomotive, and it could not hide the shortcomings that had characterized it in the last period. German factory orders fell 5.8% in August, even worse than expected. The general context accompanies the Teutonic people towards spelling a somewhat melancholic word: RECESSION. Below is the economic surprise index for the Eurozone.

At this moment, the short-term fate of the euro is entirely anchored to the vicissitudes of Berlin and its surroundings. All the other nations of the euro area (even if added together) are not capable of causing currency earthquakes like those that could arise from a hypothetical officialization of the German crisis. And now, let's put the American cards on the table, too. Jay has painted a picture that no further 50 basis point cuts are expected in the coming months, but instead, two 25 basis point cuts, one during the last meetings of the current year. I would not bet on them, not even on these two cuts. I think Jay is now (only apparently) in the "repentance phase". Someone has pulled him for the jacket, and he has allowed himself to be persuaded, but in terms of this persuasion that has won Jay, I see the kind of monetary policy cunning that perhaps the markets have not yet sensed.

Jay recently opted for a sharp cut of 50 basis points because he knew that from that point on, he would only cut rates at the end of the year. He thought one large cut was less damaging than multiple minor cuts. He knew it. We are in the land of "neither fish nor fowl", so taking an uncompromising monetary stance that goes all in on one path would mean behaving like that gambler who behaves that way because his doctor has just told him he has only one month to live. So, what does he care? Neither Powell nor the American economy are in that situation. Right now, every scenario deserves to be taken into consideration, so I can only explain the extent of the latest cut supported by the chair with the simultaneous presence of an underlying philosophy that contemplates this 50-bps cut within a scenario in which we will not see any other reductions between now and December. And then, let's tell it all. I have not seen the corpse of inflation. Now, karma pushes for the soft landing rather than for the recession, but if you look closely, how many visions has this phantom financial karma shown us? So many, so many. Now, everyone is looking at US inflation on Thursday and Friday. I think Jay doesn't like all these ups and downs, all this carefree rollercoaster, so I tend to believe that between now and Christmas, he intends to re-establish a situation in which the principle of "we are dependent on data" does not turn into the fuse capable of creating fires and flames in alternating phases.

Let's look further. The New Zealand central bank may cut rates by half a point at this week's policy meeting, which could benefit the New Zealand dollar. Still, I expect a small rally.

Let's go to the Land of Albion: the pound has been put on the ropes lately because Andrew Bailey has hinted that the BoE could be "more aggressive" in cutting rates. I believe it. But what set off the alarm bells of my attention? Bailey's intentions were utterly gratuitous, not provoked by any communication scenario that put him in a tight spot; in short, I had a clear impression that he expressed certain words because it was his deep and deliberate intention to express those words that denote a fundamental vision.

For this reason, I would start building a short position on:

GBP/USD :

Take profit:1,20 Stop Loss 1,33

GBP/NOK :

Take profit:10,50 Stop Loss 14,50

GBP/INR:

Take profit:88,00 Stop Loss 113,00

Please note that these are just my ideas and shall not constitute investment advice (see disclaimer further below).

As for Switzerland, I confidently maintain my essential vision: in currency terms, I believe that at this historical moment, part of the trading plan should be dedicated to the possibility that Martin Schlegel intervenes (even heavily) to calm the value of the Swiss currency.

And now, let's take a look at the Land of the Rising Sun. The Nikkei 225 has reached historic highs in 2024, and some signs point to the end of long-term deflation; good old Kazuo Ueda does not commit himself and remains on the river bank to contemplate the currency evolution caused by the moves studied in his buen retreat in Tokyo. Mr. Ueda is aware that from now until Christmas, the yen's yields will depend not only on his monetary policy but also on the US’s, and at the same time, he understands well the whys and wherefores of Powell’s moves and those he is about to make. I have been following the spiritual footsteps of good Kazuo and Jay for months, so I maintain my view on the dollar/yen exchange rate, which has yielded excellent results. In short, the dollar will continue to recover against the yen between now and Christmas.

And now, a look at Australia. The minutes of the latest RBA board meeting show that the central bank does not intend to loosen its grip on inflation. Therefore, it wants to keep interest rates at the current 12-year high until it is sure that inflation is heading towards the target. The RBA is, thus, distancing itself from the FOMC's monetary move and not following in his footsteps. Why? Because here, inflation and the labor market are both stronger than elsewhere. The RBA highlighted in the minutes that core inflation is "still too high" and has fallen "very little" quarterly compared to the previous year.

I prefer to close by alluding to the well-being that peace can bring, but events force me to refer to the tears that war brings. Israel's reaction to the attack on Tehran is written in the stars. Oil is on the launch pad, with Brent returning to almost the threshold of $80 a barrel. The $100 target doesn't seem that far away.

Let’s now look at some updated charts and alerts that have been triggered since the start of this week.