Has QE altered the power of rate hikes?

Thoughts and Consequences

David Zervos is one of my favourite macro observers who works for a large financial institution, as he typically offers non-consensus views. While some might call him crazy, his macro views usually have some decent, actionable risk-reward characteristics.

His “Spoos & Blues” trade was actionable and profitable for most of my trading history from 2014 until 2018. The strategy, which is very closely related to risk parity, involved buying S&P futures (vol-adjusted) and the vol-adjusted equivalent amount of “Blues”, which is the front-end future (back then EuroDollars) four years out, which was highly correlated to 5- and 10-year bond futures. As a reminder of the colour coding, the CME colour codes the first year as “whites” and the second year as “reds”, with the third and fourth years being “greens” and “blues”, respectively.

Ultimately the Spoos & Blues trade stopped performing just as we entered rocky waters over the past 18 months. You can guess why risk parity strategies underperformed. See the chart below.

His latest thesis, though, I find quite interesting. Already earlier this year, he stipulated why the steep rate hikes showed only little impact on growth and why there wasn’t more blood and cracks occurring. It was intriguing to me as I was and to some extent still am in the camp that rate hikes ultimately expose hidden leverage in the system, which it always had done previously.

His piece from earlier this year researched the thesis as to why rate hikes and QT, ironically, provided a huge unintended stimulus. His analysis involved looking at the combined balance sheet assets of the Fed, ECB & BoJ, which stood at around $ 22 trillion. He assumed a 10% mark-to-market “loss” over the last year. This would imply a loss of $ 2.2 trillion which has been shielded from the private sector. QT, in the form of asset sales, should have happened before raising rates to push the losses back into the private sector, but this has not been the case.

Below, you will find the key excerpt from his piece:

“.. in the old pre-QE world, an individual, a company, or a municipality that locked in a loan with term funding would win, while the holder of that loan would lose. For example, every US household that gained from locking in a low mortgage rate for 30 years had those gains offset by losses at a bank portfolio, a pension fund, a hedge fund, or any other holder of the loan in the private sector. In the old days like 1994, the gains and losses in the fixed-rate term lending markets offset one another in the private sector – it was a zero-sum game for the economy as a whole. But today, in the post-QE world, the loss side of this zero-sum game is not being realized in full. The central banks have become a socialized buffer for large portions of the losses, thereby creating a one-sided private sector stimulus effect from the rate hikes. That’s why both financial markets and the economy have held up so well after this tightening.

Trillions in stimulus have gone to fixed-rate borrowers across the globe, while trillions in unrealized mark-to-market losses have hit the central banks, with no immediate negative economic or financial-market consequences. There are no shareholder revolts or forced sellers after central bank losses. No CEOs get fired; no valuations collapse. This is a huge, and highly unpleasant, unintended consequence from QE. It implies that monetary policy tightenings are now much less potent than in the past. Before, a central bank could blow things up and slow down the economy with just the flick of a 300bps switch. But now, QE has become a monkey on the back of the inflation-fighting process, hampering the process of “getting the job done.” Of course, the obvious implications are that that policy will have to remain tighter for longer, and possibly go higher than previously thought. Or – another way to think about it – central banks just haven’t tightened as much as you think.”

There you have it. In short, due to massive stimulus, people and corporations were able to lock in very cheap nominal rates while QE safeguarded the losses brought upon interest hikes as a bulk of the assets are still sitting on the central bank’s balance sheet, which is immune from mark-to-market losses. The consequences were clear; the Fed would keep on hiking as rate hikes pass-throughs were less powerful than previously thought.

The piece, of course, was written before the SVB collapse in March and, ironically, at that time, could have been immediately shredded. In hindsight, however, the mini-banking crisis only reinforced the safeguarding principle by the Fed to immunise losses as liquidity was being pumped back into the system.

Zervos summarised the SVB collapse in a follow-up note as follows:

In the near term, the road will surely be bumpy. The regulators made a huge mistake in letting duration gaps widen to SVB-type levels. But I do suspect this type of rate risk mismanagement was not endemic in the broader financial system. Lots of seasoned CFOs and bank treasurers understand how to hedge MBS. This risk has been around a long time. The more savvy institutions will come through this much stronger, and those with either juniors in risk management or cavalier attitudes toward interest-rate risk will get swallowed. Capitalism will still work!!

So far this year, his thesis holds true as growth surprised to the upside while there are no large cracks (yet) appearing.

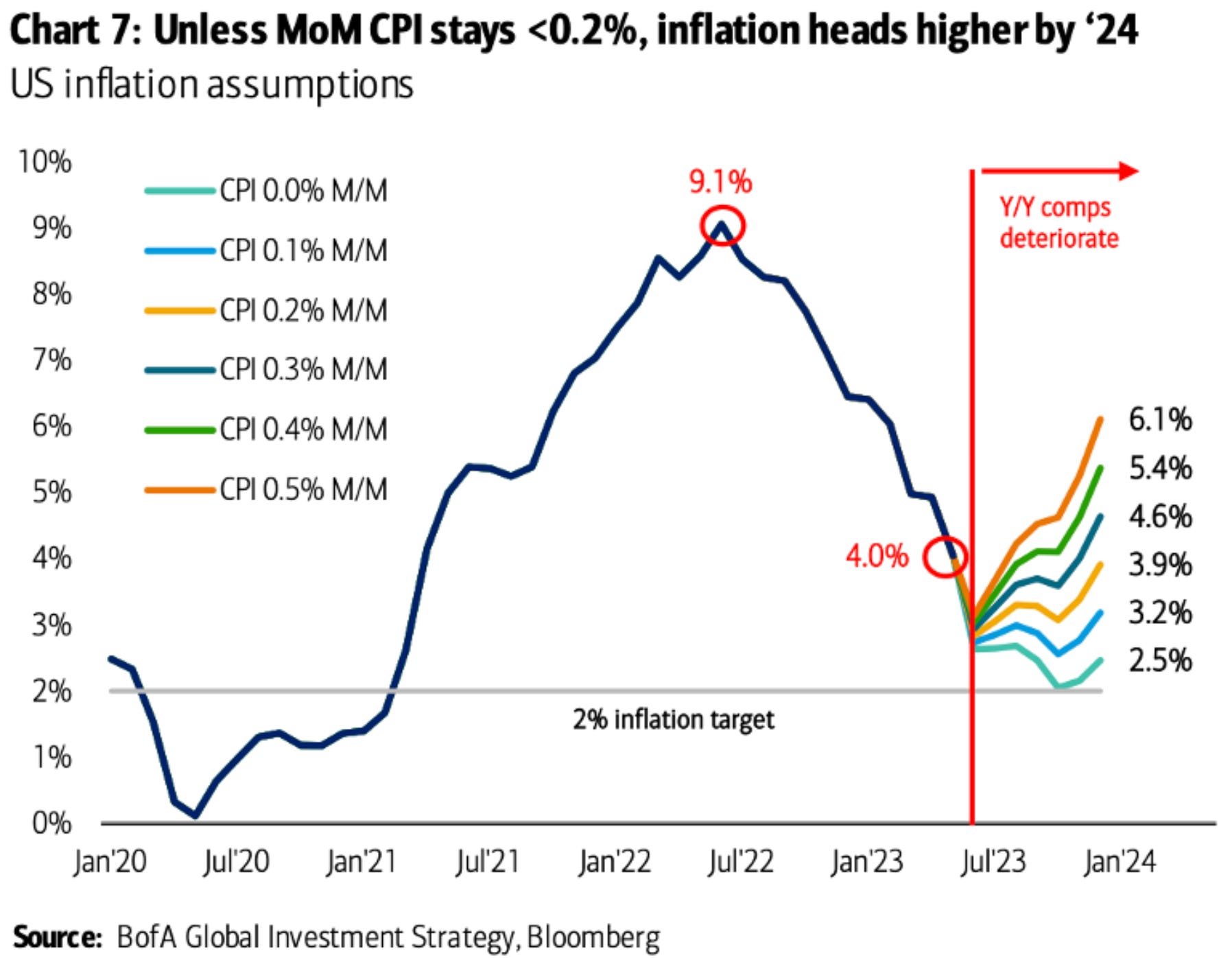

As to his views for the second half of this year, he continues to argue that rates need to be adjusted higher. The Feds’ year-end target for PCE ex-food and energy of 3.9% is consistent with hiking another 50 bps from current levels. To hit that number, we would need roughly 0.25% of monthly readings on average over the next six months.

Looking at current economic momentum, he thinks that bringing PCE core further below 3.9% by year-end is a tough task which would necessitate for the Fed to hike more than the already pre-announced 50 bps into the end of this year. As a result, he thinks the runaway equity euphoria is, on balance, misplaced as he favours high-yield credit (blue line below) as the best risk-reward at the current juncture.

Yes and thank you for the great question. All valid points but you’re getting paid 8% with a spread of 350 bps to treasuries and an effective duration of 3.5 years, so below 5 year maturities. You’re long front-end risk with massive positive carry and an option for continued nominal strength and no recession. If that breaks front end rates rally while spreads widen. Unless a disastrous recession it’s a good r/r trade.

I think the thesis makes a lot of sense. Central Banks are bag holders for mark to market duration losses and for Fed at least what does it matter. The trade though, doesn't make sense to me? Isn't High Yield particularly risky as higher rates continue to apply pressure to that very asset class where the trade is sitting? Shouldn't high rates (as long as they persist) drive the businesses which tend to find themselves in the high yield bucket deeper into distress as they tend to find themselves refinancing into worse conditions? At some point won't those hy spreads blow out(taking the trade with them )?