Friday Thoughts

Of Correlation and Volatility Spikes / Macro Thoughts on Rates

I hope you all had an enjoyable week. I mean, it had a bit of everything for everyone. Some epic football (soccer) matches followed by another war intermezzo mid-week. It’s July, anything goes.

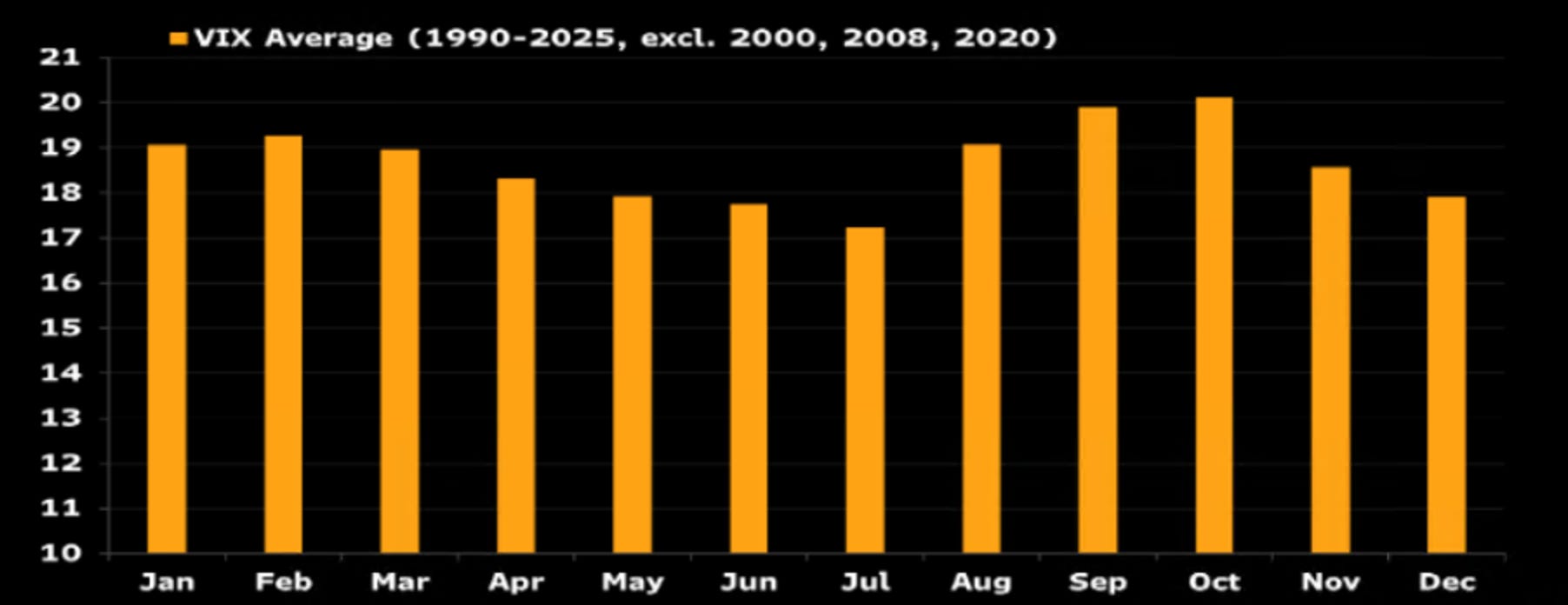

London was gripped by another heatwave, but that doesn’t matter as everyone is hyped for tomorrow’s game against Norway. The tennis is on, people are looking to depart on holidays - should we be surprised that the Vix exhibits seasonally lowest readings in July? It shouldn’t.

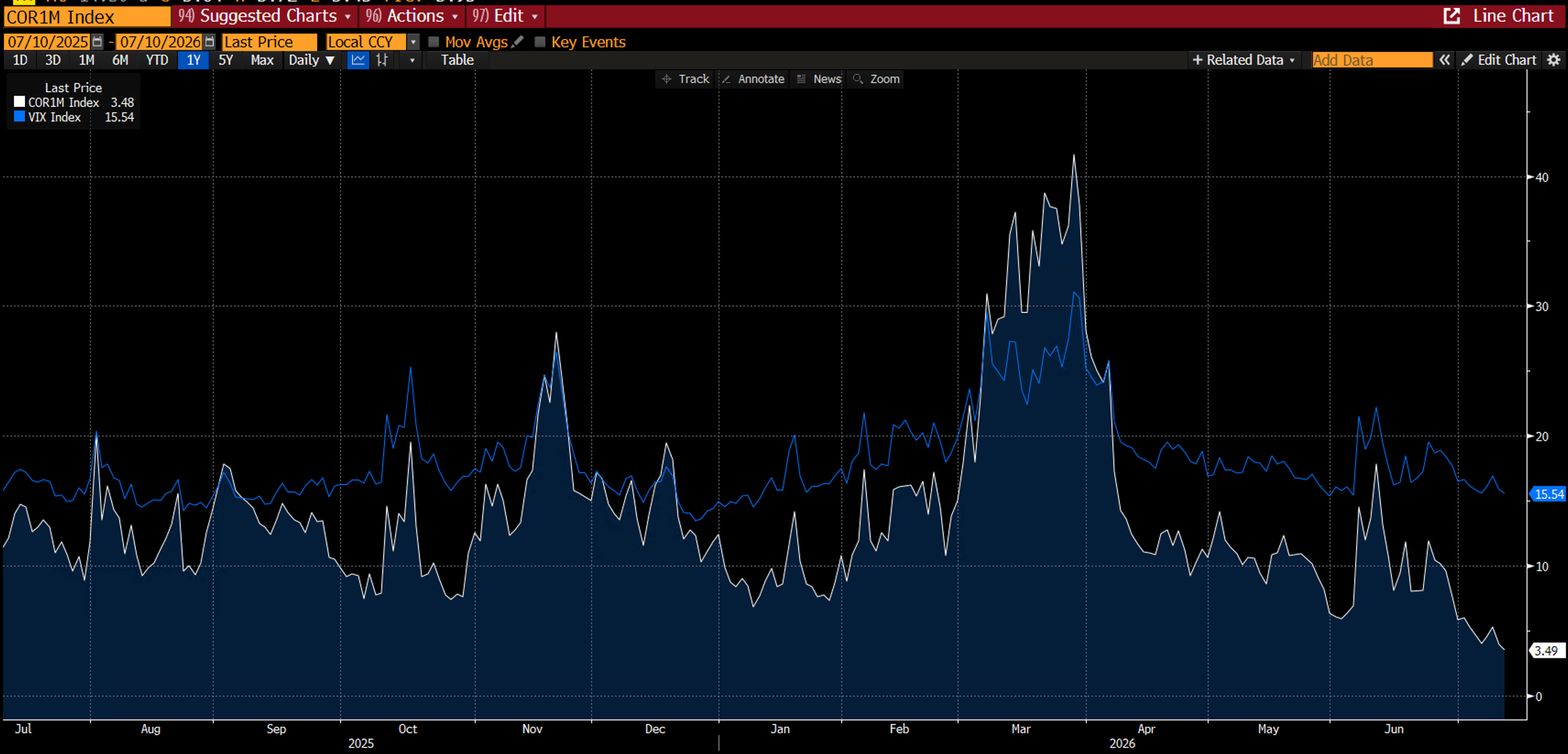

I find it interesting, however, that implied correlations are at new lows. Below you see the 1-month implied correlation and the VIX in blue.

For those who don’t know, the VIX measures how much the S&P 500 index is expected to move. That index-level vol is a function of two things: how much individual stocks move and how correlated those moves are. If every stock swings 20% but in random directions, the index barely budges. If they all swing together, the index explodes. The CBOE Implied Correlation Index captures that second component — the market’s expectation of how much stocks will herd.

The 1-month implied correlation (COR1M) is currently printing around 3.5. Meanwhile, single-stock implied vol (VIXEQ, see chart below) sits near 50 while the VIX is under 16. That spread — now at record levels — is the dispersion trade in full bloom. Funds are short index vol and long single-stock vol, profiting from the divergence. The trade suppresses the VIX mechanically while individual names gyrate wildly underneath.

This matters because extreme lows in implied correlation have consistently preceded VIX spikes. The mechanism works like a coiled spring. Correlation drops to extremes. Dispersion trades pile up. Then a macro catalyst hits, and stocks that had been moving independently start to correlate again. The dispersion trade unwinds. The mechanical bid under the index vol evaporates. The VIX doesn’t drift higher. It jumps.

July 2024. COR1M was at similar extremes. What followed was roughly a 10% drawdown in the S&P and 16% in the Nasdaq over 3 weeks as the yen carry trade unwound and correlations spiked.

One more detail. The cushion between implied and realised vol — the premium option sellers rely on — has compressed to almost nothing. On a recent session, the implied actually printed below realised. That almost never happens outside of stressed environments.

Falling correlation doesn’t cause VIX spikes. But extreme lows are the dry tinder. The match can be anything. With the Iran conflict seemingly unresolved, oil rising again, and inflation dynamics still in flux, the question is when, not if. When correlation snaps back from these levels, the low VIX will look like the mirage it was.

The SOX Index chart below seems to be signalling that some volatility is still to pass. I am closely following the moves and preparing to engage.

I have more thoughts on equities, rates and macro markets below. As always, subscribers have full access to our range of models and strategies at pa-globalmacro.com. It features a dashboard that is updated daily and linked to the daily signal alert system, which scans reversals and momentum shifts across the tracked universe of roughly 200 securities we are currently observing.

For current members, please note that to receive email notifications, go to your account settings and select which reports you wish to subscribe to.

In addition to some further macro thoughts, we have my loyal friend Macro D opine on the week just gone by and how this influences his risk-taking in Global FX markets. Annoyingly, his PC crashed over the weekend due to a corrupted hard drive, which seemingly cannot be rescued. If any of our readers has a good suggestion on how to recover some files, etc, please let us know below! Amazingly, Macro D still found ways to convey his thoughts to us. Where there is a will, there is always a way!

Wishing you all an enjoyable weekend. For football fans, it will be a fantastic few evenings and early mornings. If you are undecided, give it a cheer for England! It’s so coming home …