Friday Thoughts

Current Thoughts / FX Vol too cheap / Long Weekend ahead

Sometimes, there is just not much to say. This week has flown by, and aside from well-discussed yield break-up fears, actually not much else has happened. Good news, right? We are once again waiting for some sort of “deal” for clarity. On Thursday alone, I counted four different stories and then U-turns. It would seem we now have multiple parties who might or might not use the power of “sources” to move markets. I shall leave it at that.

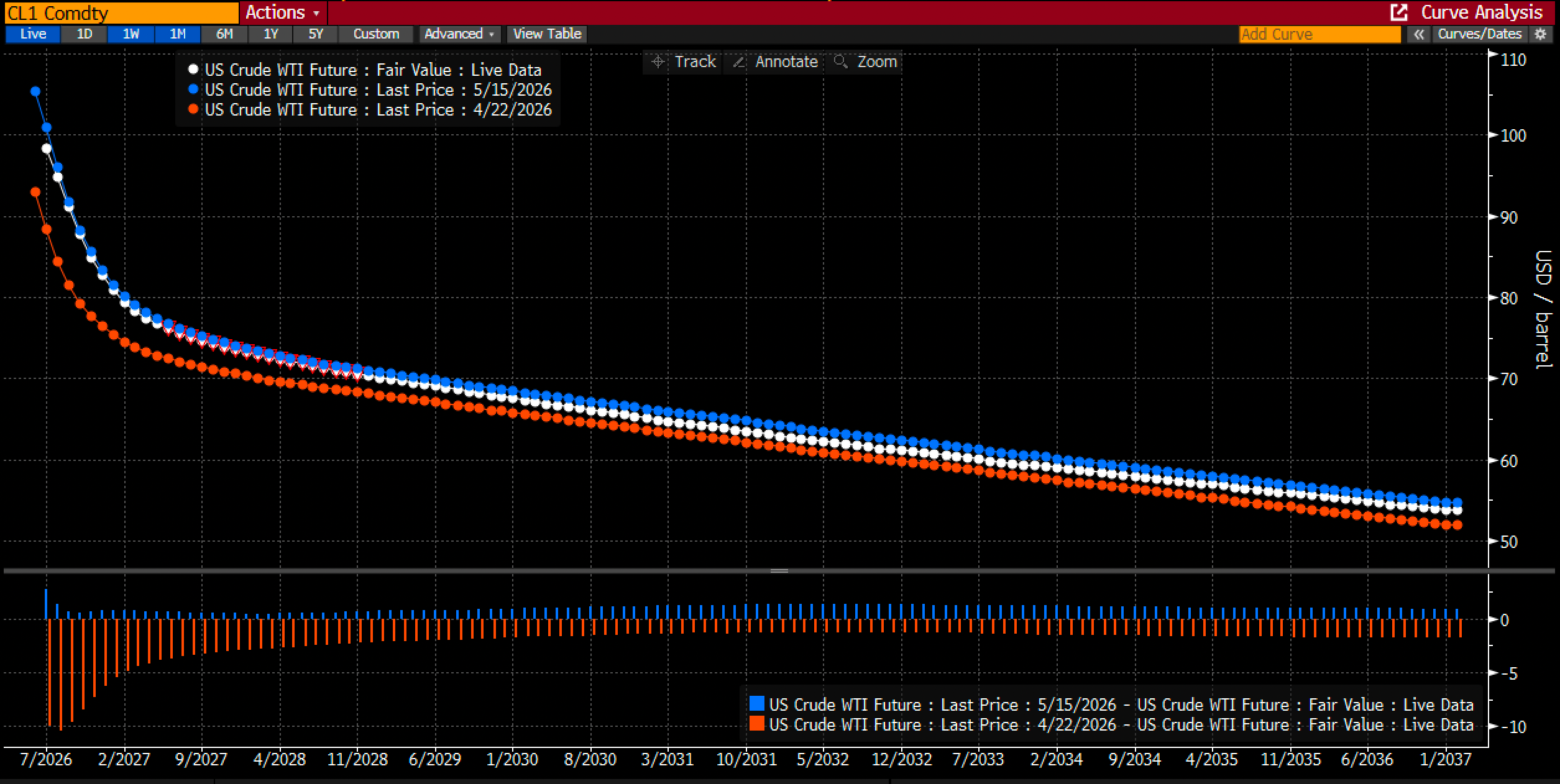

How are we meant to make sense of it? When confronted with this amount of noise, I refer back to checking the price action being exhibited. The first crude future shown below would still indicate relative tightness, with little signal of an immediate deal being struck.

As for the curve, backwardation remains in play, with little change in its slope over the past week and month, still indicating normalisation down the road, which gets stretched every day.

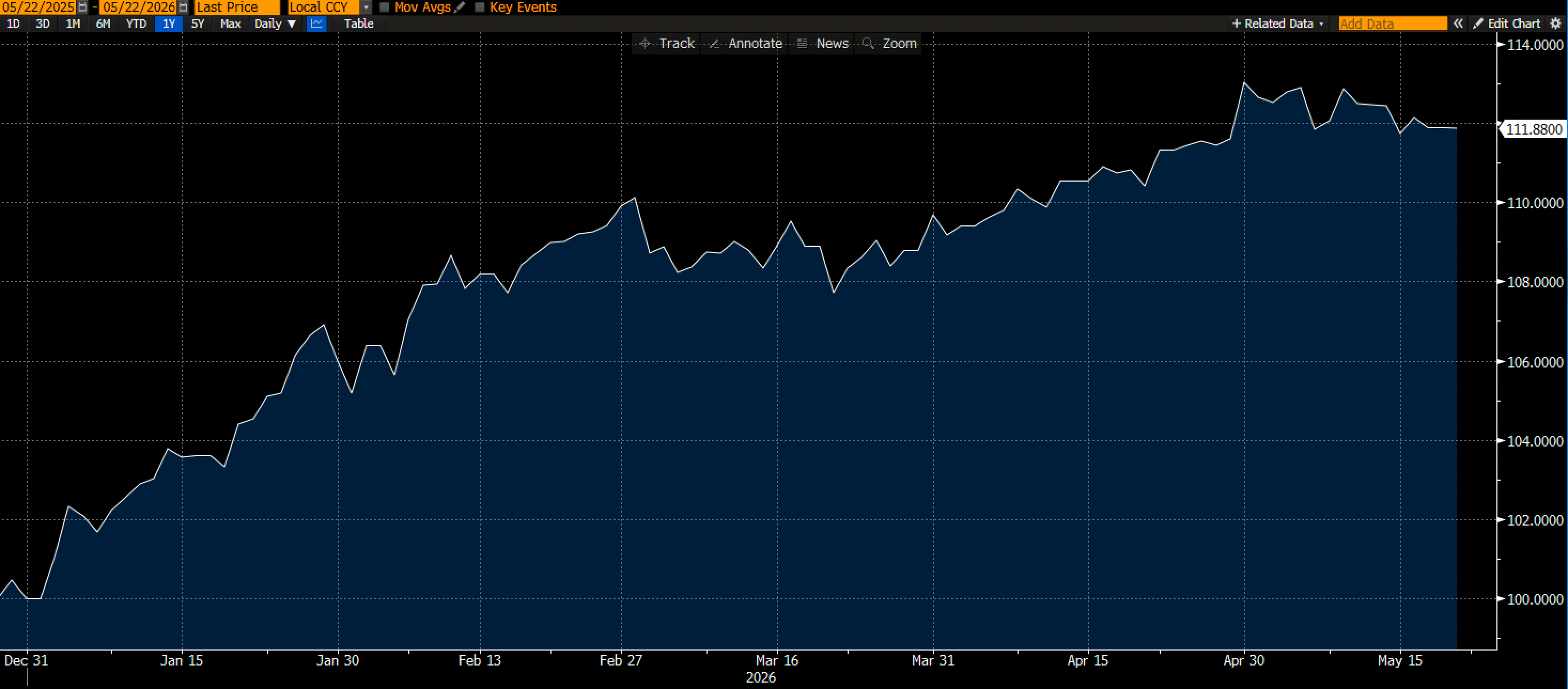

Yields were the talk of the town this week, with US 10-year yields nearly touching 4.70%. Our models and allocation tools disliked bonds for most of the year. This week, subscribers were alerted to a possible reversal from the highs, which is now playing out.

Even politically-inflected Gilts (UK 10-year yields) have staged a comeback, with yields rallying nearly 30 bps from recent highs. This was helped by weaker inflation readings and softer economic impulse data during the week.

Much of the global bond sell-off was once again partially driven by Japanese government bonds and their curve (5/30s), which reached the top end of the recent range (5/30s) before reversing sharply.

The reversal does not mean that the bond sell-off is done. For those of you who know how my reversal indicators work, know that this usually does not alter the prevailing dominant trend.

SFRZ6 (Fed year-end expectations) has slowly moved back toward the March lows, with markets now pricing in a fine balance between a Fed on hold and inflationary pressures. I would think that is fair, just as Warsh is set to begin his tenure.

This re-pricing has also given the Dollar a bit of a backing as relative monetary policy rate dynamics take hold. It was particularly interesting to see how EURUSD couldn’t bounce on good geopolitical news, with general European data disappointing and further accentuating the relative rates play, which I think many are now looking to engage in. This is the macro theme I am going to be following from here as some economies have seemingly lost a bit of economic momentum relative to the US. FX implied volatility is still at the lows, so I think there are going to be great opportunities, which I’m sure Macro D’s FX book is going to engage in.

As for the 2026 portfolio, we are still tracking around 11.9% YTD in USD terms, with May so far not giving us much action, as some of the tail-risk exposure holding us back, but that’s ok as it helped us outperform during March.

As mentioned above, subscribers were alerted about the reversal in bonds during the week. This is part of the offering now on our dedicated site at pa-globalmacro.com, where all models, dashboards, and the entire chart book are housed.

For those interested, I have put together a brief summary and a guide for subscribers at the following link.

If you are a subscriber, simply use your email to access the full range of the current offering and any new tools in the release pipeline.

If you are curious about the offering, why not try this place for 7 days? Hit the button below and enjoy.

Let’s now read Macro D’s latest thoughts and FX trade implications

Wishing you all a fantastic weekend. Temperatures in the UK are soaring just as we are enjoying a bank holiday Monday. I am going to listen to Waller’s speech today, which should prove interesting as he usually a good guy for the commitee as a whole.

Keep in mind that it's a US holiday on Monday alongside a UK bank holiday. So have a great rest and enjoy!