Friday Chart Book

January 17, 2025

Bonds are back! What sounds like a fantastic headline has to be taken with a pinch of salt. Let’s look at the chart below, which shows a nice 20 bps rally from the top, but it is premature to talk about a massive turnaround.

What has happened? Wednesday’s inflation data came in softer, especially in the run-up to the higher end of the expectations distribution. Remember that the market had started to price in a distinct possibility of hikes coming back, especially in the options space. Using the very clever tool from PricingMonkey, which shows us the vol skew for the SOFR Dec 25 contract. What has basically happened is that volatility has been crushed as markets have priced out the probability of hikes, which helped bonds rally.

On the day, interestingly, the 2-10s curve was flatter (see below), indicating to me that the bond rally was mostly due to position squaring, especially from the trend-following crowd.

Can bonds rally further? Yes absolutely. It was interesting to see Thursday’s really strong US retail sales pass, and bonds, after consolidating a bit lower, continue to rally again. This would further suggest that there is some ongoing short-covering. For a more comprehensive view, I would suggest waiting for this weekend’s allocation model and whether it has switched back into bonds.

Stocks took the bond move mid-week as a reason to rally. We bounced nicely from the 200 line (yellow in the chart below) but then stalled on the 50 resistance. Interestingly, Thursday’s bond rally didn’t help equities to close on a stronger footing. Friday, however saw a further strong US stock rally ahead of the longer holiday weekend.

We are now all awaiting Trump’s inauguration as most of the macro data is behind us. The macro consensus is still firmly set, and data is supporting the strong USD trade for now. Bessent’s testimony was pretty straightforward. He is a good man and chooses his words wisely. I think he is very strategic and has his own mind as to how best to tackle things on the tariff front. Whether Trump will align with him is a tough call. There could be a clash of egos looming.

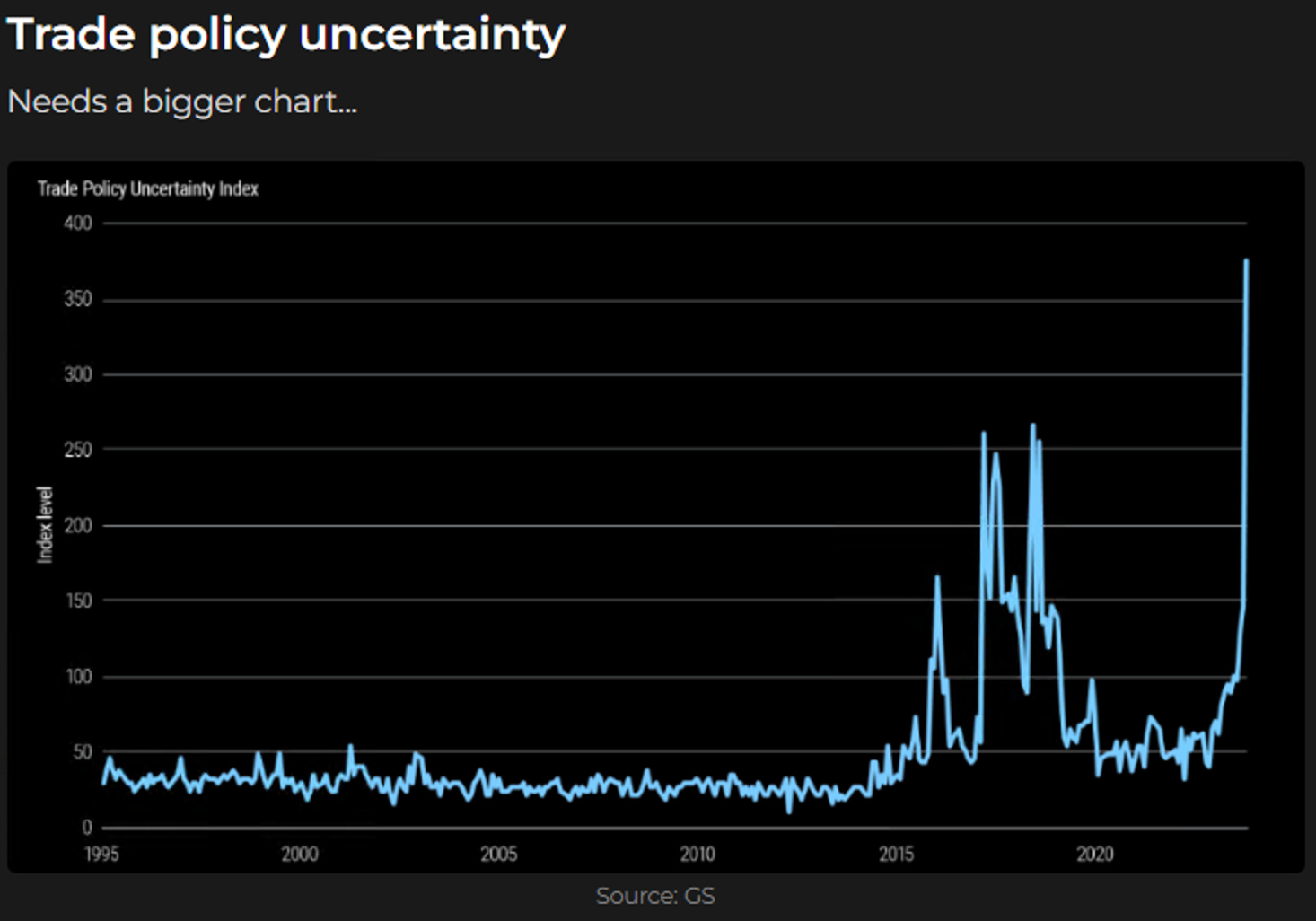

Trump declared on Friday that there are strategic channels of communication between China and the US. “President Xi and I will do everything possible to make the World more peaceful and safe!”. I'm not sure what this really means, but the signalling would suggest that some sort of deal has been struck. This caused the USD to initially sell off, anticipating less aggressive tariff policies potentially. This might be all just Trumpian communication style, of course. What if it’s true? Fewer tariffs on Chinese products? Does it mean more on other countries? Tariffs are coming, whether one likes it or not. The extent, however, and what is priced is another question. Look at this uncertainty chart below. It makes sense; nobody has a clue what’s coming. My personal guess is that it’s going to be less than people think.

This is also seen in some analyst expectations as to what sort of FX moves one can expect. See the table below, where some implied changes are being modelled. It’s assuming a horizontal 30% across all sectors. Looks scary, with an almost 5% drop in EUR/USD, for example. From here? It’s possible, of course, but I doubt that’s coming. In other words, markets, driven by fear and uncertainty, have set the bar damn high for tariff announcements to cause massive moves. Time to fade the USD? Macro still favouring the reserve currency. It’s too early.

Elsewhere, Oil is on the move. I’m not entirely sure what’s driving it, but the calendar spreads (see below) have just exploded. Normally, this would suggest that there are immediate supply issues at hand. Look at the forwards, where Feb 25 futures trade almost at 80 and those for delivery by mid-year 6 USD lower at 74. Geopolitical risks have diminished, so you’d expect the opposite to happen.

Spreads have exploded higher.

This could always be an idiosyncratic risk to some commodity players being stopped out as curve carry unwinds are happening. But it could also be linked to diminishing liquidity conditions. It is important to keep an eye on those developments for a broader risk sentiment context. So far, there is no read-through to other markets.

The models have once again done a fantastic job this week and caught the reversals in bonds ahead of time. Paying subscribers were notified on Wednesday morning. This is a reminder that you can now also use my models in TradingView scripts, which I made available for subscribers to use on their charts. This is not for free and incurs an additional cost. I am also in the process of making one of my intra-day models available. This will come at no additional cost to existing users, but new admissions will see a price increase. If you are interested, ping me an email with your TV username. Note that only paying subscribers will be granted access. No exceptions.

Let’s now read what my friend Macro D has in store for us. We then scan the multitude of charts I have updated below.

Let’s explore!