Friday Chart Book

January 3, 2025

The turn of the year is always a good opportunity to read some papers that were sitting in my inbox for a while. One of them was from the outstanding head of monetary and economic research at the BIS, Claudio Borio. In the paper, he reflects on the successes and limitations of inflation targeting (“IT”) as the de facto global monetary policy framework. IT has proven highly effective in stabilizing inflation, which is essential for long-term prosperity. It incorporates numerical inflation targets, the use of interest rates as the main policy tool, and transparent communication strategies to enhance accountability. Since its inception in countries like New Zealand and the UK, IT has gained widespread adoption, even among nations that do not officially adhere to it. IT’s resilience through major crises like the Great Financial Crisis (GFC) and the COVID-19 pandemic highlights its durability, and no country that adopted IT has abandoned it.

Despite its success in maintaining price stability, IT faces significant challenges. One of the most pressing issues is its inability to address financial imbalances, such as credit booms and asset price bubbles, which can destabilize the economy. This shift from inflation-induced to financial-cycle-induced recessions, with the GFC as a prime example, has highlighted IT’s blind spots. Furthermore, prolonged periods of low interest rates, a hallmark of IT, have eroded central banks’ policy flexibility, creating a “debt trap” where high indebtedness makes it difficult to raise rates without harming the economy.

Post-GFC, central banks have struggled to push inflation back to target levels despite aggressive monetary easing. This reflects the diminishing returns of ultra-low interest rates on stimulating demand and their negative effects on bank profitability, which reduces credit capacity. Additionally, in low-inflation regimes, inflation becomes less responsive to monetary policy because it is driven by idiosyncratic, sector-specific factors rather than broad aggregate demand. These dynamics make inflation harder to influence and highlight the limitations of IT frameworks in addressing structural changes in the global economy, such as deglobalization and geopolitical shifts.

Borio proposes several adjustments to strengthen IT. First, central banks should incorporate financial stability considerations, such as credit growth and property prices, into their frameworks. Second, policymakers must adopt longer-term perspectives to address slower-moving financial cycles and avoid excessive short-termism. Good luck with that.

In addition, greater tolerance for moderate and persistent deviations below inflation targets can preserve policy flexibility and prevent the adverse effects of prolonged low rates. Borio also emphasizes the importance of maintaining safety margins to weather future economic shocks and reducing reliance on forward guidance and oversized central bank balance sheets.

He concludes by urging policymakers to evolve IT frameworks to address these challenges while maintaining a focus on medium—and long-term stability. Monetary policy should ensure price and financial stability without being overburdened as a growth engine, and public expectations must align with its realistic capabilities. He also warns that growing political pressures and unsustainable fiscal policies pose risks to monetary frameworks and central bank independence. By adapting IT to meet these evolving challenges, central banks can ensure that it remains a robust and sustainable foundation for global monetary policy.

Another great article is by the excellent Russell Napier, which I also urge you to read. He dissects monetary history like nobody else. Since the 1990s, the global monetary landscape has undergone profound changes, largely influenced by China's economic policies. Key indicators, such as falling U.S. interest rates, skyrocketing debt levels, declining tangible investment, and soaring asset valuations, point to structural shifts rather than typical business cycle fluctuations. The turning point came in 1994 when China devalued its currency and established a managed exchange rate system, reshaping global trade and capital flows. This "non-system", as he calls it, decoupled interest rates from growth, enabling excessive debt accumulation and financial distortions while encouraging developed-world corporations to prioritize financial engineering over tangible investment.

China's exchange rate management created a flood of cheap exports and foreign investment into its economy, fueling a historic fixed-asset investment boom. Simultaneously, central banks in Asia accumulated vast reserves of U.S. debt, further decoupling interest rates from economic fundamentals and enabling a prolonged era of low borrowing costs. However, the system’s inherent imbalances — high debt levels, undervaluation of China's currency, and suppressed global inflation — are proving unsustainable. As China faces mounting debt, slowing growth, and rising geopolitical tensions, it is increasingly likely to abandon its managed exchange rate system, signalling the collapse of the "non-system" and prompting a reorganization of global monetary architecture.

The imminent collapse of the non-system, Napier argues, highlights the need for a new international monetary framework. Policymakers must address excessive global debt levels, which will likely involve financial repression, higher nominal GDP growth, and a redirection of savings toward fixed-asset investment. Given geopolitical tensions, the world may split into two monetary blocs, with the U.S. continuing to anchor a dollar-based system while China charts its course. Any new system must allow for gradual deleveraging to avoid economic and social disruption, emphasizing tangible investment and reduced reliance on financial engineering. This structural transition marks a pivotal moment in global finance, requiring nations and corporations to adapt to a drastically altered economic order.

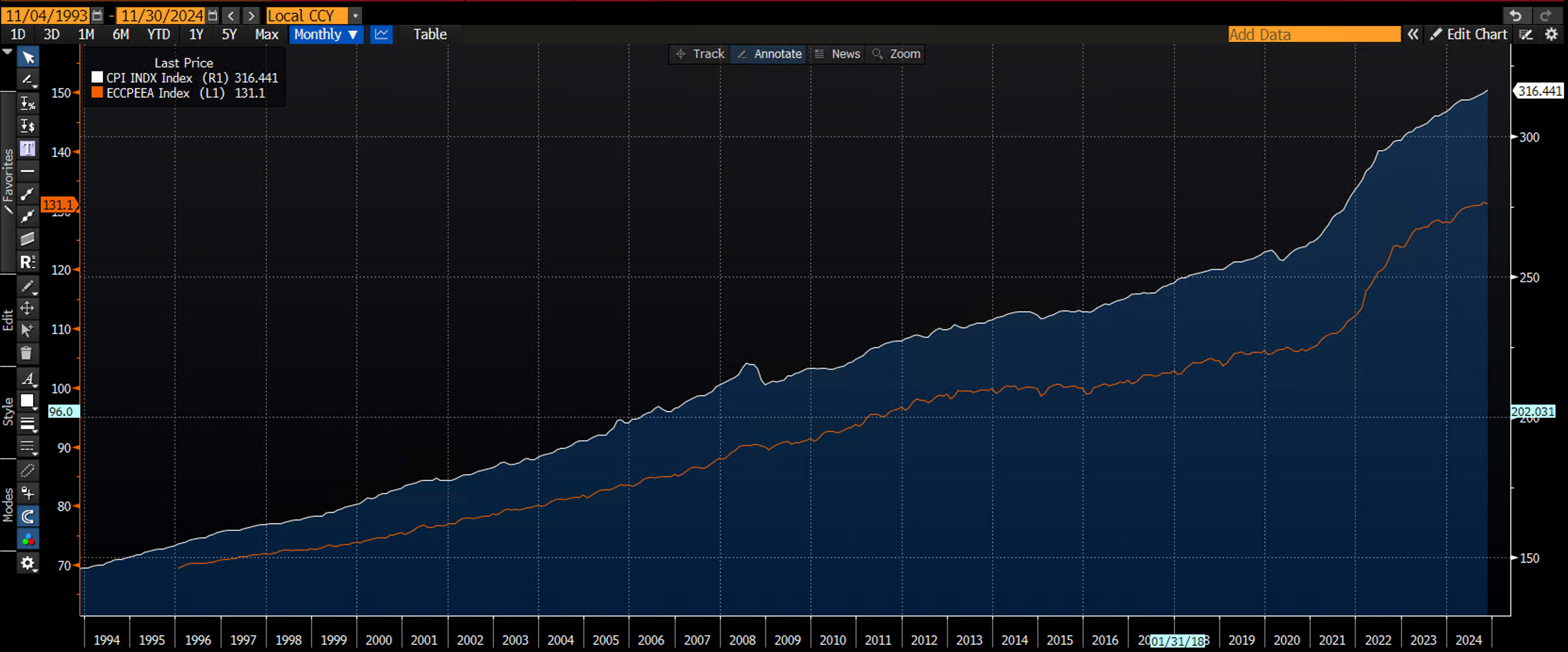

Below is the inflation level trend (white, US) and (orange, Europe). In light of the above two articles, I ask myself whether the unravelling has already started. We can talk about inflation-targeting all we want, and yes, inflation year-over-year readings are coming down, but the price level is still very high. Returning to the pre-Covid trend would require markedly lower inflation and/or deflation, which seems quite far removed from where we find ourselves now. Inflation, as I have always argued, is now a psychological phenomenon. It’s now ingrained in our social construct and, therefore, very hard to tame. Only a recession will reset mindsets, but that’s not a policy goal for obvious reasons.

What has to give? We can focus on policy short-termism, as Borio argues, and pretend it’s all good. Short-termism, however, always comes at a price and I would argue that we built instance imbalances along the way, powered by a myopic monetary policy framework, which has been tested over the past few years. By not inflicting a symmetrical approach to monetary policy, central bankers are igniting increased risk-taking, which in itself poses massive economic risks as market capitalisations stand at an unhealthy multiple of economic output. This can go on for a while, but as history teaches us, it will mean revert. In short, don’t listen to the policymakers; make up your own mind about where policy should be settling. Bond markets are now facing this realisation.

Taking it all in makes me believe that the next crisis, given deficit and debt levels, will not be one of the regular kind. Given inflation expectations and risk-seeking behaviour, it could inflict way more pain, given current levels and economic linkages to the wealth effect I mentioned before. We all dance while the music plays, but when it stops, it won’t be pretty.

Most of you will be familiar with the models and their signals by now. If not, please study the guide I have published. I highly recommend that you go through these notes and guides if you are new to the pack. I am also working on an intra-day model.

Further below, the full book of 250+ charts covers the whole asset spectrum, including equities, bonds, commodities, FX, and Crypto, to give you the most inclusive view. On average, it will generally provide 5-10 set-ups every week. The Trial is still open, so if you are curious, why not try it out?

This is a reminder that you can now also use my models in TradingView scripts, which I made available for subscribers to use on their charts. This is not for free and incurs an additional cost. I am also in the process of making one of my intra-day models available. This will come at no additional cost to existing users, but new admissions will see a price increase. If you are interested, ping me an email with your TV username. Note that only paying subscribers will be granted access. No exceptions.

Let’s now scan the multitude of charts I have updated below. We have already seen quite big moves in the new year, with EUR/USD showing a 2.5 standard deviation move.

Let’s explore!