Friday Chart Book

June 7, 2024

This week opened up a bit more interesting reads across markets than usual. The start of the week was rather volatile, which then gave way to a launchpad for risk to jet off higher. NFPs haven’t been printed as of the time of writing, but anticipations are clearly guiding towards a lower read. Bonds, in particular, are showing a more bullish undertone, which my models caught well with last week’s notice on reversal and are now supported by constructive momentum. The slowdown in data, while premature in extracting a signal, has clearly given the bulls ammunition to push yields lower. This dynamic was a notable shift from last week. No wonder risk assets loved the underpinnings of lower yield readings to rejoice once again.

I wouldn’t, however, count the chickens yet. The ECB cut rates by 25 bps for the first time since late 2019. While this was widely expected, their hawkish inflation forecast will keep them on a cautious rate-cut path. Bunds sold off as the bank’s guidance is extremely open-ended: "The Governing Council is not pre-committing to a particular rate path." The following communication is also worth highlighting. "In particular, its interest rate decisions will be based on its assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation and the strength of monetary policy transmission." This makes it hard to even trade a “cycle” at this stage as there is clearly no indication for subsequent action given the data we are currently presented. Also, a reminder for those running steepeners, as history would teach us the steepener only happens in recessions, not “mid-cycle” adjustments. So, be mindful before burning through the negative carry.

This marks the dilemma for our central bankers, they don’t know where they are and certainly don’t show any indication as to where they are going. For markets, that just means one thing. Carry on as there is nothing new to see here.

Before we explore the full book of charts and set-ups, I leave Macro D the space to explore his thoughts.

by Macro D

These days, I have continued to torment myself; a question has clung tooth and nail to the walls of the room where I catalogue all kinds of doubts.

On 29 May 2024, during a meeting organised by the BOJ, Isabel Schnabel delivered a speech that left me with a lingering question. She chose to focus on the risks of QE, a topic that, to me, seemed like wanting to pour salt on a wound that is still bleeding. Why did she choose this particular topic when she had a broad range of choices available?

I do not have an answer that can be considered more reliable than the others; I only have hypotheses, and you know, hypotheses are a waste of time (especially in this case), and they need more time.

For the moment, I am content to continue thinking about it.

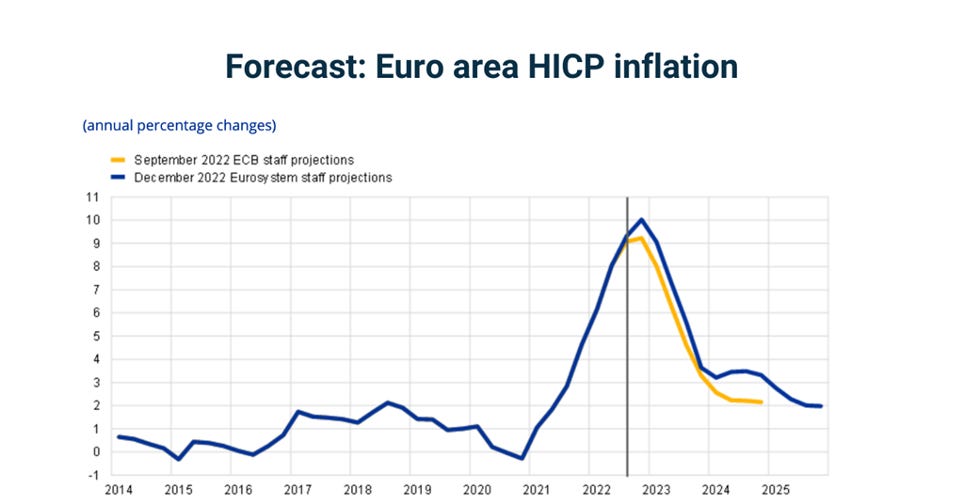

Meanwhile, in Frankfurt, the groundwork has been laid for what I fear is the next currency pandemonium. Lagarde has staked everything on the first-rate cut, but if pushed into a corner, she and her committee can only resort to an excuse, not even a very reliable one, considering the recent past. This graph encapsulates the potential impacts of QE.

According to this graph, the inflation target of 2% will be reached in 2025. I am certainly willing to accept this hypothesis, but I cannot ignore the fact that the same source also proposes another graph that does not seem to agree with the one we have just shown.

Here, the wage indicator that the ECB relies on highlights a future perspective that considers a double inflation rate. Well, yes. It's like mixing salt with sugar.

Stop everyone. Now, we can start from what was already written in capital letters in the stars: the European Central Bank cut interest rates by 25 basis points (0.25%) in today's meeting.

Combined monetary policy decisions and statement:

“The Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner. It will keep policy rates sufficiently restrictive for as long as necessary to achieve this aim. The Governing Council will continue to follow a data-dependent and meeting-by-meeting approach to determining the appropriate level and duration of restriction. In particular, its interest rate decisions will be based on its assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation and the strength of monetary policy transmission. The Governing Council is not pre-committing to a particular rate path[1].”

What does all this mean? What did Lagarde say?

It's clear that Lagarde's approach is shrouded in uncertainty, with this choice failing to secure the commitment of the Board of Directors in a future perspective. The state of things can change at any moment, leaving us on shaky ground.

To me, these seem like the words of someone whose legs are shaking, just at the moment in which he is working to testify to the implementation of an action that:

- Does not allow him to be calm.

- Despite the action implemented, he remains in doubt.

And again, it is said:

“The persistence of strong domestic price pressures can be attributed to the high wage growth, a key driver of inflation. This trend is expected to keep inflation above target until well into next year. The latest Eurosystem staff projections for headline and core inflation have been revised upwards for 2024 and 2025 compared with the March projections. Experts now indicate that headline inflation will average 2.5% in 2024, 2.2% in 2025 and 1.9% in 2026. Inflation excluding energy and food would average 2.8% in 2024, 2.2% in 2025 and 2.0% in 2026. Economic growth is expected to increase to 0.9% in 2024, 1.4% in 2025 and 1.6% in 2026.”

How do I read this other part of the press release?

It's a bit like loosening the security measures of the Van Gogh Museum in Amsterdam just when the Director of the museum received a letter from Lupin[2] that tells him:

By the end of the week, I will steal your collection.

In short, if we seek an answer regarding the characteristics of the path that the ECB will take in the future, we are destined to be left with nothing.

And if we try to answer the question:

Will the ECB further distance its monetary policy from the Fed?

As we ponder this question, we are left to interpret the contrasting emotional responses. In my view, fear may be gripping Frankfurt, while in Washington, the corks of champagne bottles may just be popping.

I remain of the opinion that this cut is a sensational blunder of monetary policy, echoing the never-forgotten mistake made in July 2008 by Jean-Claude Trichet, who raised interest rates shortly before the great financial crisis. Why did he do it? Because he was obsessed with the increase in the price of oil and food. I don't remember a more inconvenient and untimely monetary policy action than that. This comparison should make us all pause and reflect on the potential consequences of such a decision.

In short, it's like setting the alarm inside your house after the thieves have already entered and haven't even left the dog's bowl.

When Trichet intervened, the crisis was already underway; shortly after the ECB's rate hike, the global economy collapsed. What happened? Inflation became a distant memory, and the ECB was forced to backtrack. The ECB's mistake is now not based on a rate hike but on a rate cut, and yet the potential consequences could still be devastating, leaving us all in a precarious financial situation.

And what news is coming from the US?

It seems that the labour market data has taken a downward slope. The Job Openings and Labor Turnover Survey (JOLTS) report has painted its picture: what has come out of it? Thoughtfulness and prudence. There is more. The Bureau of Labor Statistics tells us that at the end of April, the United States could count on 8.1 million vacant jobs, down from 8.4 million in the month of March. This means that the United States has 2 million fewer jobs than last year, a significant decrease. I would not call it an "employment drama", but the weakening is evident. The JOLTS data never goes unnoticed, as the Fed watches them carefully in order to understand the trajectory taken by the labour market. If the downward spiral were a matter solely of the labour market, then we would be content to blindfold ourselves with one hand, but it so happens that even from the HOUSE of GDP, it is not as if greeting cards come.

My attention turned to the GDPplus of the Philadelphia Fed.

And how does the Fed respond to these early warnings? The Fed does the Fed; that is, it sets its internal mechanisms (i.e. the technicians) in motion and corrects its forecasts; after all, this is one of the main activities of central banks: continuously reviewing their estimates so that investors can have as a point of reference yet another number and graph that, indeed, in the next round, will be promptly replaced by yet another forecast. In short, a continuous chase. This time, the Fed responded through its Atlanta section.

But how? Just two weeks ago, a 4.1% growth rate for the economy in the second quarter was mentioned, and then a change of guard between the sun and the moon of fourteen days caused a drop towards 2.7%. Something doesn't add up, and to take stock of the situation, I find myself forced to refer to the thoughts proposed by good Jay every time he painted the macro picture of his monetary policy. Jay has always made it clear that an economy that was too strong prevented the consideration of cutting rates. However, that same economy has suddenly ended up in the clutches of a dietician who doesn't give anyone any discounts. Well, now, I'm not saying that the rate cut is closer; I think that the rate increase is a little further away. If the Fed is data-dependent, I must be, too.

What does the publication of the ADP employment report, relating to creating new jobs in the private sector, say?

The latest job report has revealed a significant downturn in the US economy, with the lowest number of jobs added in four months. This figure, which is notably below the monthly average of last year, is a cause for concern. According to ADP, the United States added only 152,000 private payrolls last month, a significant drop from 188,000 in April and also below the annual average of about 194,000 private jobs added each month.

We can only consider this report as further evidence of the worsening of the US economy.

And yet, there would be another piece of information. The service sector report, which accounts for over 75% of the entire American economy, also confirms the continued collapse of employment, with the sub-index firmly below the 50-point threshold.

And how did the markets read all this?

Following the release of the job data, the markets responded in a predictable manner. Treasury rates, after analyzing the situation, took a dive. On Wall Street and in Europe, investors reacted by buying, leading to a rise in most of the major US equity indices.

It always takes little to rekindle enthusiasm.

Yet, as I said before, I do not think that the Fed cut is any closer; I must stick to the facts. Inflation is still above target, so what could change current affairs? If Friday's non-farm payrolls report continues along the lines of the harmful data we've seen recently, and if the inflation data also starts to look toward the minus one plane rather than the attic, the Fed might begin to think that the pause might be over.

Is there more?

The Bank of Canada has cut its benchmark lending rate by 25 basis points to 4.75%, the first rate cut in four years. Why has there been this change in monetary policy management? Headline inflation is still at 2.7%, but the first quarter GDP of 1.7%, combined with Canadian central bankers' confidence in a continued slowdown, was deemed enough to opt for a change of course.

Even the rise of the Australian dollar did not leave me indifferent; the latest data regarding more substantial inflation than expected forces us to shelve the hypothesis of a rate cut by the RBA. It seems to me that Michele Bullock's concern can be summed up in this sentence she uttered: "Australian household spending is very, very weak". The governor is aware of the higher cost of living and has said she is ready to intervene by raising interest rates again to contain inflation. In short, it's always the same old story: we cannot ignore the actions of central banks. Never.

We now turn our attention to the charts. By now, most of you will be familiar with the models and their signals. If not, please study the guide I have published.

The full book of 250+ charts covers the whole asset spectrum from equities, bonds, commodities, FX and Crypto to give you the most extensive view. On average, it will generally provide a good 5-10 set-ups on a weekly basis.

A reminder that you can now also use my models in TradingView scripts, which I made available for subscribers to use on their charts for a fee. If you are interested, ping me an email with your TV username. Note that only paying subscribers will be granted access. No exceptions.

Let’s go