Friday Chart Book

June 28, 2024

Look at this beautiful chart below of major Western central banks and their policy rates since 2001. Does this shout independence? Absolutely not. We have covered and chewed over the various implications in various write-ups. The recent ECB and BoC rate cuts won’t do hardly stand out as of yet. The SNB, you could argue, is truly independent as it strives to weaken its domestic currency in the process. They have a plan. The others, less so. Everyone is waiting for the Fed to guide. In the meantime, similar service sector inflation stickiness is almost universally observable. I am trying to imagine where this chart will be in a year’s time. I find it inconceivable that relative outcomes will vary over the coming year as it would be quite an economic miracle for all those countries to follow the same growth/inflation and, therefore, policy paths going forward. There are going to be tremendous trades.

But hey, why look at spot rates? Spot rates were former forward rates, so let’s look at whether there is more dispersion on a 1y1y forward horizon (read front rates in a year’s time). There is as the market inevitably wants to price probabilities on forward dispersion and diverging macro trends, but it is still quite narrow compared to the previous few years. With the Fed priced for 2 cuts by year-end and the straddle (call+put) trading at 37 bps, you could say that the scenarios are pretty well distributed. From 3.5 cuts to only a 50% probability of a cut.

Meanwhile, the JPY is continuing on a tear. Look at the chart below that goes back to the 70s. We are, at least technically, in that sharp deceleration zone from the 80s. My view is the same and hasn’t changed. Fundamentally, the JPY fall can not be stopped by unilateral intervention; it would require a larger Plaza-type of accord. Good Luck with that. Yes, they have large pools of foreign reserves, mostly sitting in US treasuries. Sure, they could try to sell them and buy the Yen. But this would just trigger a death loop, shooting US bond yields higher and, with it, the Dollar. Their tactic is to slow the depreciation, but they can’t stop it.

“Inflation is a form of taxation that can be imposed without legislation.”

Milton Friedman

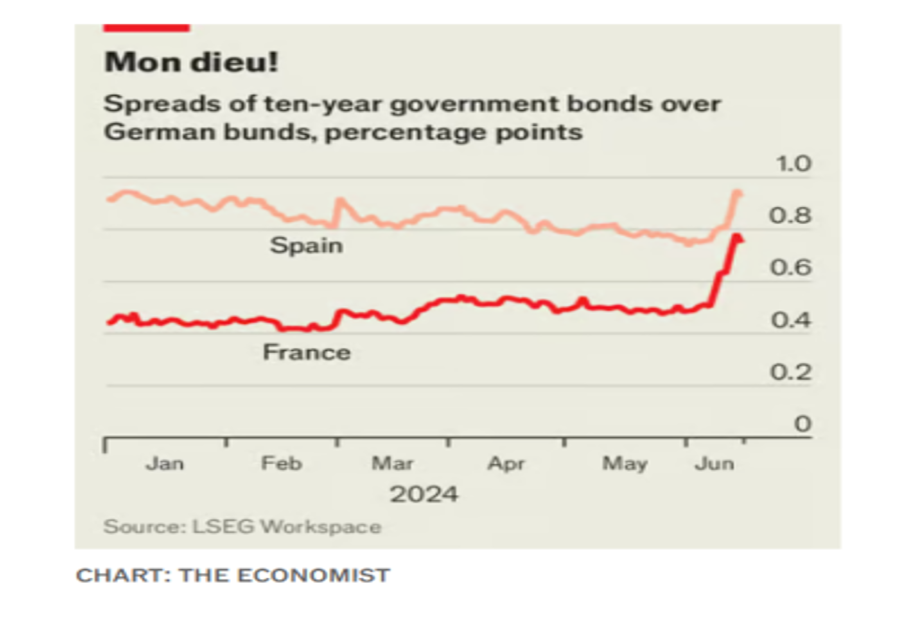

It was announced as the week of US inflation, and so it was. Everyone was waiting for the data, myself included. Focusing on just one topic brings me back to the saying "put all your eggs in one basket", and to tell the truth, I still haven't understood whether this saying refers to a virtue or a weakness. On Monday, I started looking around, and to look, there was something. For example, the European Commission announced its intention to propose to the EU Council the start of an excessive deficit procedure for seven member countries: Italy and France, Belgium, Hungary, Poland, Slovakia, and Malta. And then there is always the Economist[1], which does not miss the opportunity and begins in this way:

What did we leave behind? Given a US economy that exceeds expectations, I would first respond with "A Fed ready to cut rates”.

The latest S&P Global surveys declare that the American economy performed well in June, with inflation that subdued: 1) The composite PMI rose to 54.6 in June, marking the highest level since April 2022. 2) The services PMI went from 54.8 in May to 55.1, the most accentuated expansion of the services sector in the last two years. 3) The manufacturing PMI went from 51.3 to 51.7.

So, the recovery seems reliable, and sales price inflation after the increase in May fell to one of the lowest levels recorded in the last four years.

And now, let's go knock on the beating heart of the week. Monday, June 24: Before the inflation data, the general context was a jungle of conflicting messages. The interest rate cuts seemed to have been postponed following significant economic activity and a healthy labour market. The consumer and producer inflation rates were good, and all this advised not to consider immediate increases in US bond yields and the US dollar.

The Fed is carefully monitoring the core PCE index to gauge the path of the Fed funds rates, which are still stuck between 5.25% and 5.5%. It must be considered that the core PCE—relating to May represents the swan song (the last significant macro data in the United States for the second quarter of 2024).

This data purges the headline PCE index of the most volatile variables: food and energy prices.

The consensus estimates were for monthly growth of +0.1 % in May, which is the lowest since November 2023. The crux of the matter was this: if the expectations had been confirmed, then the markets would have been legitimized to still believe in a rate cut.

It was a Monday afternoon, and I, a victim of a long-standing monetary obsession, went back to knock on the door of the good Jay, and I remembered pretty recent times. In the last FOMC meeting, Powell emphasized the need to see further evidence of disinflation before committing to a rate cut: "In fact, a revision of the 'dot plot' was also carried out, with the 'median dot' indicating only one cut for this year (previously there were three), but with a further cut next year, bringing the total to four cuts for 2025". I was there to reel off my classic questions in the open air since the data on US inflation was still far from being revealed.

"Does it follow that I shouldn't focus too assiduously on the 2024 halfway point, given that Treasuries are pricing in the view that has two cuts for this year?

I passed the time by peeking at my smartphone: the rates of US government bonds with a maturity of 10 years oscillated around the threshold of 4.270%, while the rates of two-year Treasuries were hovering around 4.745%. The increase in consumer prices has fallen from 9.1% in June 2022 to a range between 3% and 4% in recent months but is still above the Fed's target of 2%, which calls into question the stability of the response to the fundamental question.

“Will Jay cut rates this year, or will he sit back and wait?”

As the inflation target approaches, it is necessary to hope that there will be no nasty surprises, i.e. data above expectations, as happened in the first quarter of 2024; at the same time, a powerful slowdown in the labour market could lead the FOMC to take their cutting intentions more seriously. Meanwhile, between screens, I grappled with Chicago Federal Reserve Bank President Austan Goolsbee, who was still looking for a further cooling of inflation as part of the process that would open the door to a rate cut. In an interview with CNBC, Goolsbee said he hoped he and his colleagues would soon have more confidence in inflation. He called the monetary policy implemented by the Fed so far "very restrictive". I arrived on Wednesday without any surprises to keep me company (apart from the data on Australian inflation that seems to be a precursor to an upcoming rate hike). Here, I saw that the yields of US Treasuries were rising following the resumption of inflation in other countries and fears of an intervention by the Japanese authorities to stimulate the Yen. At that time, in Japan, the Yen had fallen to its lowest level since 1986 against the dollar, and this immediately made me think that soon, some voices would rise from the Land of the Rising Sun. No sooner said than done, the time to sense a certain pressure on Treasuries, that Japanese Finance Minister Suzuki said he was ready to act on the decline of the yen, as he was "deeply concerned" about the effect of the decline of the yen on the economy. At that time, the yen was down about 2% in June and 12% for the year against the dollar.

Cabinet Secretary Yoshimasa Hayashi also revealed the authorities’ readiness to “respond appropriately” in the event of excessive currency volatility that would hurt household and business demand.

Regardless of the direction of the exchange rate, I also began to worry about the source of the money that Japan would spend to patch up the battered yen further. This time, would it find the money by selling US Treasuries? Would it print money?

Meanwhile, there was also news from the banking sector. The central US banks have enough capital to cope with hypothetical economic and market turbulence and various black swans that could appear along the way. This is the verdict of the Federal Reserve’s “stress test”. It found that 31 central banks could withstand unemployment, significant market volatility, and even a collapse in the residential and commercial mortgage markets while maintaining enough capital to continue lending and doing their jobs. Charles Schwab Corp had the highest capital levels under the test, with a 25.2% capital ratio under a severe scenario. Bank of New York Mellon Corp, JPMorgan Chase, Morgan Stanley, Northern Trust, and State Street reported double-digit capital ratios after the test.

And here we are, closing in on the weekend.

The PCE index of the leading US consumer prices, one of the most relevant indicators for the Fed's Fed's monetary policy decisions, increased by 3.7% in the first quarter of 2024. Core inflation, which excludes energy and food prices from the calculation, exceeded analysts' estimates, which expected an increase of 3.6% in the first three months of the year after 3.7% in the first reading. In the last quarter of 2023, the PCE core had marked +2%.

The final estimate also revises the United States's GDP upwards, which grew by 1.4% in the first quarter of the year.

And in response to these data, how did the market close?

We saw a relatively weak closing. In Frankfurt, the Dax closed positively, while London, Paris, and Milan ended with a minus sign. Why? European operators focused on the first round of the French elections, scheduled for Sunday.

But let's go back to the American macro data. I asked myself:

"Do they help the Fed or not?"

I answered that these data theoretically increase the possibility of a rate cut, but certainly not immediately. The final GDP data goes in this direction, showing that the American economy has slowed down. The GDP data also tells us something else about consumption, which has slowed to 1.5% from 3.3%, as shown in the fourth quarter of 2023. Furthermore, unemployment benefits also give Jay a helping hand as this week they reached the highest since the end of 2021.

Then, it was the turn of the boxing match: Biden vs. Trump. Who won?

According to the CNN poll, 67% of Americans believe Trump won. Why? There was a tired, confused, and unintelligent Biden in front of everyone's eyes, who offered a questionable performance. Trump, as usual, hit hard from every direction and added fuel to the fire, making fun of Biden's difficulty in expressing complete sentences. The futures of the American indices reacted with a rise to the debate's outcome. The futures of the S&P 500 index rose by 0.3% while the US dollar also gained ground in the Asian session.

In the morning, the UK GDP was revised upwards, and I interpreted the data as a signal, allowing the BoE to gain more precious time before moving. At this point, the rate cut could be definitively postponed until after the summer. At this point, I had no choice but to count the minutes until the long-awaited moment. When the PCE core index finally arrived, I thought... Much ado about nothing.. Why?

The monthly trend shows zero variation, as expected (but I love to imagine surprises of all sorts). On an annual basis, there was a rise of 2.6%.

In short, this time, Mrs. Inflation wants to pack her bags and say goodbye to everyone. Who believes it? I don't, but the markets think differently.

Futures on the leading US stock indices accelerated upwards, while the rates on 10-year US Treasuries fell to 4.265%. Now Jay has the much-desired information he was waiting for. What will he do?

Before the long-awaited US macro data, IMF director Kristalina Georgieva's speech made me smile, asking the Fed to wait until the end of 2024 before cutting rates. The director's reasoning, on the other hand, is understandable. "US GDP is strong, and inflation is still far from the 2% target: why rush and cut rates?" Perhaps the director was predicting something.

[1] The Economist is an English-language weekly political and economic news magazine that focuses on global current affairs, international trade, politics, and technology.

We now turn our attention to the charts. By now, most of you will be familiar with the models and their signals. If not, please study the guide I have published.

The full book of 250+ charts covers the whole asset spectrum from equities, bonds, commodities, FX, and Crypto to give you the most extensive view. On average, it will generally provide a good 5-10 set-ups on a weekly basis.

A reminder that you can now also use my models in TradingView scripts, which I made available for subscribers to use on their charts for a fee. If you are interested, ping me an email with your TV username. Note that only paying subscribers will be granted access. No exceptions.

Let’s go