Bond Market Thoughts

Keeping Perspective

Let’s look at the recent bond movements and keep a perspective on what is noise and what is maybe signal.

You know my view on the recent Fitch downgrade. It’s meaningless. Rating agencies are one of the most useless organisations on the planet. They are like a doctor that will pronounce you dead when they lower your casket down into your resting place. They never had any proactive role in anticipating a credit event, at least not to my knowledge.

The Fitch rating agency, which is by far the least important amongst the “big three”, downgraded US sovereign credit from AAA to AA+ yesterday afternoon. Index-sensitive investors who are only allowed to buy sovereign bonds of a certain quality will not be impacted. The much-used Barclays indexes use the middle rating of Moody’s, Fitch, and S&P for sovereign and agency debt ratings. Therefore, US Treasuries and GSE debt ratings will be lowered from AAA to AA+ as a result of the downgrade. This will not force any selling at all as reserve managers’ guidelines point to the “highest of” rating or exclude US Treasuries altogether. Yawn.

With that out of the way, let’s scan what’s going on in rates.

Any sovereign creditworthiness would appear in swap spreads. Invoice spreads are similar in that they compare the yield on a Futures CTD with a forward starting swap of equivalent risk. If creditworthiness were in doubt, invoice spreads would go deeply negative. In this case, they just moved lower by a basis point, hardly noted on the charts below, which include 2,5,10 and 30-year maturities.

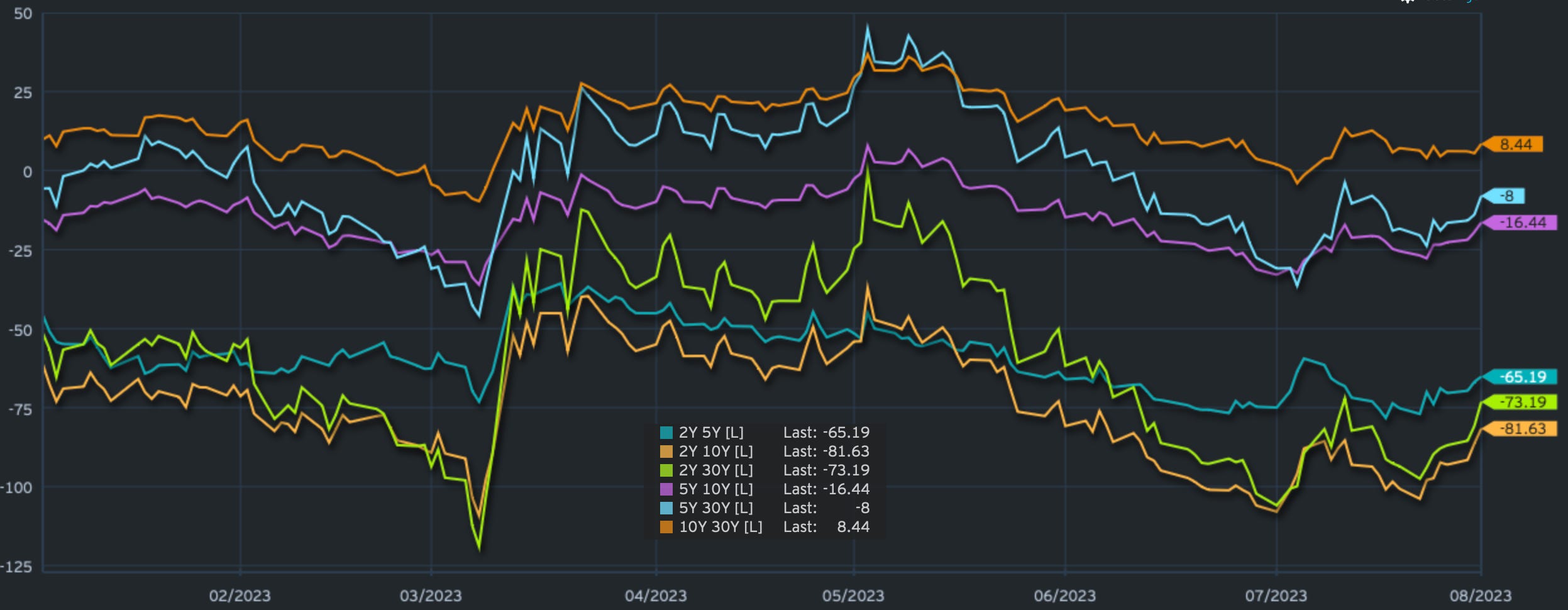

Curves have been bear-steepening over the past week, reversing some of the previous flattening trend.

Looking at the weekly spot / forward change heatmap reveals our intuition that the 10+ part of the segment has been hit hardest, both in the spot and forward curve, while the front end has hardly moved.

Why the steepening? I think there are two thoughts worth exploring on this. One is the impact that BoJ’s more flexible YCC approach had on global yields. I discussed this on Monday in ATW.

This “overcommunication” strategy has now taken another small knock in my view when thinking about what the BoJ has just done last Friday. Although they kept the YCC band at +/- 50 bps, it no longer views this band as a rigid limit and will not look to rein the rate in via unlimited bond purchasing operations even if it rises above 50 bps. Rather, it will use such operations only if the long-term rate threatens to exceed 100bps. To this degree, the central bank has increased its ability to exercise discretion which is refreshing to see.

It reminds me of the time when Mark Carney (former Bank of Canada and Bank of England governor) was regarded as being an “unreliable boyfriend”. While somewhat of an uninspiring label, it is precisely how central banking should work.

The other thought is simply a hit to the good old hunt for carry trade. Remember the following saying when it comes to investing in fixed income. “Eat like a mouse, poop like an elephant”. A little reminder that yield curve flattening positions are and have been a very profitable trade this year, especially as long as the Fed was perceived to be in play.

A 2-30s flattening position (selling 2s vs 30s dv01 neutral) would result in a massively long carry/roll proposition. In fact, the curve would have to steepen by 103 bps over a year in order for you to start losing money on the trade.

Whack, that’s a 30 bps move in your face over the past week. Remember, those trades involve a large degree of leverage.

With this move, option vol should be exploding, right? The below chart shows the 3-month expiry on 30-year tenors ATM (top line dark blue) and then the implied annual bps volatility of the skew from -100 bps to +100 bps. While moving higher, there is hardly an unorderly vol spike.

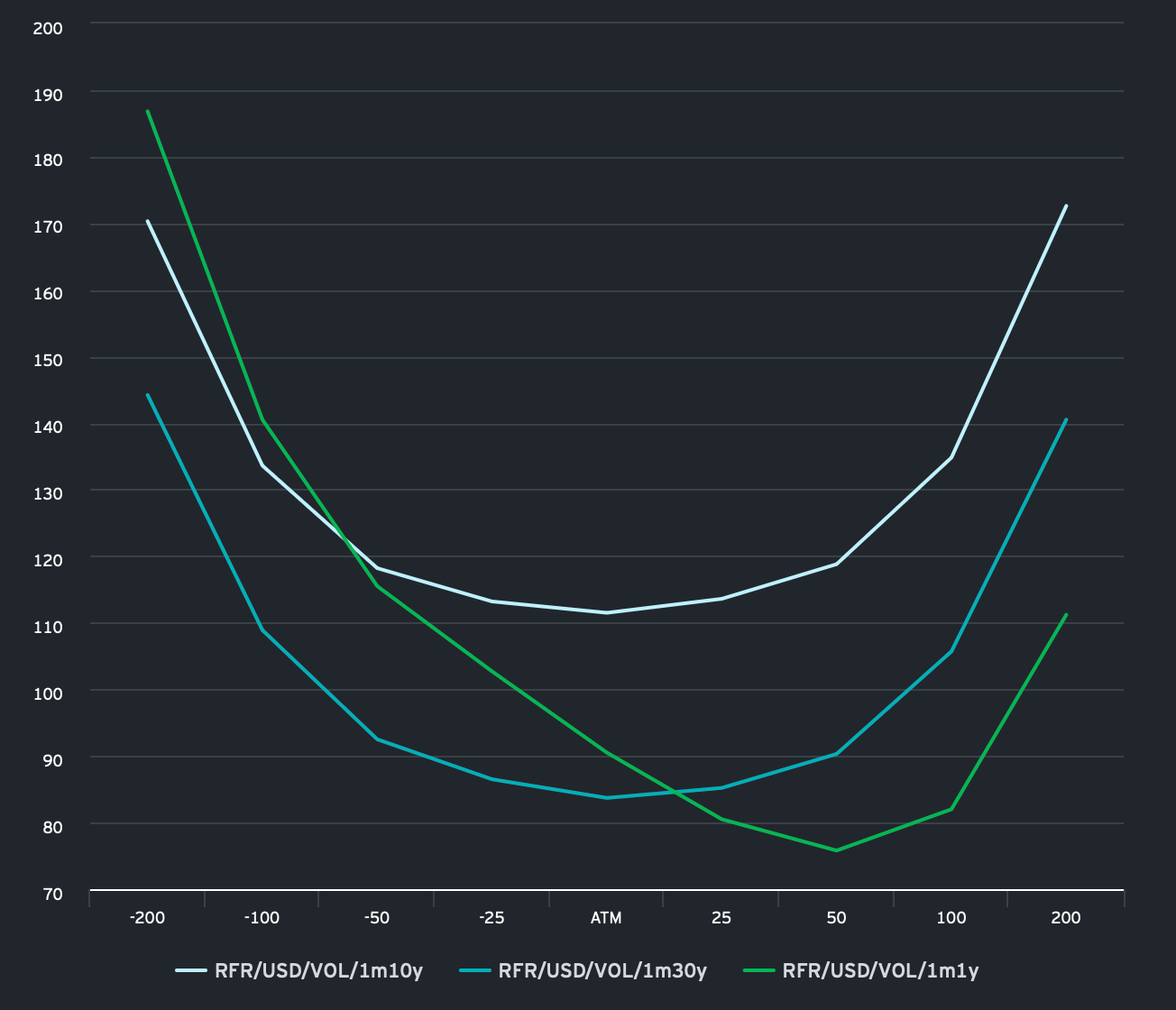

Looking at the skew, both 1-month expiry options on 10-year and 30-year SOFR swap maturities exhibit a very symmetrical volatility smile. Meanwhile, I’ve also plotted the 1-month expiry of 1-year swaps, which clearly have a massive skew towards lower prints, indicative of good hedging and speculative positioning for lower front-end rates.

Technicals, meanwhile, still look ugly. Those on the alerts know that the countdown for a bounce has begun. The model has been shorting this on the longer time frames and playing the bounces very well. I will update you when and if anything gets triggered.

ZN is exhibiting similar downside fatigue and flashing oversold conditions.

I hope you found this useful. If you want to be updated on any thoughts and model alerts, join the pack and hit the button below.

Good luck out there!

Can you recommend any further reading on bond files? I have always been interested in them!

Good piece as always. Where do you get the curve carry and roll down screen from?