Bond Futures

A (hopefully) simple Guide

I am sure you have come across bond futures before and even traded them privately or professionally. There is nothing super complicated about them, but I thought it would be useful to have a short guide here for those who might not be as familiar.

Basics

Government bond futures contracts are a very liquid and key risk tool both for hedging and speculative purposes. They are exchange-traded standardised contracts that set a price for a specific amount and quality of bonds to be delivered during the futures contract's expiry month. Unlike short-term interest rate futures (STIR), which I will cover in a separate post, bond futures demand the actual delivery of the bond upon settlement. STIR futures, meanwhile, are cash settled.

Most futures contracts, including those traded on ICE, EUREX & CME, have three-month maturity intervals with termination dates in March, June, September, and December. As the maturity date nears, the trading of contracts becomes less liquid.

After establishing a position in a futures contract, a party can either let the position mature or terminate it between the trade date and maturity. If a position is closed, either a profit or loss must be booked. If a position is held until maturity, the party who has the futures contract will receive the underlying asset (the bond) at the settlement price, while the party who is short on futures delivers the asset.

The beauty of futures is that there is no associated counterparty risk. The clearing house settles the contracts and acts as the buyer for all contracts sold and the seller for all contracts bought.

There is plenty of excellent intros and more intricate detail you can find here and regarding contract specifications here.

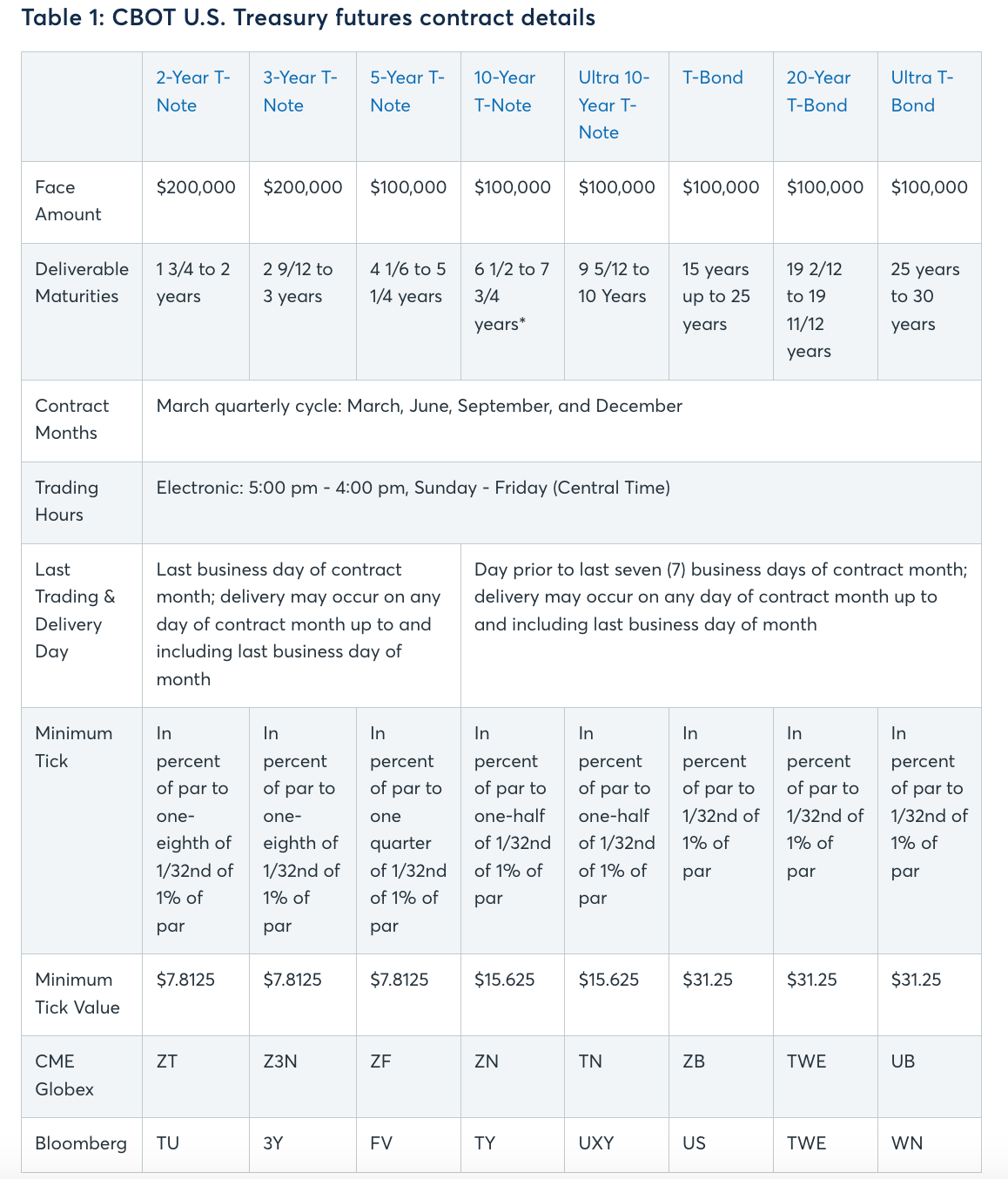

This table gives you the details regarding US bond futures specifications. Note that only the 2 and 3-year notes have a notional of $200k.

Futures Pricing

Now, this is slightly trickier, so I am trying to simplify as much as possible. As with many things in finance, one has to price most derivatives arbitrage-free. This means that no risk-free money can be generated by the simultaneous buying and/or selling of securities. This is no different for bond futures contracts.

Example

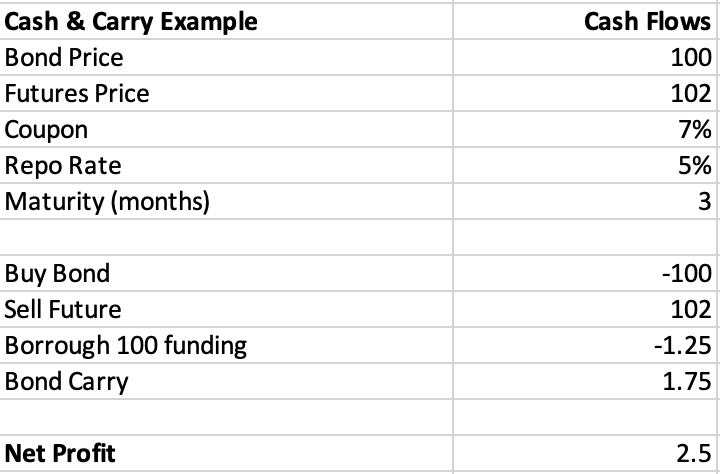

Let’s say that we have a 10-year bond with a coupon of 7% that is trading at par (100). This bond is the underlying asset represented by the long bond futures contract; the contract expires in precisely 3 months. If we also say that the three-month repo rate (borrowing rate) is 5%, what is the fair value for the futures contract?

This is assuming no funding, so we have to assume borrowing. For our example, we are assuming a futures price of 102.

In a Cash & Carry transaction, we borrow funds to buy the bond at 100 and then sell the future at 102, which settles in three months’ time.

The cash flows associated with this combination are as follows:

As you hold the bond, you are entitled to your carry of 1.75 (7% / 4), but you have to pay back the borrowed funds of (5% / 4). As you are in a profit in this example, this cash & carry would make money which in the real world would be immediately “arbd” away.

Now, let’s imagine the price of the future would be 94 instead of 102, with all else being the same. We would conduct a reverse Cash & Carry transaction, whereby we are selling the bond short, earning repo on the cash received while simultaneously buying the future until maturity. The cash flows would look like this.

Again, the future is mispriced as the transaction nets you a gain of 5.5.

In order to get to arbitrage-free pricing of futures, we can now solve the above cash flows as follows:

Definitions

R = the repo rate

C = the bond’s running yield

B = Price of bond

F = Price of futures

T = Time to expiry

So for the cash & carry example above, we get the following:

Total Proceeds: F + (B * C * T)

Total Costs: B + (B * R * T)

Profits = F + (B * C * T) - (B + (B * R * T))

Now, we know that profits have to be zero in our arb-free world.

So it’s:

0 = F + (B * C * T) - (B + (B * R * T))

Rearranging for F gives us the following:

F = B + (B * R * T) - (B * C * T)

F = B * (1 + T * (R - C)

R - C = Cost of Carry

This should hopefully make sense. If we have positive carry (when C > R), then the futures price will trade below the cash market price, that is, so the future will gain in price terms to offset the positive carry it is not receiving. Where R > C and we have negative carry, then the futures price will be at a premium over the cash market price. Obviously, if the net funding cost was zero, such that we had neither positive nor negative carry, then the futures price would be equal to the underlying bond price.

I will leave it here as there are quite a few angles to digest. Remember that this example above is from an unfunded perspective and hence involves leverage (borrowing) in order to derive the arbitrage-free price.

What if you are fully funded, though? In this case, you have either the option to buy the bond and earn the carry (yield) over your investment horizon or, alternatively, buy the corresponding future, which carries no yield. As the future is only margined, you can then earn the repo rate yield of the cash not invested over your investment horizon. This should, apart from deviations of CTD optionality, return you the same total return as the bond over your investment horizon.

Bond futures are not magic, but they offer leverage to the investor, so it is prudent to understand the basics. The CME has a great tool where you can look at various futures and see their modified durations and BPV (basis point value or DV01), which gives you an indication as to the price sensitivities for every basis point in yield. Another important concept which I will cover in a future post.

I hope you found this guide helpful. Please leave a comment if you want me to cover other topics or go into more detail.

Great explanation thanks