Attack the Week (ATW)

February 26, 2024

Monday Thoughts

I am currently advising a friend looking to in-house his trading strategy within a larger institution. It’s a great systematic investment program, which he has been running for a few years with his own capital and is now looking to scale up. He has had a few offers and almost gave away parts of his intellectual property rights. Luckily, he didn’t. When we first sat down and looked through various options and contacts, I homed in on one simple thing to remember. “Don’t play it small”.

It’s easy to be enticed when the first offers come in. Yes, you would still be better off than continue running it only with your own money, but the opportunity costs of not going big can be massive. What he should be focussing on is getting the support of an institution that can help scale up quickly, powered by a vast distribution network to support such an endeavour.

I have experienced it personally and seen it often in others how playing things small is often viewed as the safest strategy. It's surely the path of minimal resistance, a way to protect oneself from the potential pitfalls of failure. However, while seemingly prudent, this approach harbours its own set of dangers, both to personal growth and business evolution.

Playing it too small in markets has obviously similar implications. Sure, you might not lose much, but how will you ever outperform if you are not playing it big when you have the highest conviction?

Today’s market feels like the majority of investors are playing it small. Many of the smartest discretionary investors I follow or talk to do indeed not have much risk on. If everyone plays it small, aren’t there bigger opportunities around the corner? Vol-targeted funds, meanwhile, are scaling up as cross-asset vols recede, exhibiting their natural pro-cyclical risk setup. Patience, as always, is warranted as the bigger pitches will come; we just have to observe synthesised signals and keep the mental capacity for when the time to engage more forcefully comes.

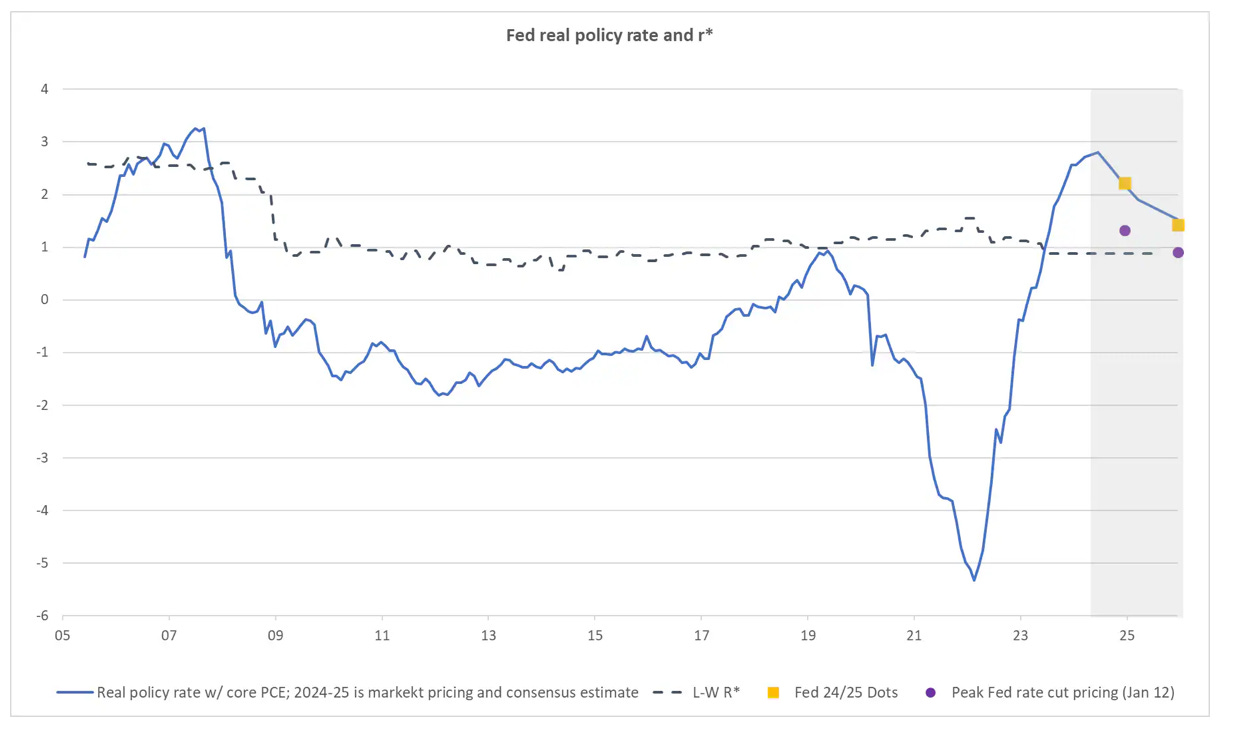

The re-pricing of US rate cut expectations was a relatively larger set-up over the past few weeks. We caught this one as the momentum model guided us towards higher yields. Now, we have arrived at the pricing in the Fed’s 2024 and 2025 dots to perfection (yellow markers in the chart below).

The question is whether the recent crossing of US 10-year real yields above 2% will again prove to be a headwind for risk-asset performance. This comes at the same time when US nominal treasury yields (10y) exceed the SPX’s earnings yield for the first time in two decades.

I thought Governor Waller’s latest speech was worth a read. The following passage was noteworthy:

“That makes the decision to be patient on beginning to ease policy simpler than it might be. I am going to need to see at least another couple more months of inflation data before I can judge whether January was a speed bump or a pothole. I will be watching wages and compensation, and the components of inflation that I outlined today to see whether broad progress on inflation continues or stalls. I will also be monitoring economic activity and employment, attentive as always to any unexpected warning signs of a recession, but also paying close attention to whether growth in each is consistent with continued progress toward 2 percent inflation.”

We are all watching the same data here, but we know from his speech and last week’s minutes that there is no hurry on their end. They are playing it small for now. Understandably so.

Let’s now turn our attention to what else we should be focussing on during the week. Similarly, we will nail down the most important charts.