Attack the Week (ATW)

September 11, 2023

Monday Thoughts

I am writing this from Italy’s beautiful Umbria region. I decided last minute to take my wife to Venice and then relax for a few days in some beautiful surroundings in the heart of Italy.

As I was enjoying the drive through the Tuscan hills, I pondered a question a family friend asked me in terms of what the equity vs. bond split should be in portfolios these days. It's not an easy question to answer, especially after the disastrous performance of both asset classes in 2022. Also, it obviously depends on everyone’s personal circumstances and time horizons.

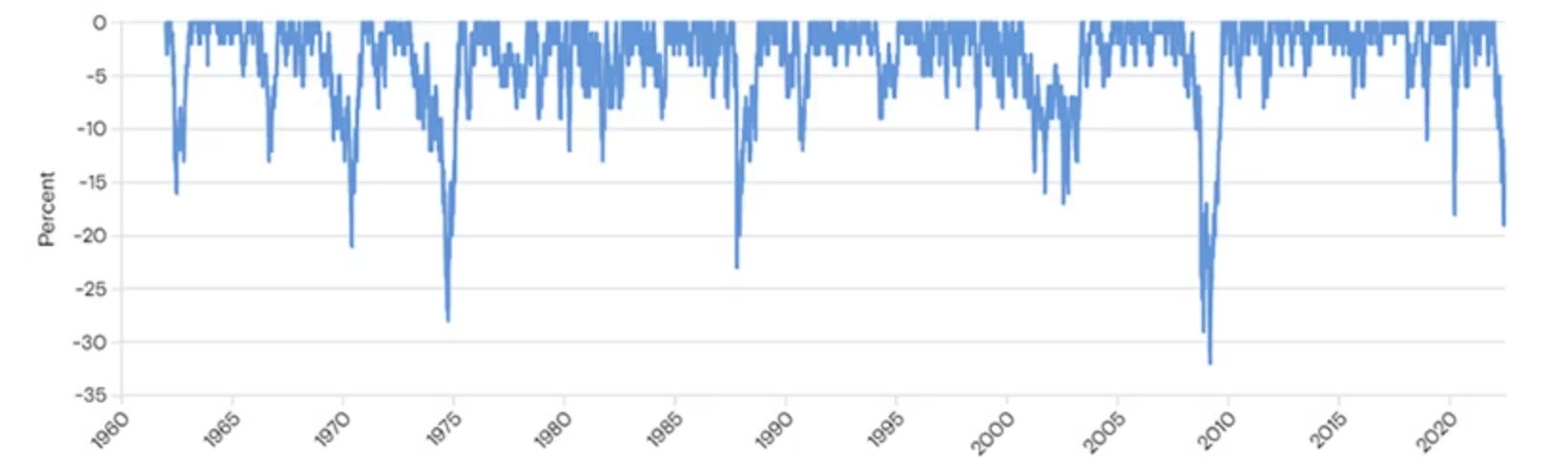

60/40 Portfolio, 12-month peak-to-trough drawdown (until 2022)

The much-lauded 60/40 split worked extremely well and posted the highest Sharpe ratio over the past decade until recently. As you can see from the graphic below, those eye-watering Sharpe ratios weren’t as rosy during more inflationary times, such as the one we are currently in.

10-year rolling Sharpe Ratios (monthly returns)

The aggressive monetary tightening trend over the past 18 months has shaken global bond markets and, hence, any portfolio that relied on the asset class for diversification and risk mitigation benefits.

The need for inflation protection would currently suggest a higher allocation to real assets would be warranted. Real estate, precious metals and collectables have proven more resilient during more inflationary times, certainly relative to traditional markets.

10-year rolling returns, annualised

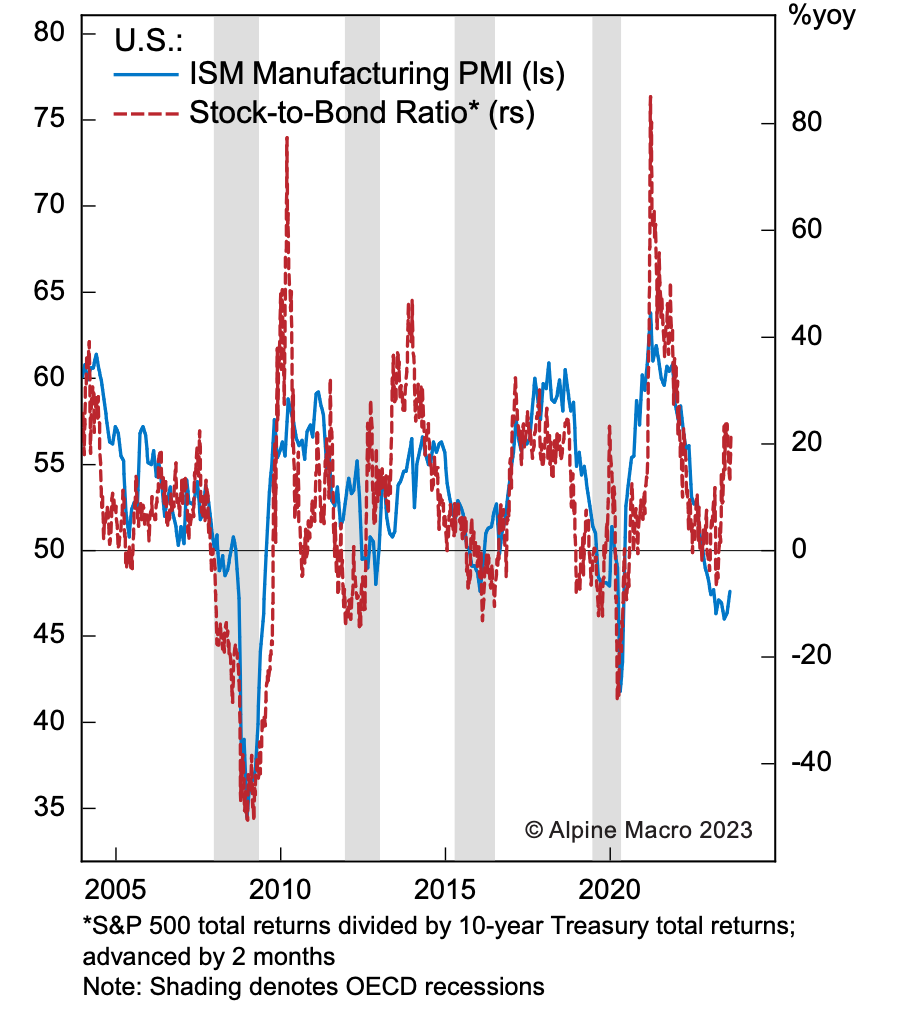

The Equity / Bond Ratio (US in the below chart), however, has hit new all-time highs. The ratio typically turns south as we enter a recession. The exception was in the 80s when Volcker’s tightening hurt bond markets first while stocks continued grinding higher amidst high nominal growth. Sounds familiar, right? Although equity valuations were much cheaper back then than now.

The ratio has some predictive characteristics, with the current juncture pointing to a strong rebound in manufacturing conditions in the US. Or is the ratio about to turn lower?

So, the answer isn’t easy. If you expect a recession in the coming 3-6 months, it’s prudent to reduce your equity weight in favour of bonds. If you are, however, still in the high nominal growth camp while we continue waiting for a recession to materialise, a higher equity weight still seems warranted, given higher running nominal growth. A continued build to real assets is also still warranted. It’s finely balanced, and I would as always urge you to do your own homework on it and continue staying nimble.

The answer, as usual, lies somewhere in the middle. I’d think neither 100% allocation to bonds nor equities is prudent; a mix is possibly the best option to make sure you gain some diversification benefits. As for me, 1/3 to bond, equities and real assets is possibly the best mix still. Within that, of course, there is more detail to be discussed, which I will happily do in a separate post.

Now, let’s attack the coming week with more data points and likely set-ups in play.