Attack the Week (ATW)

Fed Chair Transition History / Weekly Calendar / Asset Allocation Model Update

Sunday Thoughts

I have now returned from the hills and valleys, my body aching, but my head and mind are cleared and fully recharged. There is something special about connecting with nature, sitting atop a hill, and just watching the clouds go by.

The upcoming week will be very interesting as it will reveal the momentum behind the entrenched global yield sell-off, which culminated with a sizeable global move on Friday. Both my asset allocation model (see the latest allocation below) and our momentum model (dashboard on pa-globalmacro.com) have been flagging underperformance in global bonds for a while. Key levels are being tested in US 10-year yields as I laid out in my last post.

Late Friday Thoughts

I have spent the past few days hiking through the hills and valleys in the rainy British North with little reception. I planned this by design as I cherished some detox from screens and constant market news. I only checked markets yesterday evening after returning to a hotel with access to the worldwide information superhighway. Before I left, I sold down some of my equity risk exposure and moved to cash, as I didn’t see scope to further chase the rally from here. Much of my thinking was driven by the piece I wrote before this week’s CPI, which outlined how increased inflation volatility will drive markets and risk premia from here onwards. It’s the biggest macro driver from here. See details below.

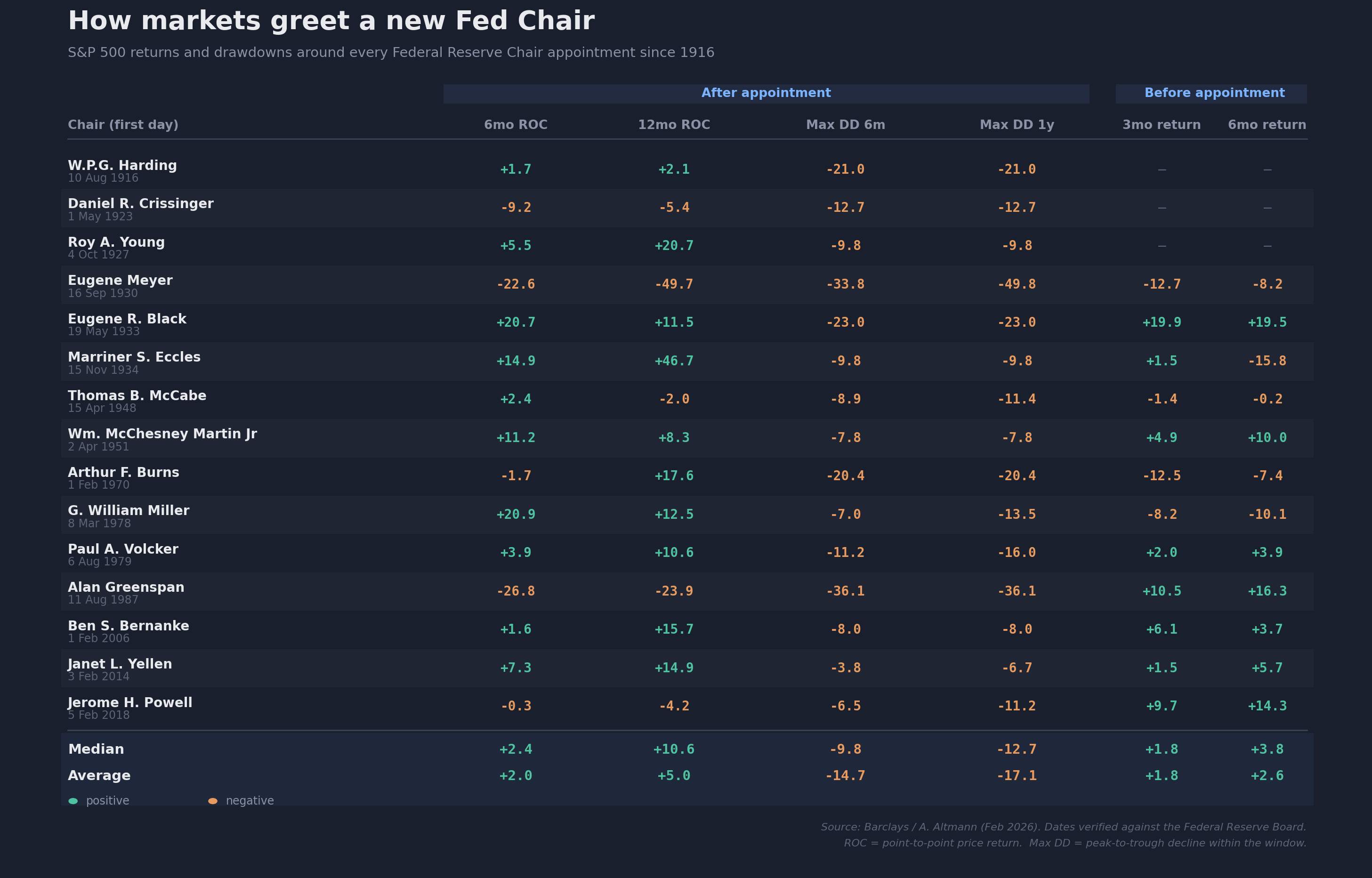

Furthermore, risk assets have begun to react to higher yields, and the increased volatility they create across asset markets is evident. One day doesn’t change the overall trend, but it is important to see it in the context of a Fed chair transition.

Powell’s term as chair expired last Friday, May 15, and Kevin Warsh was confirmed by the Senate two days earlier in a 54-45 vote — the most partisan ever for a Fed chair, with only Fetterman crossing from the Democrats. He hasn’t yet been sworn in, but his first FOMC is already on the calendar for June 16-17. So we’re sitting in the handover window: a market that knows who’s coming, hasn’t seen what he’ll do, and has roughly four weeks to price it before he opens his mouth in an official capacity. The table is designed exactly for this moment.

The historical pattern is harsher than the median suggests. Looking across all fifteen chairs back to Harding in 1916, the median six-month return after a new chair takes office is a perfectly respectable +2.4%, and the median first-year return is +10.6% — numbers you’d happily take if offered.

But the drawdown columns tell a different story: the median peak-to-trough decline inside year one is roughly 13%, and the average is closer to 17%, dragged there by chairs who walked in just before the wheels came off — Eugene Meyer into the Depression, Greenspan eleven weeks before Black Monday, Burns into the early-70s bear, Powell into the Q1 2018 correction. The other regularity worth flagging is that markets aren’t usually flat going into a new appointment; they tend to have just rallied (Powell himself had a +14.3% six-month run-up before taking the chair) and then test the new chair on the way in.

Warsh inherits the trickiest version of that setup. S&P at all-time highs into the handover, CPI at a three-year high after the energy shock from the US-Israel-Iran conflict, four FOMC dissents in April (the most divided since 1992), and a president openly demanding cuts, the data may not support. Warsh’s stated preferences — faster balance-sheet runoff, tighter inflation discipline, a more narrowly focused Fed — point hawkish relative to where Trump wants policy to land, which makes the June 16-17 meeting a genuine event-risk catalyst rather than a procedural one.

The historical base rate says the test usually comes within six months; what it can’t tell you is whether Warsh’s reputation as a balance-sheet hawk dampens the drawdown (by reassuring on inflation credibility) or amplifies it (by tightening financial conditions into an already-stretched market). Either way, the table is a reasonable prior for sizing the next six months of equity risk — not a forecast, but a base rate worth carrying in the back of the head.

Let’s now read Macro D’s latest thoughts as we view his latest Macro FX trades, before we scan next week’s macro calendar, analyse the latest Macro Dashboard insights and then find out what the asset allocation model’s latest output is.

Have a successful week ahead!