Attack the Week (ATW)

Market Whispers / Weekly Calendar / Macro FX Spreadsheet / Dashboard / Asset Allocation

Sunday Thoughts

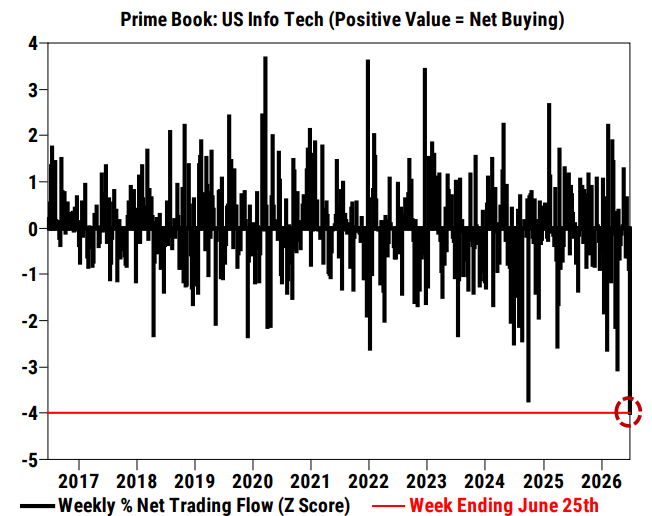

I hope you all had a fantastic weekend. As I am back in the saddle and more glued to my screens, I couldn’t help notice how equities have started to trade oddly. There are huge intra-day swings, on no news, and this is not only visible in US stocks but also in some Emerging Market indices. According to GS, they have seen the largest net selling of global equities in three months. Interestingly, the US info tech sector has seen the largest net selling in over a decade.

In many ways, the markets are always trying to tell us something. Often, of course, it is just noise. This time, however, I think there is more subtle messaging being broadcast. It all comes back to my observations around the Fed and Warsh’s new reigns. I think that markets are adjusting to a world of new constraints. I think investors are still underestimating how different the second half of this cycle may look.

While I am not yet entirely convinced that the “new” Fed has completely changed its clothes, I am open to reassessing my view given what markets are telling me. Warsh’s first FOMC meeting represented a potentially meaningful shift in the Fed’s reaction function towards restoring price stability. I still believe the communication was encouraging, but after spending several decades analysing central banks, I have learnt to place considerably more weight on actions than words. Institutions rarely abandon deeply ingrained habits overnight, particularly after more than a decade in which markets were repeatedly conditioned to expect monetary policy to cushion every growth scare, equity correction or financial accident. One unanimous meeting, a shorter statement and less forward guidance do not constitute a new regime. They simply increase the probability that one may be emerging.

Fortunately, macro investing is not about being right all the time. It is about continuously updating probabilities as new information arrives. We can hold multiple competing views simultaneously and gradually adjust them as markets reveal new information. My base case remains that the Fed has not yet fully escaped the post-GFC mentality of protecting growth and financial conditions. However, I also have to acknowledge that markets are increasingly behaving as though they believe otherwise. The rally in longer-dated Treasuries, the repricing at the front end, and the resilience of the dollar all suggest investors are beginning to assign a higher probability to a Federal Reserve prepared to tolerate slower growth if that is what restoring price stability requires.

Importantly, that does not automatically imply structurally higher bond yields. In fact, improved central bank credibility can more effectively anchor inflation expectations and ultimately support longer-duration assets. The bigger change lies in the reaction function itself. For years, investors assumed that weaker growth, softer equities, or falling oil prices would inevitably prompt an easier monetary policy. That assumption is becoming less certain. Lower energy prices undoubtedly help headline inflation, but they do little to address the broader inflationary forces embedded in the economy. Services inflation remains sticky, nominal demand continues to hold up remarkably well, while tariffs, supply-chain frictions and persistent wage pressures continue to complicate the disinflation story. If anything, the hurdle for rate cuts may now be considerably higher than markets have become accustomed to.

I will share further thoughts below, along with my more structural investment implications. In the meantime, we follow our regular framework as we enter a new week. In particular, we have the following items on today’s agenda:

Macro D’s latest Macro FX spreadsheet & thoughts

Weekly Macro Calendar

Macro Dashboard Analysis

PAAM Asset Allocation Model Update

let’s go!