Attack the Week (ATW)

Virtual Insanity / FOMC Week / Weekly Calendar / Chart Setups / PAAM Allocation Update

Sunday Thoughts

Everyone’s Spotify 2025 wrap is out. Mine didn’t feature too many surprises, other than the fact that my listening age is half my actual age. I take it as a compliment. I am the product of the music of my youth, and besides, new music doesn’t do it for me.

Unsurprisingly, my most recent Jamiroquai gig has catapulted one of his songs into my top 10 list. I started reflecting as I listened to a line in one of my favourite songs that has always stuck with me: “Futures made of virtual insanity now…” At the time, it sounded abstract, a warning aimed at a technologically dislocated society. Nearly three decades later, it reads like a direct commentary on modern financial markets. Because increasingly, what we see isn’t real — not in the sense of genuine risk-transfer, capital formation, or price discovery. It’s a theatre. It’s a game. A virtualised system where surface-level “truths” can be manufactured, distorted, or voted on.

And now we have Kalshi — markets where you can bet on basically anything, from CPI prints to Taylor Swift’s wedding destination. It is a prediction embraced as entertainment, financialised uncertainty packaged as participation. Market prices, which once moved asymptotically toward truth, now drift in the grey zone between speculation and spectacle.

This gameification isn’t healthy. The guardrails have quietly moved. We’re no longer just trading assets; many are trading narratives of possibility because reality itself feels increasingly out of reach. It’s a speculators’ circus where the ringmasters aren’t central banks or asset managers—they’re platforms selling dopamine disguised as financial inclusion.

And yet, I understand the appeal. I really do. When governments fail to support living standards, when wages stagnate, when purchasing power decays, people naturally reach for whatever tools might offer escape from the gravitational pull of debasement. Whether out of defiance, fun, or desperation, they turn to markets—any markets—to take back agency. I honour those who try. I wish every single one of them success.

But capital markets, casinos, and crowd-fuelled trading arenas cannot lift everyone out of their circumstances. If only it were that easy. Buying the dip, squeezing the shorts, meme-stock crusades—these have evolved into cultural identity markers. You don’t need wealth, training, or experience. You just need an app. Trading is for everyone now, for better or worse.

Crypto was the original playground for this behaviour, but we’ve moved on. Everything is tradeable. Everything.

And when everything can be traded, everything can become distorted. Price stops reflecting value. Outcome stops reflecting skill. And reality itself becomes malleable.

This speculative phase we’re living through - this virtual insanity— cannot end well for the majority. The history of manias teaches us that democratised speculation doesn’t democratise wealth; it democratises risk. The tide always goes out eventually, and when it does, we discover how many were swimming without even realising they were in the water.

For now, the neon lights remain bright, and the circus feels alive. But beneath the surface, we’re building a financial culture where entertainment and investment are becoming indistinguishable —and where the eventual bill will be paid by those who can least afford it.

The truth is simple: Not everyone can get rich from the markets.

But everyone can get hurt.

And that, perhaps, is the absolute insanity.

Here at Paper Alfa, we stay out of the circus and focus on what is right in front of us. Macro’s twists and turns are never dull, but a well-rounded process built on the foundations of a solid risk-management framework ensures that we stay in the game long enough to make the good times count and enable compounding.

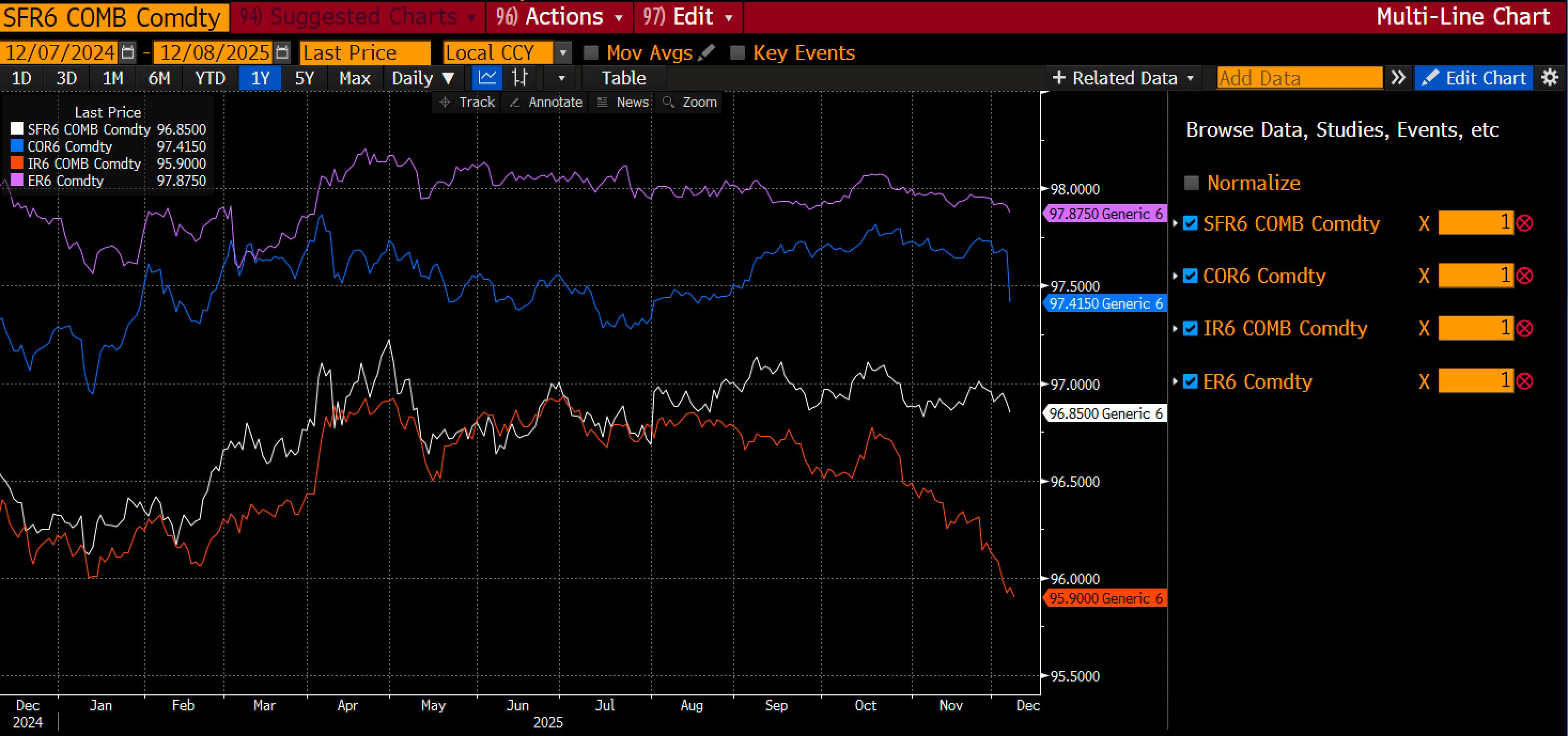

As usual, we face an uncertain setup as we enter FOMC week. The consensus seems to be shifting towards a hawkish cut, based on the notion that a cut is already priced in, but the committee sees little consensus to continue cutting. It is never that simple. More recently, the front-end in Australia and Canada has sharply repriced. Could the US front-end be next?

At the same time, energy commodities are starting to break out, although from very subdued levels. What if we are looking at rising energy costs into next year? The disinflationary forces might reverse and put the anticipated easing amid fiscal expansion into the limelight.

US 10-year yields are still in a downward shifting trend channel, with the top band at around 4.21% now in a firm target.

I will look at the chart setups behind the paywall further below.

Let’s now read some Macro D’s latest thoughts on the Fed and Trump before we analyse the weekly calendar, look at some interesting chart setups and interpret the output of our weekly asset allocation model.

Best of luck in FOMC week, and stay true to the reality that matters.