A Guide To Short-Term Interest Futures (STIR)

Basics & Complexities

STIR contracts stand for short-term interest rates securities which are futures on global exchanges pricing in various maturity forward contracts and options. The underlying are generally money-market rates from various different currencies and markets with the goal of efficiently hedging or speculating on the direction of money market rates which are obviously mostly influenced by central banks as their primary monetary lever. As for a guide to all the different money market rates, I highly recommend studying the excellent posts by Concoda. The most liquid futures will be found in predominantly developed markets, namely USD, EUR, GBP, JPY, AUD, CAD, CHF.

Something that seems like a niche corner of financial markets is the major playground of traditional macro houses. Brevan Howard, Moore Capital, and BlueCrest are just a few of the large players in this field. The market is deep, and liquidity is abundant in the major currencies. Euribor and, up until recently, Eurodollar futures were traded in the trillions (notional) on a daily basis. Knowing who the usual players are in this field, you’d have to be cautious when it comes to trading those products. Not to say that you can’t be profitable, but this is a big boy playing field, so naturally, some basics are needed.

The rise of SOFR futures came in light of retiring anything related to LIBOR contracts which the Eurodollar futures were linked to. The mechanics, however, are very similar.

You’ll find tons of information on the CME. Looking at prices to infer expectations is now slightly easier than with the previous Eurodollar futures, as they had a basis on top of the underlying unsecured rate, which was linked to the FRA/OIS basis.

STIR futures generally trade as a quote of 100% minus the interest rate. For example, if interest rates were 5.50 %, the futures would be quoted as 94.50. This methodology provides price synchronicity to other interest rate products, such as bonds, which fall as interest rates rise and rise as interest rates fall. If interest rates were suddenly cut by 0.25% or 25 basis points to 5.25%, the STIR future would rise to approximately 94.75.

Alternatively, the price of the STIR future can be used to back out an implied forward rate by 100% minus the STIR future price. In the above example, 100% - 94.75% = 5.25%. This STIR futures price implies a forward interest rate of 5.25%.

The key difference between the now retired Eurodollar and SOFR futures is obviously the underlying rate which is unsecured in the case of Eurodollar and secured for SOFR. Also, and more importantly, the SOFR contracts are now based on the average of the SOFR overnight rate during the last three months prior to the expiration of the contract. For Eurodollar futures, the settlement is forward-looking in that the final expiry price for the future will be determined by where the 3-month Libor would price as a term for the coming quarter. So if you say have a December 23 expiring contract, the former Eurodollar future would also have to price the likely money market evolution for the entirety of the first quarter of 2024.

Fed Fund Futures are also a quite popular yet less liquid instrument. They are also based on market participants' expectations of where the daily weighted average federal funds rate will be for a particular month in the future. The pricing is calculated using a day count basis of actual days/360, based on a 30-day month. I am sure you have seen the CME’s Fed watch tool. I would urge you to have a go and try calculating the probabilities yourself. The most important thing to remember is that they are priced as a weighted average over the month. If you have an FOMC meeting on the 15th of the month, the ultimate expiring price will be 50% of the current Fed Funds and 50% of the prevailing Fed Funds + 25 bps (assuming they only go in 25 bps steps). A quick way to work out pricing is to check a Fed Funds Future month where there is no meeting and use this as the basis to work out how much is priced for the meeting in the month prior. For more detail, work through the excellent examples here.

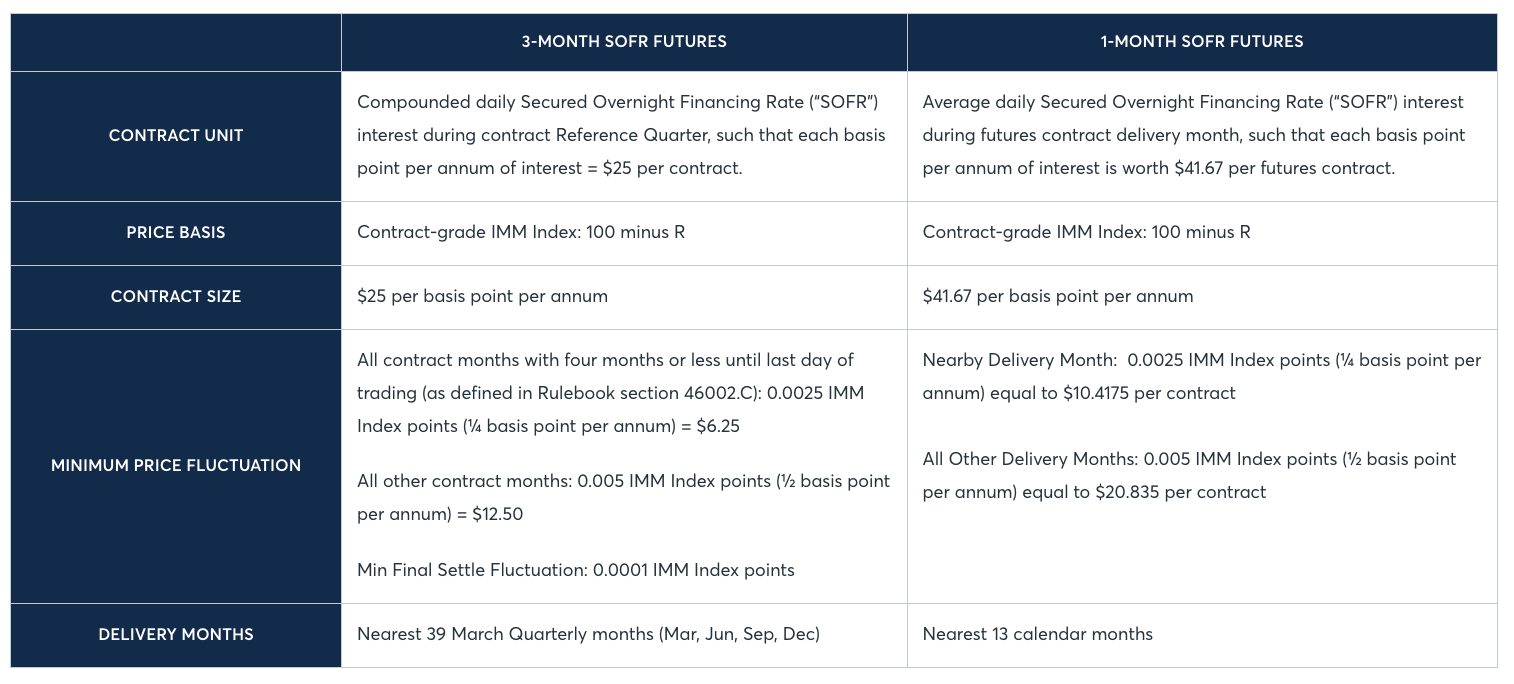

There is a small idiosyncrasy in STIRT futures in that their dv01 (value of a basis point move) remains constant. SOFR futures, as highlighted below, are based on fixed basis point value ($25 or €41.67, dependent on expiry) irrespective of the level of interest rates, and therefore their price sensitivity to a change in rates is linear and has no convexity as opposed to traditional bonds or swaps. If you want more information on this, read on here.

Trading Strategies

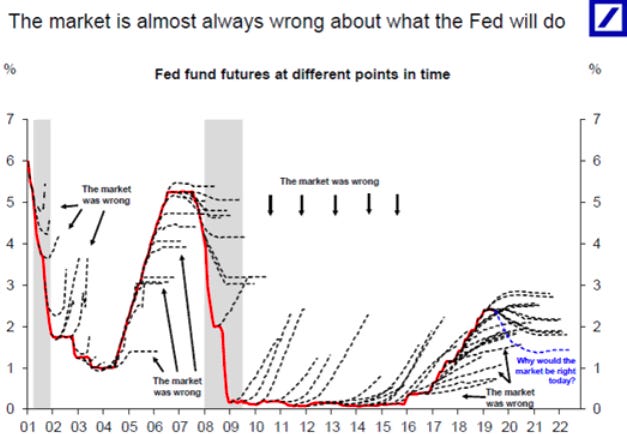

First of all, I’d like to put the record straight when it comes to charts like the one below. The market is always wrong! Such a superficially stupid thing to say. Those fan charts are respective futures prices further out. Having gone through the dynamics above the market, especially in STIR future, is giving you the weighted average view of all participants, which by definition is going to be wrong as it’s pricing probabilities, not outcomes. Think about the next Fed meeting. There rarely is a 0 or 100% probability but something in between. So the market is always going to be wrong.

There are generally two basic strategies applied when trading short-term interest rate futures. One is outright trading, going long or short, a contract across the maturity spectrum where you think you have discovered mispricings relative to where you will expect markets to go. The second one is to do it relative to either another contract on the curve or versus other country curves.

Of course, there are more complexities possible, especially since a lot of various options and strategies are being employed. I have seen plenty of them being traded. The most common strategies usually also involve selling volatility. This is usually done by selling 1 by 2 or 1 by 3 structures. This means that you buy one call option in one strike and sell 2 or 3 call options further out, collecting a net premium while you’re massively short volatility. This is a particularly popular trade ever since our monetary leaders have become very predictable. It’s obviously also quite a risky undertaking.

Calendar spreads involve the simultaneous buying and selling of the same underlying contract but in different delivery months.

An example would be the SOFR Dec 24 - SOFR Dec 23 spread below. Keep in mind when plotting those charts that there is a natural roll. In Bloomberg, you can pick, say, the 4th vs the 8th contract, which will include the roll. Tradingview doesn’t have the full curve beyond the first two contracts.

Butterfly spreads are plays on the curvature of a certain STIR curve. Essentially it can be thought of as combining two spreads across three maturity points.

Typically it is priced as taking the nearest maturity future + the furthest maturity future - 2 * the middle maturity future.

Below is the SOFR Dec 23 / Dec 24 / Dec 25 fly. The convention of buying the fly is to determine whether you are buying the nearest expiring future. If there would be perfect linearity in this curve, then the fly would trade zero. The fly is trading negative because the market puts in more cuts between Dec 23 and Dec 24 compared to Dec 24 and Dec 25.

I hope you find this guide useful. Remember to do your own research before entering any trading or investing arena, especially this one, which is littered which big hedge fund traders and algorithmic trading strategies; it’s far from easy.

As in all things in investing, try to understand what is driving the markets and causing the price action. Teach yourself to observe different risk-reward characteristics.

Best of Luck out there!

Disclaimer

Thank you for this!!!

If you’ll keep up with this kind of content I’ll have to become a paid subscriber🙏

STIR options next? ;)